Independent evidence-based advice on infrastructure planning, policy and priorities to benefit all Australians

Annual Performance Statement 2026

1 April 2026

Introduction

Introduction

Infrastructure Australia is the Australian Government’s independent adviser on nationally significant infrastructure investment planning and prioritisation. Sectors within Infrastructure Australia’s remit comprise transport, energy, communications, water, and social infrastructure.1

Purpose of this Statement

This document delivers on the requirement in section 5DB of the Infrastructure Australia Act 2008 (IA Act) that Infrastructure Australia must give to the Minister and table in both Houses of Parliament each financial year:

- an annual performance statement (the Statement or the Performance Statement) on the performance outcomes being achieved by states, territories and local government authorities in relation to the infrastructure investment program and existing project initiatives funded by the Commonwealth; and

- an annual budget statement to inform the Commonwealth’s budget process on infrastructure investment.

_____

- Social infrastructure is generally considered in the context of a broader infrastructure development proposal that includes integrated investments in other infrastructure and contained in place or region-based infrastructure planning.

Analysis of the Australian Government’s program of infrastructure investments

Analysis of the Australian Government’s program of infrastructure investments

This Statement reports on the performance outcomes being achieved by states, territories and local government authorities in relation to the infrastructure investment program and existing project initiatives funded by the Australian Government, across Infrastructure Australia’s sectoral remit.

The Australian Government provides funding for state and territory infrastructure projects through two main mechanisms: grant programs and the Federal Financial Relations (FFR) system. This Statement provides analysis of the performance of Australian Government funding of infrastructure projects under the FFR system. It excludes analysis of Australian Government investments through equity, loans and special purpose vehicles to Government Business Enterprises and private sector entities.2

Criteria used to identify in-scope projects

As Infrastructure Australia’s remit is nationally significant infrastructure across transport, energy, water, communications and social infrastructure sectors, this Statement focuses on a subset of Australian infrastructure projects that meet defined criteria.

A project defined as in-scope for Performance Statement analysis:

- is part of the infrastructure sectoral Federation Funding Agreements (FFA)

- is an individual, nationally significant project (i.e., does not form part of a funding package and/or funding program)

- includes an Australian Government funding contribution or commitment over $250 million

- is funded in the Federal Budget

- is in the transport, energy, communications, water, or social infrastructure sectors

- has been or is expected to be evaluated by Infrastructure Australia.

Projects completed before May 2022 in the FFA Schedule for Land Transport Infrastructure Projects are excluded from analysis.3

Projects meeting the criteria above were identified in the infrastructure sectoral FFAs from the following FFA schedules:

- Land Transport Infrastructure Projects (2024-2029)

- National Water Grid Fund

- Pilbara Ports Common User Upgrades

- Perth City Deal.

Projects that do not meet the above criteria are excluded from analysis. Therefore, the Performance Statement does not analyse all the Australian Government’s infrastructure investments.

How the Statement corresponds with the 10-year Infrastructure Investment Program, Infrastructure Portfolio Budget Statements and MYEFO

While the majority of in-scope projects analysed as part of the Statement are in the Australian Government’s 10-year Infrastructure Investment Program (IIP), there are in-scope projects that are not in the IIP, such as those in other portfolios, like water.

Likewise, the Statement does not correspond with the Infrastructure, Transport, Regional Development, Communications, Sport and the Arts Portfolio Budget Statements. This is because Infrastructure Australia’s remit includes sectors outside of this portfolio.

The Statement uses project data available from the 2025–26 Federal Budget (and previous Budgets), as this is the Australian Government’s main financial report outlining Australia’s economic and fiscal outlook. The analysis has not considered new projects, or changes to existing projects, arising in the 2025 Mid-Year Economic and Fiscal Outlook (MYEFO) or other financial reporting.

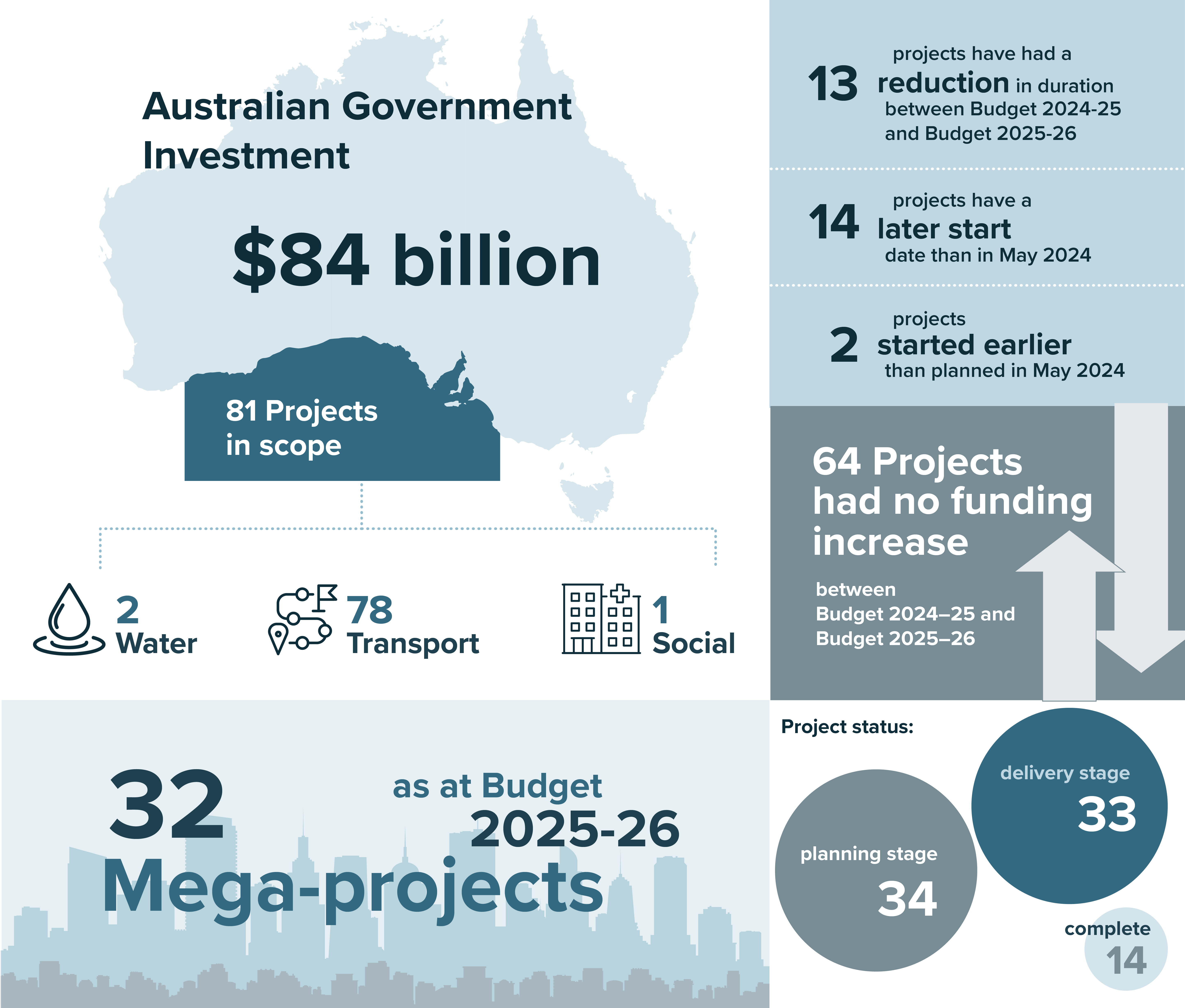

Summary of in-scope projects

This year’s analysis is based on data provided on 81 projects, comprising 78 transport infrastructure projects, 2 water infrastructure projects, and 1 social infrastructure project that meet the defined criteria.4

For in-scope projects, Infrastructure Australia analysed:

- project attributes, including sector, project status, and funding sources

- changes in time and costs between the 2024–25 and 2025–26 Federal Budget papers.

Nine projects within the dataset have not been evaluated for time and cost changes, as they represent new commitments in Budget 2025–26 and were not part of previous budget data.5

The following analysis relates to in-scope projects only and therefore provides a subsection of the Australian Government’s infrastructure investment. It does not look at or analyse delivery of the Australian Government’s full program of infrastructure investments.

Figure 1: Performance outcomes analysis - summary of key findings

Performance outcomes analysis - key findings

The 2026 Performance Statement indicates greater stability in the cost and schedule performance of the Australian Government’s nationally significant infrastructure investments.

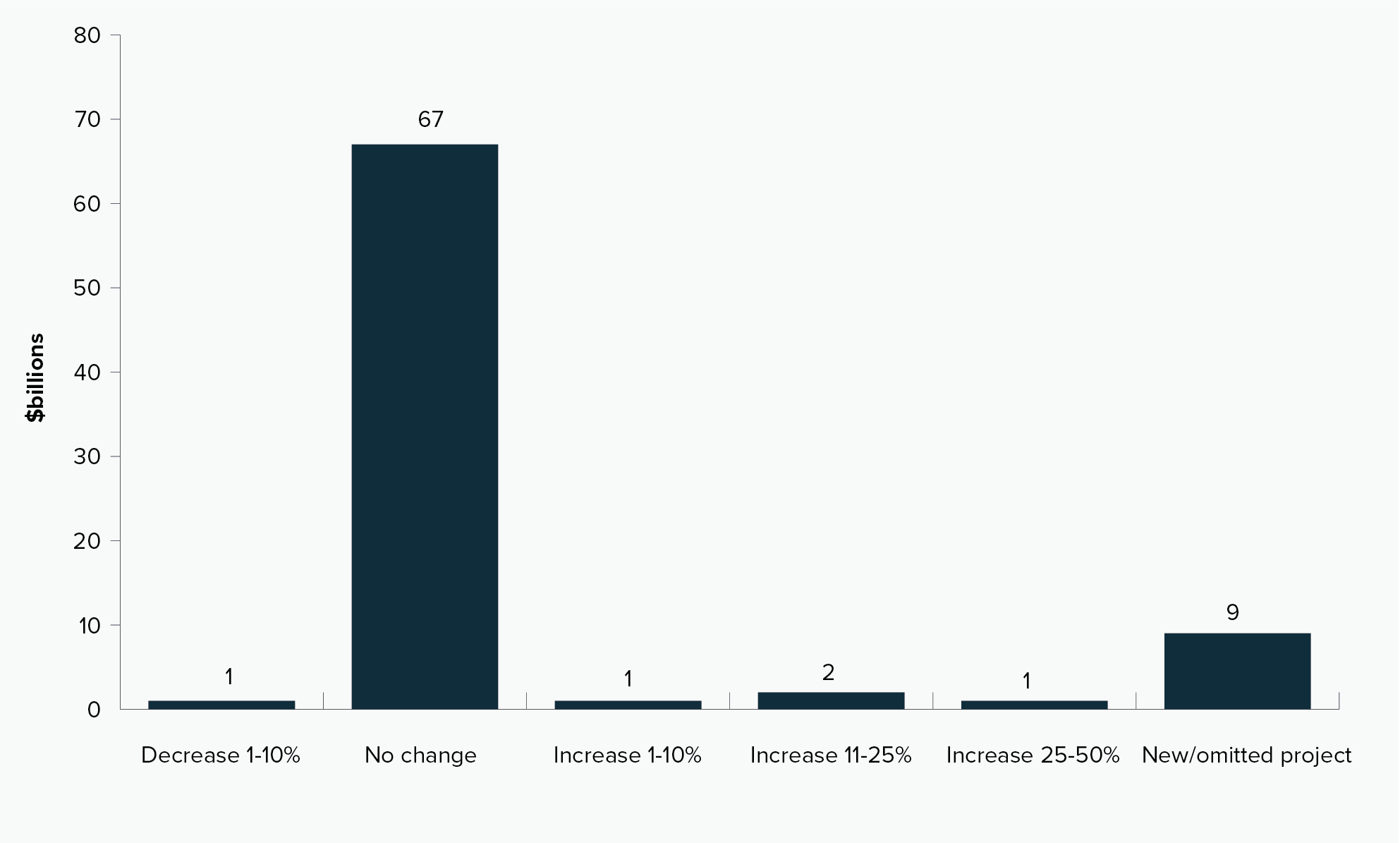

Of the 81 in-scope projects funded in Budget 2025–26, a majority (64 projects or 65% of total value of projects) had no change in total project cost. Six projects increased in cost between Budget 2024–25 and Budget 2025–26, compared to the 2025 Performance Statement, which showed 31 projects increased in project cost between Budget 2023–24 and Budget 2024–25.

This year’s Performance Statement shows a clear shift in cost-escalation trends.

Most project cost increases were below 25%, whereas last year’s Statement showed most project cost increases exceeded 25%.

The reduction in project cost increases translated into fewer funding increases for the Australian Government.

Australian Government funding increased for 4 out of the 6 projects with total project cost increases, with the Australian Government funding a 38% share. All up, Australian Government funding for the 72 projects reported in last year’s Statement increased by less than 1%.

Fewer cost increases allows unallocated funding to be directed toward new infrastructure commitments.

The 2026 Performance Statement reports a growing number of in-scope projects and Australian Government investment with:

- Nine new projects added to the Performance Statement dataset in Budget 2025–26 (7 road and 2 rail projects), versus 4 new projects in Budget 2024–25

- Megaprojects growing to 32 projects in Budget 2025–26 from 26 in Budget 2024–256

- Australian Government funding rising to $84 billion over 81 projects in Budget 2025–26 from $70 billion over 72 projects in Budget 2024–25

- Of the $14 billion in new Australian Government funding for in-scope projects in Budget 2025–26, $13.4 billion went to funding new projects.

As the Performance Statement only analyses a subset of projects in the Australian Government’s infrastructure investment program, these figures do not necessarily reflect the full scope of Australian Government funding in infrastructure overall.

Correlating with easing cost pressure is better schedule performance.

The reported project schedules were more stable in Budget 2025–26 (69% of projects by value with no change to time-to-completion), compared to Budget 2024–25 (48% of projects by value with no change to time-to-completion).

Project cost pressures may have eased for several reasons, including macroeconomic factors and project-specific drivers.7 The improved cost performance observed in the 2026 Performance Statement could also be influenced by the Australian Government’s reforms to infrastructure decision-making.

The 2023 Independent Strategic Review of the Infrastructure Investment Program and 2023 Independent Review of the National Partnership Agreement on Land Transport Infrastructure Projects made several recommendations to improve the management of the infrastructure project investment portfolio. Many of those recommendations have been operationalised by, for example, the FFA Schedule on Land Transport Infrastructure Projects (2024–2029) and the Infrastructure Policy Statement.

Australian Government’s reforms to infrastructure decision making

In 2023, the Australian Government reshaped the IIP following two major reviews: the Infrastructure Investment Program Strategic Review (the Strategic Review) and the Independent Review of the National Partnership Agreement on Land Transport Infrastructure Projects (the Halton Review).

The Strategic Review found the pipeline was unsustainable, with significant cost pressures, inconsistent governance, and many projects lacking a clear national rationale or credible planning and costings. It recommended annual 10-year state infrastructure plans, stronger and earlier gateway assurance processes, improved cost escalation methods, a 50:50 funding split between Australian and state and territory governments, rolling programs targeted toward nationally significant outcomes, and reviewing the National Land Transport Act 2014.

Additionally, the Halton Review reinforced the need for disciplined investment decisions through a structured two-pass process and strengthened risk-based governance.

Together, the recommendations of these reviews underpin the Government’s reform package. The Infrastructure Policy Statement now provides a strategic framework for assessing national significance and alignment with long-term planning priorities. The FFA Schedule for Land Transport Infrastructure Projects (2024–2029) and the associated 2025 Notes on Administration, which replaced the National Partnership Agreement, embed the two-pass process, enhanced gateway assurance requirements, and the Confidence Index. These measures are helping to improve cost stability as observed by the 2026 Performance Statement in Budget 2025–26.

Analysis of project attributes

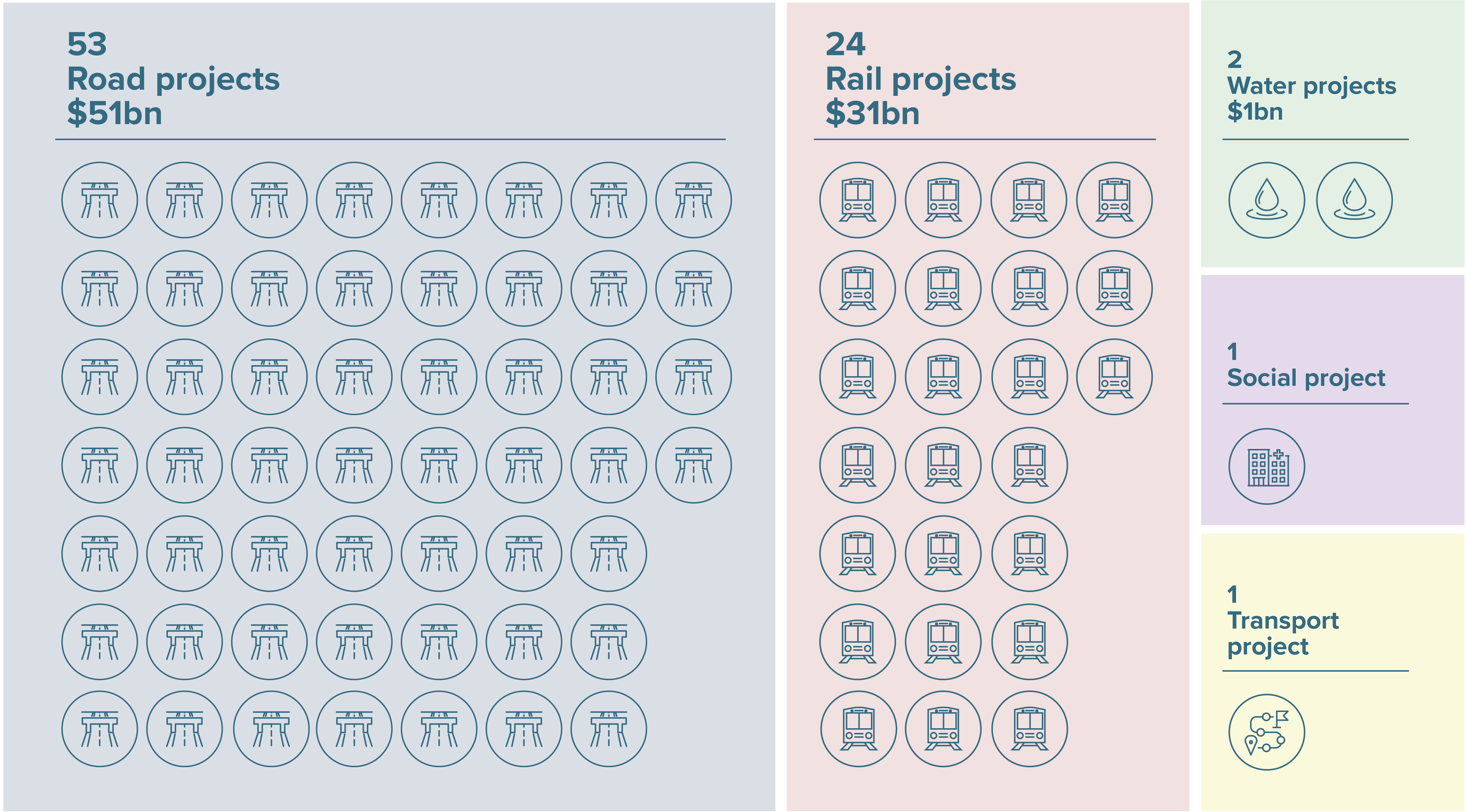

Road and rail infrastructure projects represent the majority of Australian Government funding for the in-scope dataset, accounting for 61% ($51 billion) and 37% ($31 billion), respectively. Water projects are 1% of Australian Government investment, as are Social and Transport-multimodal projects combined.

Figure 2: Projects analysed by sector, count and by Australian Government investment

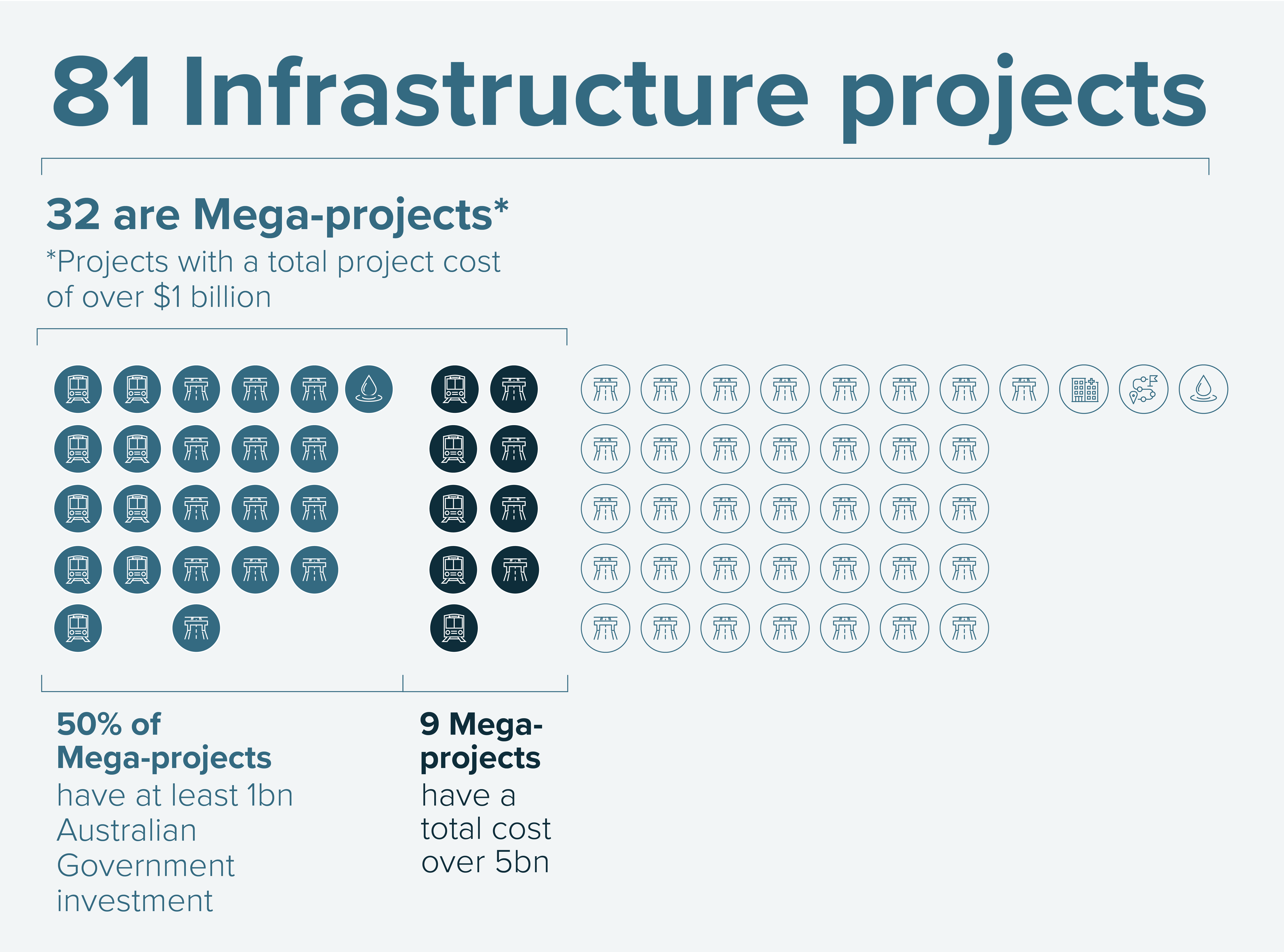

The in-scope projects include 32 megaprojects (investments with a total project cost of over $1 billion). Sixteen megaprojects have Australian Government investment of at least $1 billion. There are 9 projects that have a total cost over $5 billion, representing 64% of the in-scope projects by value, and 50% of the Australian Government’s investment. In comparison, the 49 projects with a total project cost of less than $1 billion represent 60% of projects by count, but only 16% by value and 24% of the Australian Government’s investment. Because of their size, megaprojects influence the performance of the Australian Government’s investments. As project size and complexity increase, project delivery becomes more complicated, and the relative impacts of realised risks and schedule delays on cost increase.

Figure 3: Megaproject count and size as proportion of all projects and Australian Government investment

Megaprojects and the infrastructure investment program

As noted in Infrastructure Australia’s 2024 Annual Budget Statement, megaprojects can increase the risk profile of the overall infrastructure investment program as they can be more at risk of cost and time overruns.

While in-scope projects did not have large cost or time variations this year, previous annual statements have demonstrated a correlation between size, time and cost risk.

With megaprojects influencing the size and profile of the Australian Government’s investment pipeline, Infrastructure Australia’s 2025 Market Capacity Report highlights the substantial opportunities for megaprojects to enhance innovation and productivity in the construction sector.

Despite a short-term lift in productivity (2% growth in 2023–24), long-term construction productivity remains stagnant and well below historical benchmarks. Modern methods of construction, including prefabrication, account for less than 5% of the market, and current procurement practices focused on lowest cost continue to discourage innovation and long-term value creation.

There is a clear opportunity to develop incentives and investment models that address the upfront costs of innovation, enabling broader national adoption of new technologies and methods. Targeted incentives for technology demonstration and scaling, along with harmonised standards and procurement processes, are practical ways the Australian Government can use its project sponsor role to drive innovation in megaprojects and reduce long-term risks in its investment pipeline.

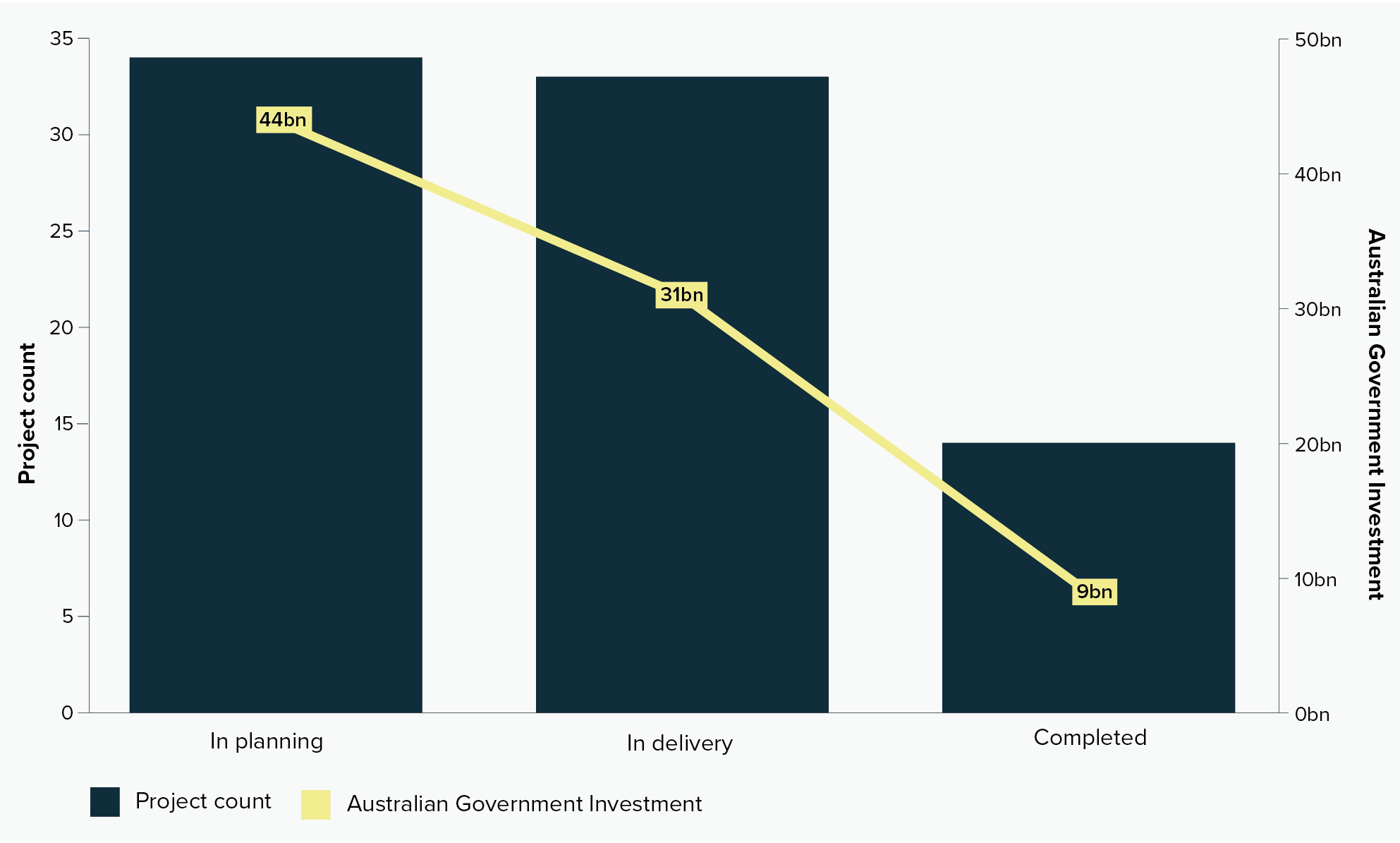

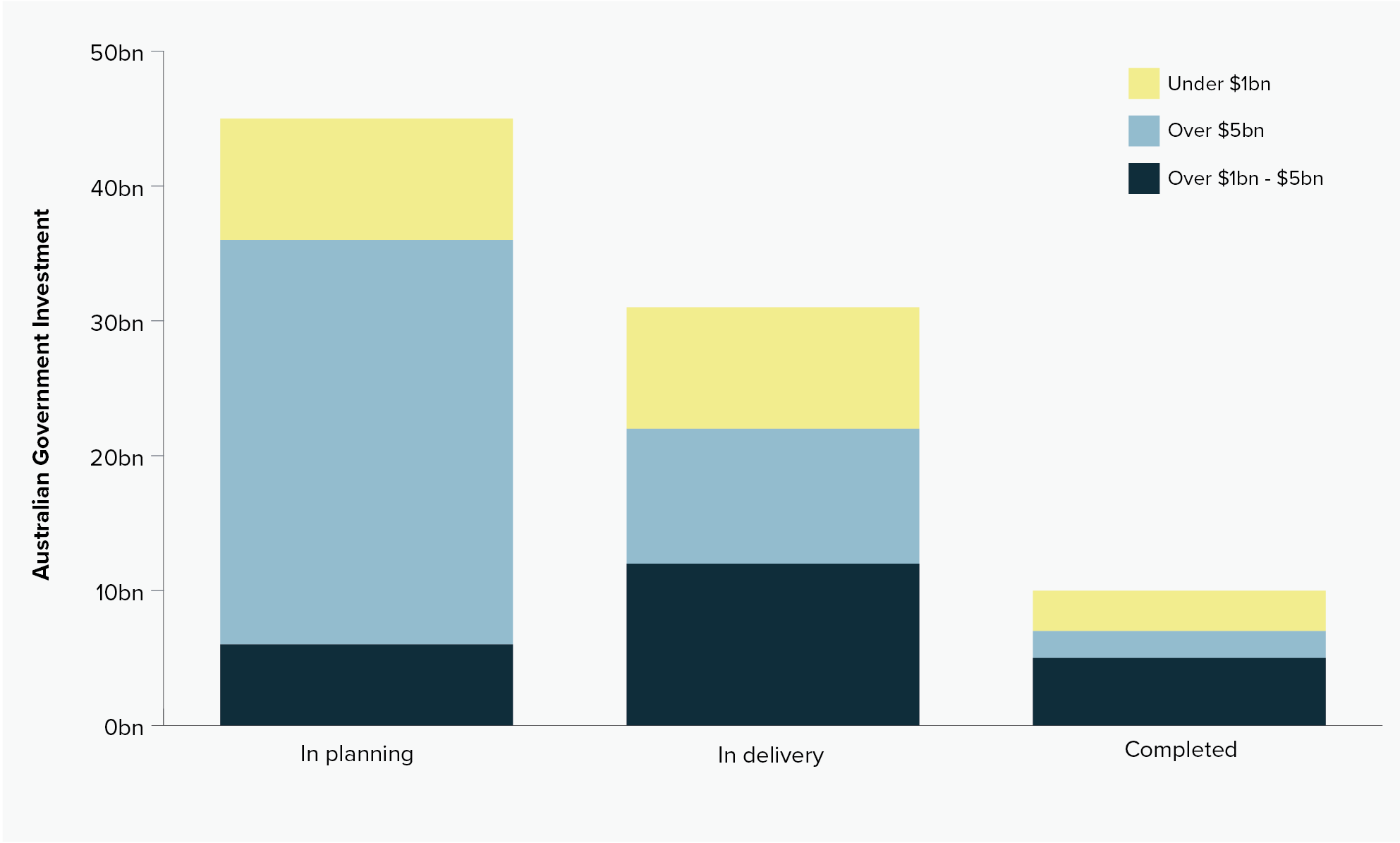

Figure 4 shows that most of the Australian Government investments are in the planning or delivery phases: 34 projects (53% by investment value) are in planning and 33 projects (37% by investment value) are in delivery. Fourteen projects, 10% by value of the Australian Government’s investment, are completed. Figure 5 shows most megaprojects by value of Australian Government investment are in the planning phase.

Figure 4: Project phase by count (bars) and by Australian Government investment ($ billions) (line)

Figure 5: Australian Government investment by project phase and grouped by size of project ($ billions)8

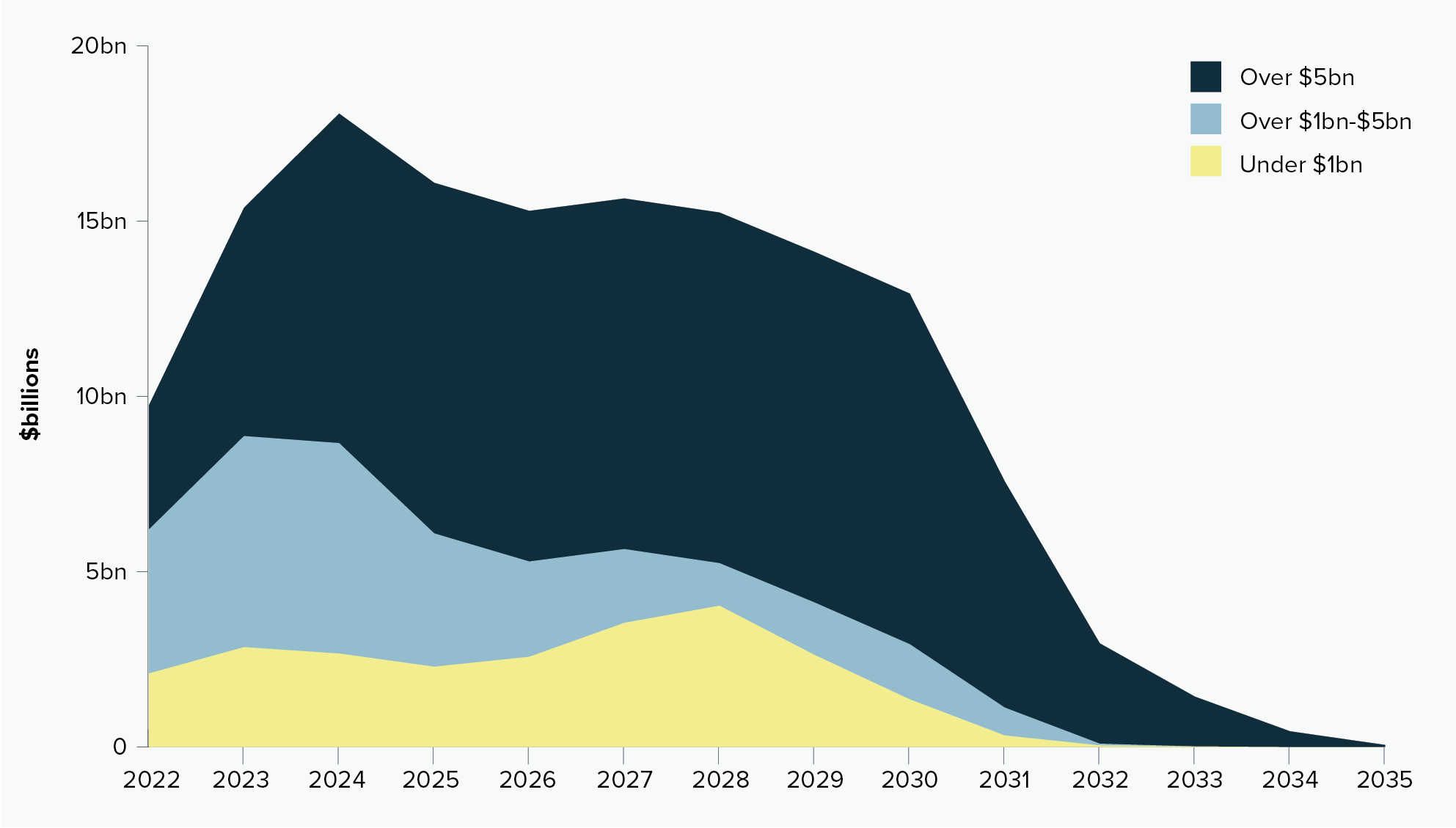

Figure 6 shows a forecasted profile of in-scope projects over their delivery schedules. Megaprojects represent 64% of the pipeline by value. Small shifts in timeline (and subsequently cost) for megaprojects can shift a significant proportion of the pipeline’s value, with meaningful impacts on market capacity and construction inflation.

Figure 6: Forecasted profile of in-scope projects over the delivery timeframe, megaprojects (over $1bn) represent majority of the pipeline ($ billions)9

Maintaining a balanced program (sequencing projects, geographical diversity and asset type diversity), particularly for megaprojects, is important to provide a sustainable pipeline of investment for industry that is deliverable and provides a realistic funding profile for governments.

Changes between Budget 2024–25 and Budget 2025–26

Analysis of variation in cost and time between Budget 2024–25 and Budget 2025–26 is for 72 of the in-scope projects as it excludes the 9 projects that included new commitments in Budget 2025–26. These 9 projects appear in charts under ‘new/omitted project’.

Variations in delivery schedules

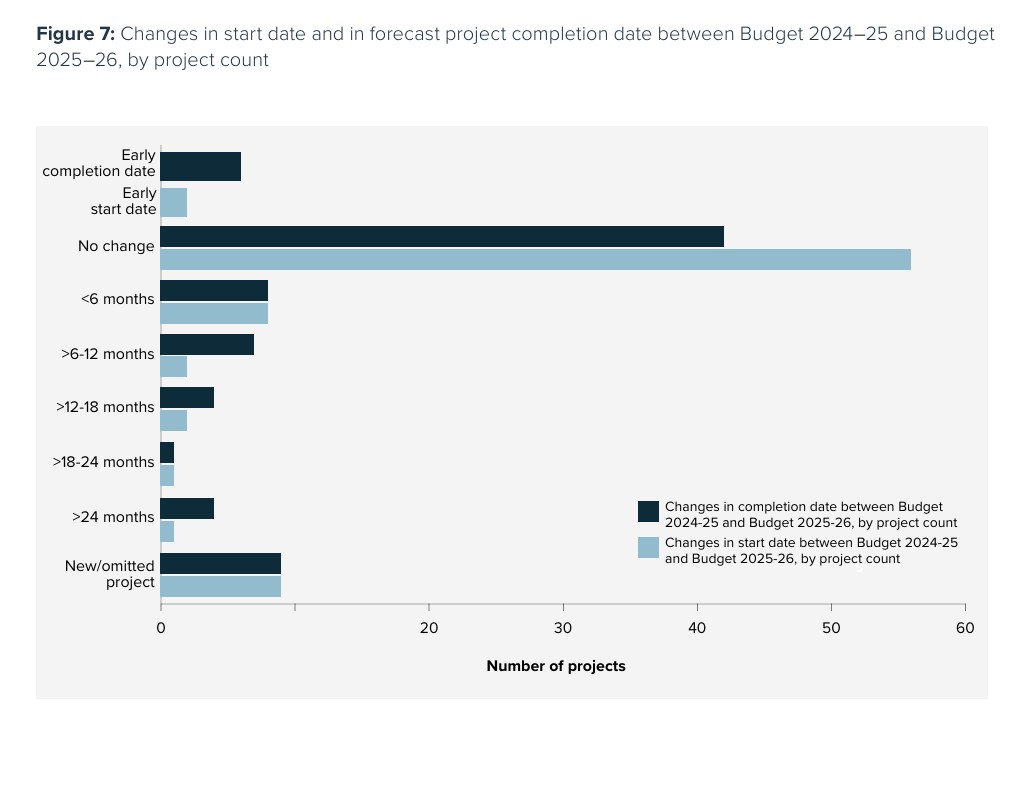

Project start dates have held or been brought forward in 58 (72%) projects since Budget 2024–25, and 14 projects are starting later (Figure 7 refers).

Forecast project completion date has been brought forward or remains unchanged for 48 projects (60%) with 6 projects forecasting earlier delivery completion (Figure 7 refers).

Expected project duration (time-to-completion) has increased for 17 projects with 13 projects expecting an increase in construction schedule of at least 25%, 2 projects expecting a schedule increase around 50% and 2 projects anticipating an increase in construction schedule of over 50% (Figure 8 refers).

Figure 7: Changes in start date and in forecast project completion date between Budget 2024–25 and Budget 2025–26, by project count

Figure 8: Percentage change in duration between Budget 2024–25 and Budget 2025–26, by project count (bars) and by value ($ billions) (line)

Figure 9 shows that projects with increased duration totalled $17 billion in total project value, or 9% of projects by value.

Increases in duration were more likely to occur in road projects (21% of road projects) as opposed to rail projects (17% of rail projects).

Project schedules were more stable in Budget 2025–26 (69% of projects by value with no change to time-to-completion), compared to Budget 2024–25 (48% of projects by value with no change to time-to-completion).

Variations in project cost and funding

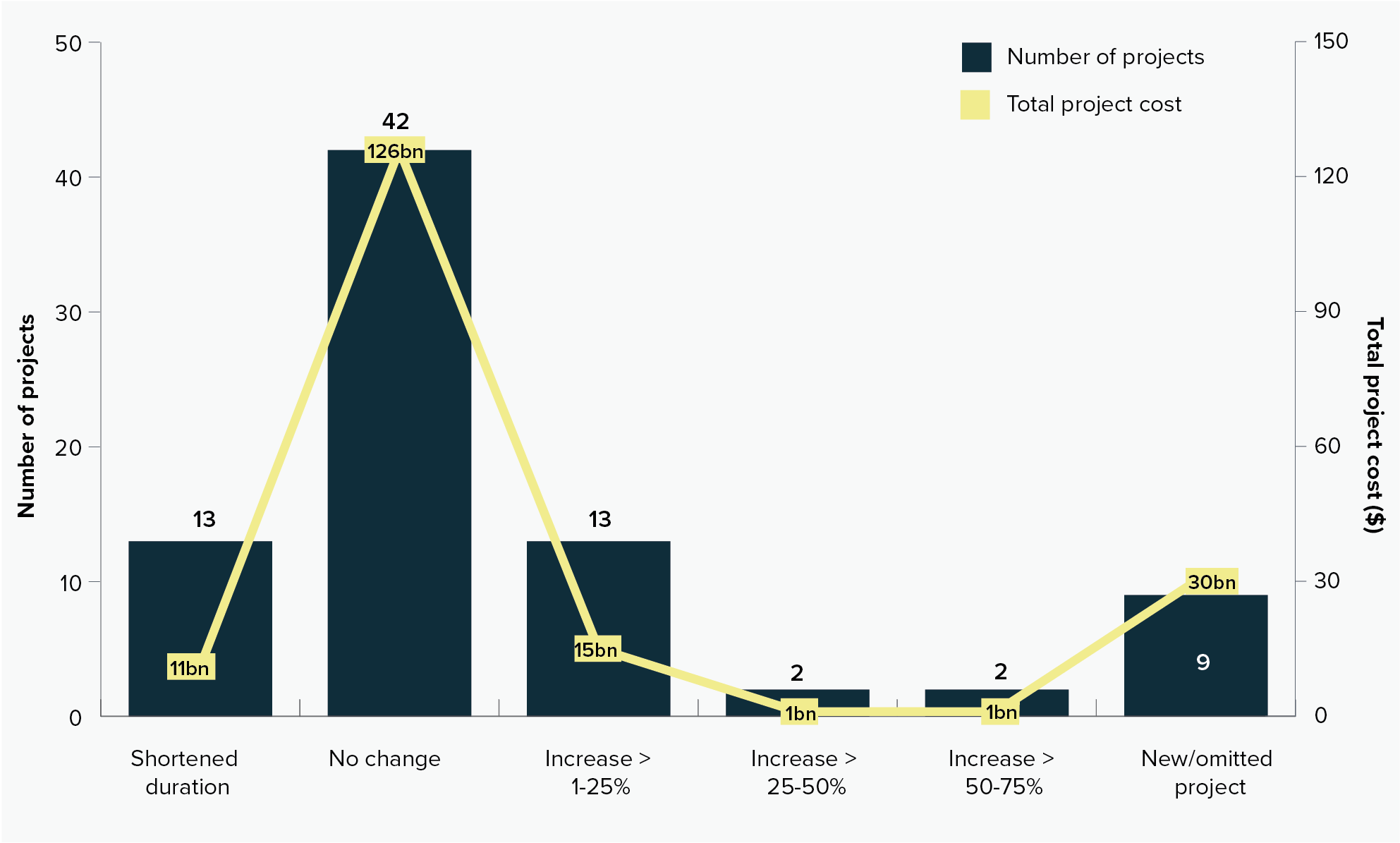

Across the 81 in-scope projects, there have been much smaller changes in total project cost in Budget 2025–26 than in those reported for the same projects in Budget 2024–25.

Furthermore, most in-scope projects experienced smaller cost increases in Budget 2025–26 compared to Budget 2024–25. Only 6 projects saw any cost increases, 5 of these with cost increases less than 25% of project value in Budget 2025–26, versus 31 projects with cost increases in Budget 2024–25, 18 of these with cost increases more than 25%.

Correlating with improved project cost performance, Australian Government funding increases for in-scope projects in Budget 2025–26 were modest. Four projects received an increase in Australian Government funding, three of which involved increases of less than 25% (Figure 9 refers). This contrasts with in-scope projects in Budget 2024–25, where 29 projects saw Australian Government funding increases, including 11 with increases of more than 50%.

Figure 9: Percentage change in Australia Government funding between Budget 2024–25 and Budget 2025–26, by project count

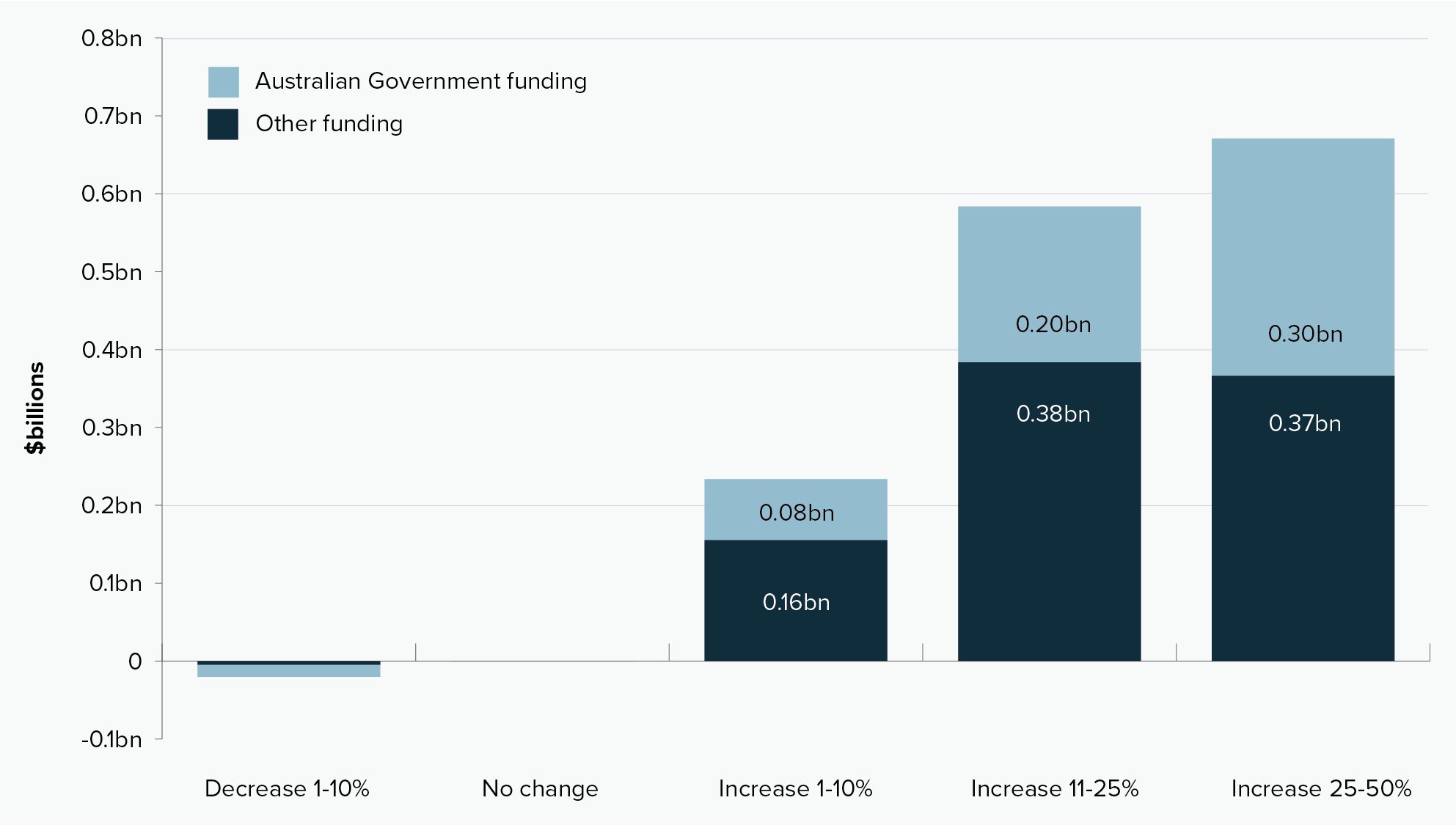

The Australian Government funded a lower number of cost increases across in-scope projects in Budget 2025–26, funding 38% of project cost increases (Figure 10 refers).10 All up, Australian Government funding increases on existing project investments in Budget 2025–26 increased by less than 1% on Budget 2024–25.11

Figure 10: Project cost changes between Budget 2024–25 and Budget 2025–26, grouped by funding source ($ billions)

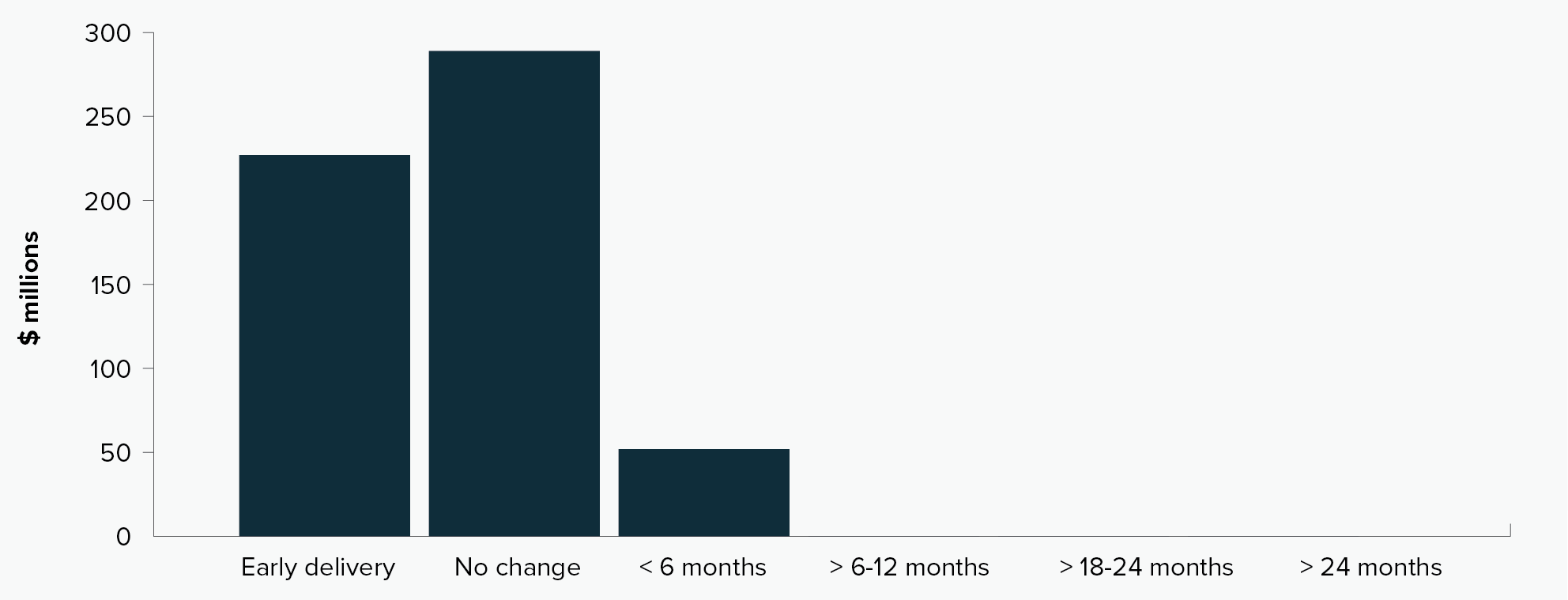

In Budget 2025–26, changes in Australian Government funding for in-scope projects did not align with longer time-to-completion. Over 90% of Australian Government funding increases were allocated to projects that are expected to be delivered early or with no change to their schedule, with only a small proportion directed to delayed projects (Figure 11 refers). This could indicate that additional funding was primarily focussed on stabilising or accelerating existing project delivery, rather than addressing schedule slippage as 98% of cost increases occurred in projects in delivery.

Figure 11: Change in Australian Government funding due to change in project duration ($ millions)

_____

- There are significant Australian Government investments in infrastructure outside of the FFR system, including equity investments and loans through Government Business Enterprises such as the NBN Co, Snowy Hydro and Western Sydney Airport Co, and through Special Investment Vehicles such as the Northern Australian Infrastructure Facility, the Clean Energy Finance Corporation and Housing Australia.

- Aligned with reporting by the Department of Infrastructure, Transport, Regional Development, Communications, Sport and the Arts.

- Project data was provided by the Department of Infrastructure, Transport, Regional Development, Communications, Sport and the Arts for transport and social infrastructure projects and by the Department of Climate Change, Energy, the Environment and Water for water infrastructure projects.

- This includes Melbourne Airport Rail which had significant new scope added at Budget 2025–26 with Sunshine Station redevelopment added to the project. It is omitted from analysis of time and cost changes to avoid skewing results.

- Megaprojects have a total project cost above $1 billion.

- The main macroeconomic drivers of infrastructure project costs are inflation, interest rates, commodity prices, and labour market dynamics, which collectively influence the cost of materials, financing, and labour. These factors are partly exogenous to government policy. Project-specific factors are scope, project management and governance, resource management, planning and forecasts, engineering and design, contractual and stakeholder issues, and geotechnical and site conditions.

- May not sum due to rounding.

- Infrastructure Australia has calculated each project’s Total Project Cost distributed across its construction years using a standard S-curve formula.

- ~$568 million in Australian Government funding increase, over ~$1.5 billion of total project cost increases.

- Australian Government funding increases less decreases in 2025–26 equals $568 million, over Australian Government total investment in 2024–25 which equalled $70 billion. See Annual Performance Statement 2025

| Introduction |

| National Infrastructure Investment Priorities |

| Considerations for infrastructure planning and delivery |

Annual Budget Statement 2026

1 April 2026

Introduction

Introduction

Infrastructure Australia is the Australian Government’s independent adviser on nationally significant infrastructure investment planning and prioritisation. Sectors within Infrastructure Australia’s remit comprise transport, energy, communications, water and social infrastructure.1

Purpose of this statement

This document delivers on the requirement of section 5DB of the Infrastructure Australia Act 2008 that Infrastructure Australia must give to the Minister and table in both Houses of Parliament each financial year:

- an annual budget statement to inform the annual Commonwealth budget process on infrastructure investment; and

- an annual performance statement on the performance outcomes being achieved by states, territories and local government authorities in relation to the infrastructure investment program and existing project initiatives funded by the Commonwealth.

In addition to the legislative requirements, Infrastructure Australia’s Statement of Expectations notes that our advice is to be aligned to the Australian Government’s needs and strategic infrastructure priorities.

The Annual Budget Statement 2026

This third edition of the Annual Budget Statement provides advice in response to Australian Government needs and strategic infrastructure priorities, including those outlined in the Infrastructure Policy Statement (IPS). This includes:

- National Infrastructure Investment Priorities, developed by Infrastructure Australia from Australian, state and territory plans and investments, consultation with stakeholders, Infrastructure Australia research and submissions for the 2026 Infrastructure Priority List (IPL).

- Considerations for infrastructure planning and delivery, including infrastructure market capacity issues and constraints based on Infrastructure Australia’s latest 2025 Infrastructure Market Capacity research and a focus on infrastructure decarbonisation and productivity.

This Budget Statement identifies nationally significant priority infrastructure proposals determined by Infrastructure Australia as ready for Australian Government investment in planning or delivery funding in the 2026-27 Budget.

The 2026 Infrastructure Priority List also identifies priorities for future investment over the medium term (2-4 year pipeline) and long-term (5-10 year pipeline).

_____

1. Social infrastructure is generally considered in the context of broader place or region-based infrastructure planning.

National Infrastructure Investment Priorities

National Infrastructure Investment Priorities

As Australia’s population grows and needs change, so too does the demand for infrastructure that is resilient, efficient and meets the needs of our long-term future. From expanding transport networks that boost productivity and better connect our communities, to projects that enhance communication and water security, support new housing, and ensure a stable and secure energy future, our infrastructure must evolve to support the prosperity of our nation.

The five national infrastructure investment priorities identified by Infrastructure Australia in the 2025 Annual Budget Statement (see Figure 1) represent Infrastructure Australia’s view of the most significant focus areas for infrastructure investment needs at a national level.

Figure 1: Current national infrastructure investment priorities

The advice in this Budget Statement has been informed by:

- Infrastructure Australia’s research and analysis on national infrastructure needs, gaps and priorities.

- Extensive engagement with Australian, state and territory governments and other stakeholders on current and emerging priorities for infrastructure planning and delivery investment, including as part of developing the 2026 Infrastructure Priority List.

- Analysis of infrastructure issues, needs, gaps and priorities identified by Australian governments, including published infrastructure strategies, plans and investment pipelines.

The five priorities identified above remain priorities to address and support nationally significant infrastructure needs and opportunities in response to Australian Government priorities and objectives, such as the Infrastructure Policy Statement and a range of other policies and initiatives of the Australian Government, including but not limited to those identified in Figure 2.

Figure 2: Examples of Australian Government policies and initiatives aligned to national priorities for infrastructure investment

Enabling productive and resilient infrastructure networks and supply chains

The Infrastructure Policy Statement states that the Australian Government will seek to invest in infrastructure projects that:

- improve national productivity.

- improve supply chain efficiency by removing bottlenecks and connecting regions to markets.

- improve the resilience of critical infrastructure networks, such as rail and road corridors.

- contribute to the goals of the National Freight and Supply Chain Strategy.

Investment and reforms to achieve this include high-performing, resilient and technology-enabled transport, energy, water, telecommunications and social infrastructure that meets the current and future needs of a changing economy, population and climate.

As the Australian Government’s independent adviser on nationally significant infrastructure, Infrastructure Australia has an important role in providing a cohesive national, cross-sectoral understanding of current and future infrastructure needs to enable modern, productive and resilient infrastructure networks.

Three of the five national infrastructure investment priorities identified by Infrastructure Australia are relevant to this challenge: high productivity freight networks, ports capacity and connectivity, and secure, sustainable water for growth. This section recommends investment opportunities in each of these areas that should be considered as priorities for Australian Government investment in 2026.

High Productivity Freight Networks

Australia’s freight networks are the backbone of domestic supply chains, enabling the efficient movement of goods across vast distances and supporting the nation’s economic growth and resilience.

Domestic freight is projected to increase by up to 26 per cent between 2020 and 2050, yet rail freight is expected to grow by just 5.7 per cent compared to a 77 per cent increase in road freight over the same period.2 Shifting more freight from road to rail is essential to reduce road congestion, improve productivity, lower greenhouse gas emissions, and enhance network reliability. Road freight and resilient supply chains remain crucial to Australia’s freight task, including for connecting regions to major gateways and serving regional and remote communities.

Expanding intermodal terminal capacity is key to meeting future freight demand, encouraging a shift to rail freight and strengthening supply chain resilience. Infrastructure Australia has identified the following nationally significant infrastructure proposal as an investment-ready priority:

- Northern Territory freight rail and logistics capacity improvements – this proposal is an immediate priority for planning investment to support local supply chains and connectivity to the national transport network. The Australian Government has committed $440 million in planned equity to create a network of regional logistics hubs along the Darwin-Tarcoola rail line, which is part of the National Network for Interoperability. Further planning is required to progress this proposal, which will increase supply chain capacity and assets in regional areas.3

Safe, reliable access for critical regional and remote supply chains is a national priority to ensure access to essential goods and services. Infrastructure Australia has identified the following nationally significant infrastructure proposals as investment-ready priorities:

- Road access improvements for remote Western Australia communities, which is a priority for planning investment to address unreliable road access.

- Great Northern Highway improvements – Broome to Kununurra in Western Australia, which is a priority for planning investment to address safety and resilience issues from regular weather-related road closures. The corridor received a vulnerability rating of medium in the 2023 Road and Rail Supply Chain Resilience Review.

Future strategic priorities for investment identified by Infrastructure Australia include:

- Australia’s rail infrastructure and enabling technologies, to advance interoperability across the National Network for Interoperability (NNI) – including the adoption of digital train control and signalling systems on the national and interstate rail network that comply with European Train Control System (ETCS) mandatory standards – and improve the safety, productivity and competitiveness of critical national freight and passenger rail corridors.

- Intermodal capacity and connectivity, including increased use of integrated intermodal precincts, to optimise national freight efficiency, reduce costs and increase the role of rail freight, enabling seamless road-rail integration and improving overall network performance.

- Enhancing the productivity and reliability of key road freight routes, including the development and upgrade of networks to enable higher productivity vehicles, and targeted upgrades to strengthen the resilience and safety of nationally significant corridors.

More details on specific proposals recommended for Australian Government investment in the short, medium and longer term can be found in Infrastructure Australia’s 2026 Infrastructure Priority List.

Ports Capacity and Connectivity

Australia’s economy is heavily dependent on international trade,4 with over 99 percent of this trade by volume moving through our maritime ports.5 Major ports underpin national productivity and global competitiveness, connecting producers, freight networks and markets.

Expanded and upgraded common-user infrastructure capacity and connectivity at ports is essential to address supply chain inefficiencies, accommodate increasing trade volumes, larger vessels and expanded range of commodities as ports seek to diversify in an environment of shifting international demand, global trade patterns and decarbonisation efforts.

Enabling infrastructure is essential to transform Australia’s marine precincts, ensuring they can support the delivery of complex maritime and defence projects. Infrastructure Australia has identified the following nationally significant infrastructure proposals as investment-ready priorities:

- Western Trade Coast enabling infrastructure – Henderson Precinct and Lefevre Peninsula growth infrastructure – Osborne Precinct, which are priorities for planning investment. These proposals support the transformation of existing maritime precincts in line with Australia’s AUKUS and naval shipbuilding commitments.

Targeted investment in common user infrastructure supports economic diversification by enabling new industries to deliver value for both regional and national economies. Infrastructure Australia has identified the following nationally significant infrastructure proposal as an investment-ready priority:

- Common user infrastructure at the Middle Arm Precinct - the Australian Government has committed $1.5 billion in equity to support construction of this proposal, which presents an opportunity to develop new industries that will increase export value and economic diversification. Further planning is required by the Northern Territory Government to define the full package of infrastructure and associated staging.

Improving both rail and road connectivity to ports will reduce freight bottlenecks and strengthen Australia’s supply chain performance. Infrastructure Australia has identified the following nationally significant infrastructure proposal as an investment-ready priority:

- Westport, which will enable transition of container trade from the Port of Fremantle to a new facility in Kwinana to support continued growth in container volumes on the Western Trade Coast. The Westport enabling infrastructure (Anketell Road Upgrades) proposal recognises that road, rail and intermodal terminal upgrades will be key enablers of the broader Westport Program, delivering essential port connectivity to support efficient access to new port facilities. Upgrading Anketell Road is the initial priority, with additional infrastructure works planned in coming years to further enhance the overall functionality of Westport.

Future strategic priorities for investment identified by Infrastructure Australia include:

- Long-term investments in port capacity, common-user infrastructure and modernisation, to address inefficiencies and ageing infrastructure, and accommodate increasing trade volumes, larger vessels, an expanded range of commodities and strategically significant port precincts.

- Targeted investment over the next decade in ports connectivity improvements, including addressing gaps in dedicated rail freight connectivity into major ports, to support further mode shift to rail to meet Australia’s growing freight task and reduce road congestion.

- Strengthening airport infrastructure to support national productivity, economic growth and global competitiveness, including improved airport rail connections for Australia’s major capital cities and improved fuel pipeline connectivity to major international airports.

More details on specific proposals recommended for Australian Government investment in the short, medium and longer term can be found in Infrastructure Australia’s 2026 Infrastructure Priority List.

Secure, Sustainable Water for Growth

Australia’s urban and regional water and wastewater infrastructure is under growing pressure from a rising population, expanding water-intensive industries, a shifting climate, ageing water assets and heavy reliance on climate-dependent water sources.

Regional and remote communities face persistent water security challenges, with variable climate conditions and limited infrastructure affecting reliability. Secure, sustainable and climate-independent water supplies are critical to meet growing and competing needs and address declining supply and reliability of surface and groundwater resources.

Investment in diverse water supply options from climate-independent sources is a national priority for sustainable and resilient water supplies for rapidly growing populations. Infrastructure Australia has identified the following nationally significant infrastructure proposal as an investment-ready priority:

- Darwin region water supply (Adelaide River Off-Stream Water Storage), which is a priority for investment in detailed planning activities. This proposal will provide additional water supply and storage capacity to the Darwin region over the long term, providing security for consumers, businesses and agricultural users.

Providing access to reliable water to support economic growth and industrial development opportunities is a national priority. This includes reliable water supply to meet growing demands from established water-dependent industries, such as agriculture, mining and manufacturing, and rapidly growing industries such as data centres that have significant demands for water consumption and supply reliability. Infrastructure Australia has identified the following nationally significant infrastructure proposals as investment-ready priorities:

- Paradise Dam improvement project – further investment, beyond the $600 million already committed by the Australian Government, to ensure the dam complies with safety regulations and remains safe and reliable to meet growing demand for productive agricultural use.

- Werribee water system reconfiguration – proposed upgrades to assets within the Werribee water system to support use of recycled water within the catchment’s irrigation districts. A secure, reliable and fit-for-purpose water supply will support increased productivity and climate resilience.

Future strategic priorities for investment identified by Infrastructure Australia include:

- Securing long-term reliability and security of water supply, as a critical enabler of industry investment and growth for water-intensive industries, including ensuring existing water supply assets remain safe, reliable and capable of supporting economic development.

- New or upgraded water supply, treatment, storage and distribution infrastructure, including solutions that reduce reliance on highly treated drinking water for all uses, to provide safe, secure, reliable water for communities and for economic growth and industrial development.

More details on specific proposals recommended for Australian Government investment in the short, medium and longer term can be found in Infrastructure Australia’s 2026 Infrastructure Priority List.

Enabling infrastructure to support prosperous, liveable and accessible communities

The Infrastructure Policy Statement states that the Australian Government will seek to invest in infrastructure projects that:

- improve the ability of Australians to move around their cities, towns and regions.

- reduce pressure on congested urban transport systems.

- link strategic planning, population and employment growth, the supply and availability of housing and land transport infrastructure investment.

The Australian, state and territory governments have set housing targets under the National Housing Accord and are investing significantly to increase supply. This requires a step change in housing delivery, addressing constraints around labour and materials, and investing in complementary enabling infrastructure including public transport, roads and utilities to unlock new housing development and increase density.

As the Australian Government’s independent adviser on nationally significant infrastructure, Infrastructure Australia has an important role in identifying opportunities to invest in enabling infrastructure to support housing growth.

Two of the five national infrastructure investment priorities identified by Infrastructure Australia are relevant to this challenge: high-capacity transport for growing cities, and secure, sustainable water for growth. This section recommends investment opportunities in these areas that should be considered as priorities for Australian Government investment in 2026.

High-Capacity Transport for Growing Cities

Australia’s transport networks connect people, places and opportunities across our cities and regions, supporting access to jobs, housing and essential services. Urban road networks are already seeing rising congestion and increasing freight movements, and mass transit must carry more of the passenger task in Australian cities.

Rapidly growing cities and suburbs face rising congestion and high reliance on private vehicles. High-capacity, multi-modal public transport, complemented by targeted urban road investments, bus and active transport networks, is needed to keep pace with and enable growth, unlock and support new housing, improve mobility, reduce emissions, and help shape more connected, liveable communities. Expanding high-capacity public transport, and optimising and upgrading existing networks, including high-capacity signalling, are national priorities. Opportunities to strengthen intercity passenger rail will also offer more sustainable travel options and reduced pressure on road and aviation networks.

Investing in expanded public transport networks in Australia’s largest capital cities – Melbourne, Brisbane, Sydney and Perth – is a priority. Infrastructure Australia has identified the following nationally significant infrastructure proposals as investment-ready priorities:

- Melbourne Suburban Rail Loop – East – the first stage of the Suburban Rail Loop is identified as a priority for investment, to support delivery of a rail connection between Cheltenham and Box Hill. This will reduce travel times, facilitate new housing and connect major employment, health, education and retail areas in Melbourne’s east and southeastern suburbs.

- The Wave (Sunshine Coast mass transit) – the proposal for a new passenger rail line between Beerwah and Birtinya and a proposed future bus rapid transit route connecting the new rail line with the Sunshine Coast Airport is identified as a priority for investment to provide high-capacity public transport services that support fast-growing suburbs on the Sunshine Coast and the Brisbane 2032 Olympic and Paralympic Games.

Enhancing intercity rail connections between capital cities and rapidly growing regional centres is a national priority. Infrastructure Australia has identified the following nationally significant infrastructure proposal as an investment-ready priority:

High Speed Rail – Newcastle to Sydney - the proposal for the high-speed rail connection between Newcastle and Sydney is an immediate priority for planning investment to support further analysis of housing objectives, investigations into funding strategies, and improved certainty of costs and benefits. This proposal aims to address connectivity challenges, rapid population growth, and housing pressures through one of Australia’s busiest regional corridors. The proposal is identified as the first stage of a future national high speed rail network.

Future strategic priorities for investment identified by Infrastructure Australia include:

- Expanding high-capacity public transport in Australia’s capitals and other major cities, including investment in passenger rail networks and other modes of public transport, enhancing multi-modal integration and improving access to mass transit.

- Continued investment in high-capacity signalling and complementary upgrades to stations and rail lines, to improve the capacity, efficiency and reliability of public transport networks, including replacing existing assets, signalling and train control systems with contemporary train control technologies to increase the frequency of rail services, reduce crowding and improve travel times.

- Strengthening intercity rail connectivity between rapidly growing regional cities and nearby capitals, and between major capital cities, including future stages of an east coast high speed rail network.

More details on specific proposals recommended for Australian Government investment in the short, medium and longer term can be found in Infrastructure Australia’s 2026 Infrastructure Priority List.

Secure, Sustainable Water for Growth

Australia’s urban and regional water and wastewater infrastructure is under growing pressure from a rising population, expanding water-intensive industries, a shifting climate, ageing water assets and heavy reliance on climate-dependent water sources.

Major cities need targeted investments to maintain existing and develop new water supply options, prevent water supply constraints on housing and economic growth and to ensure infrastructure keeps pace with increasingly complex treatment and contaminant challenges.

Ageing wastewater infrastructure can have significant impacts to the health of populations and the environment. Investment in upgrades to wastewater infrastructure is a national priority to meet contemporary standards and support housing development. Infrastructure Australia has identified the following nationally significant infrastructure proposals as investment-ready priorities:

- Launceston Sewerage Improvement Program - this proposal includes detailed investigations for a consolidated sewerage plant to meet environmental standards. The proposal supports population growth and housing development in Launceston.

- Bolivar Wastewater Treatment Plant capacity - the proposal aims to increase the capacity of the treatment plant and increase use of recycled water to improve the security and sustainability of water supply in Adelaide’s northern growth areas. The Australian Government previously committed $2.5 million in planning funding for a study that investigated options to augment the Bolivar Wastewater Treatment Plant, which led to subsequent investment in the related Northern Adelaide Irrigation Scheme project.

Future strategic priorities for investment identified by Infrastructure Australia include:

- Development of a diverse portfolio of water supply options, such as recycled and desalinated water in our cities and tailored innovative solutions for regional and remote areas, to accommodate growing populations and provide greater resilience of supply, including to pressures from climate-related factors.

- Capacity and technology upgrades of wastewater treatment plants and improvements to ageing wastewater infrastructure to support population and housing growth and address increasingly complex treatment challenges.

More details on specific proposals recommended for Australian Government investment in the short, medium and longer term can be found in Infrastructure Australia’s 2026 Infrastructure Priority List.

Enabling infrastructure to support net zero and sustainable approaches to transport and infrastructure

The Infrastructure Policy Statement states that the Australian Government will seek to invest in infrastructure projects that:

- enable the achievement of commitments to emissions reduction targets and net zero by 2050.

- support more efficient, affordable and sustainable modes of transport.

- decarbonise transport operations, including facilitating take-up of low or zero emission transport technologies.

- decarbonise transport infrastructure, including encouraging the use of lower emissions materials in construction.

Successful and timely delivery of clean energy infrastructure faces significant national and international challenges around enabling infrastructure and supply chains, which create barriers to the transition and put the achievement of net zero targets at risk. Infrastructure Australia’s national role and cross-sectoral remit makes us ideally placed to provide the national system-wide view to inform a coordinated approach and identify national priorities for enabling infrastructure, skills and supply chains needed to deliver.

As the Australian Government’s independent adviser on nationally significant infrastructure, Infrastructure Australia has an important role in identifying opportunities to invest in enabling infrastructure to support the energy transition.

Of the five national infrastructure investment priorities identified by Infrastructure Australia, the one relevant to this challenge is delivering net zero and a clean energy economy. This section recommends investment opportunities in this area that should be considered as priorities for Australian Government investment in 2026.

Delivering Net Zero and a Clean Energy Economy

Australia’s aims to cut emissions by 62–70% by 2035 and reach net zero by 20506 require a fundamental energy system transformation and the decarbonisation of construction and transport. The transition to net zero also brings opportunities for Australia to harness its renewable resources and build a competitive clean energy economy.

Achieving this requires replacing fossil fuels with rapid delivery of large-scale renewable generation supported by dispatchable storage, new and upgraded transmission networks, flexible gas capacity and enabling infrastructure. Reducing embodied carbon from infrastructure construction, maintenance and end-of-life phases of assets as well as operational and enabled emissions, such as those from road and rail transport, is also critical to achieving net zero.

Investments in batteries and deep storage are a key component to ensuring grid reliability and stability during periods of uncertain renewable supply. Infrastructure Australia has identified the following nationally significant infrastructure proposal as an investment-ready priority:

- The ACT renewable energy storage enhancement proposal to deliver Battery Energy Storage Systems in the ACT. Adding new firming capacity would help reduce the risk of power outages and load shedding in the National Electricity Market, which can have detrimental impacts on network equipment, leading to potential security and reliability issues for those connected to the electricity grid.

There is an opportunity for all states and territories to transition existing public bus fleets to zero emissions buses. This requires complementary upgrades to bus depot infrastructure. Infrastructure Australia has identified the following nationally significant infrastructure proposal as an investment-ready priority:

- Enabling infrastructure for NSW Zero Emissions Buses - Future stages - planning funding will enable definition of the enabling infrastructure required to support the deployment of zero-emissions buses across the state. The program involves upgrading existing depots, building new depots, and implementing smart technology to manage power draw from the grid.

Future strategic priorities for investment identified by Infrastructure Australia include:

- Continued support for net zero goals and future electricity demand, including renewable generation, short- and long-duration storage capacity, and flexible gas-powered generation supply infrastructure to back up renewables and support energy system stability.

- Coordinated planning and delivery of new and upgraded electricity transmission infrastructure networks for Australia’s major energy systems, including the National Energy Market, to connect new renewable generation storage infrastructure to electricity grids and support system stability and a reliable energy supply.

- Strategically important enabling infrastructure required to deliver the energy transition, including capacity and access at critical ports and upgrades to key freight corridors to allow for efficient transport of oversize, overmass energy project components and other freight needed for the timely delivery of renewable energy capacity.

- Decarbonisation of transport and infrastructure, including support for electrification of public transport fleets and domestic production of low-emission construction materials such as green steel.

More details on specific proposals recommended for Australian Government investment in the short, medium and longer term can be found in Infrastructure Australia’s 2026 Infrastructure Priority List.

_____

- Department of Infrastructure, Transport, Regional Development, Communications, Sport and the Arts, 2025, National Freight and Supply Chain Strategy, Australian Government, p. 13-14, available via: https://www.infrastructure.gov.au/infrastructure-transport-vehicles/transport-strategy-policy/freight-supply-chains/national-freight-supply-chain-strategy

- Department of Infrastructure, Transport, Regional Development, Communications, Sport and the Arts, 2025, National Freight and Supply Chain Strategy, Australian Government, p. 29, available via: https://www.infrastructure.gov.au/infrastructure-transport-vehicles/transport-strategy-policy/freight-supply-chains/national-freight-supply-chain-strategy

- World Bank 2024, Exports of goods and services (% of GDP) – Australia, accessed 6 January 2026, available via: https://data.worldbank.org/indicator/NE.EXP.GNFS.ZS?locations=AU

- Ports Australia 2024, State of Trade 2024,, p.3, available via: https://cdn.prod.website-files.com/64b93e7050a85c306292e4b7/66da8f4b7c00883379c6d117_Ports%20Australia%20State%20of%20Trade_Full%20Report.pdf

- Department of Climate Change, Energy, the Environment and Water 2025, Australia’s Net Zero Plan, Australian Government, Canberra, available via: https://www.dcceew.gov.au/sites/default/files/documents/net-zero-report.pdf

Considerations for infrastructure planning and delivery

The successful planning and delivery of infrastructure is critical in supporting our nation’s growing cities and regions, particularly as we navigate the growth in investment across renewable energy and social infrastructure projects, while continuing to deliver record levels of investment in major transport projects.

This next section highlights several critical considerations for the Australian Government when making new infrastructure investment decisions.

When considering new infrastructure investments, the Australian Government should continue to take account of:

- Market capacity for both labour and materials, with a focus on:

- Existing pressures on the infrastructure construction market, and prioritising investment in project planning, development and business case proposals for a sustainable pipeline.

- Existing and planned projects with similar and large material and labour needs – for example, mega projects and tunnelling projects, across different sectors.

- Existing and planned projects within a similar geographical area.

- Geographical limitations on material and labour supply, particularly in regional locations projected for significant demand growth. Regional demand is rising sharply, especially in Queensland, Northern Territory, South Australia, and New South Wales, with some regions expected to more than double current construction activity in the next four years.

- Engaging with jurisdictions to:

- Ensure an appropriate, sustainable balance of funding for nationally significant infrastructure between maintenance, renewal and investment in new infrastructure.

- Ensure oversight and coordination of the overall pipeline, particularly as the pipeline for energy, water and housing grows, to reduce potential cross-sector competition for resources and manage the risk of driving up costs and project delays.

- Ensure that proposals brought forward adequately consider resilience issues and address current and future climate-related risks and adaptations to infrastructure.

- Continue to embed consideration of emissions into infrastructure policy, planning and decisions, and implement measures to reduce embodied carbon in infrastructure. This includes implementing the Transport and Infrastructure Net Zero Roadmap and Action Plan across all levels of government to ensure the transport sector contributes fully to Australia’s emissions reduction goals.

- Explore ways to embed more innovation in infrastructure project delivery to unlock significant productivity gains across the construction sector.

Construction industry sustainability and market capacity constraints

Each year, Infrastructure Australia undertakes detailed analysis and demand projections of Australia’s national Major Public Infrastructure Pipeline (MPIP) as part of its Market Capacity program. The MPIP covers projects valued over $100 million in New South Wales, Victoria, Queensland and Western Australia, and over $50 million in South Australia, the Australian Capital Territory, the Northern Territory and Tasmania.

The MPIP is currently valued at $242 billion across the 5 years from 2024-25 to 2028-29. This represents a 14% increase in the last 12 months (compared to the demand projection last year for 2023-24 to 2027-28) and reflects governments’ ambitions to boost housing stock and transition our energy sources towards a net zero future, while holding steady the record levels of investment in productivity-enhancing transport infrastructure.

There is a significant increase in either public-funded housing investments or energy transmission projects across all of Australia’s states and territories. Delivery challenges are also slowing the rate of the energy transition, with delays to the start of construction for many private infrastructure energy projects. Industry reports approval delays and energy projects not materialising fast enough which may be causing investors to move offshore, firms to hold off investing in workforce capabilities, and global supply chains for energy being less interested in supplying to Australia. Governments could further accelerate the energy transition by providing industry with greater certainty about the forward energy pipeline. This could support more effective planning, investment, and capacity building across the supply chain.

Public spending accounts for 28% of the $1.14 trillion construction market, comprised of $242 billion (22%) planned on major projects (MPIP) and $66 billion (6%) on Small Capital Projects. Buildings (62%) dominate the total infrastructure pipeline, followed by transport (17%), utilities (16%) and resources (5%).

Infrastructure Australia’s 2025 Infrastructure Market Capacity report provides further analysis and advice.

Key changes in the Major Public Infrastructure Pipeline (MPIP) in the past 12 months include:

- Transport infrastructure investment is projected at $129 billion and remains the largest expenditure category, accounting for 53% of the MPIP. This is a $3 billion (2%) increase on last year’s outlook, indicating steady investment.

- Projected demand expected in the final year in the outlook period is much higher than observed in the first four editions of the Infrastructure Market Capacity reports. It indicates that government investment may be becoming more certain across a longer-term time horizon.

- Buildings infrastructure investment is projected at $77 billion, which accounts for 32% of the MPIP. This investment – driven by social and affordable housing ($28 billion) and health projects ($22 billion) – is up $6 billion on the previous year’s outlook (up $14 billion compared with the outlook from two years earlier).

- Utilities infrastructure investment is projected at $36 billion, which now accounts for 15% of the MPIP and is up $20 billion on the previous year’s outlook. This increase is largely due to additional electricity transmission line projects.

Peak workforce shortage could reach 300,000 as the sector faces both supply and skilling challenges

Labour remains the most critical delivery risk. After a brief easing in 2024, shortages are projected to surge and could reach 300,000 workers by 2027. Regional areas will be hardest hit, with shortages forecast to quadruple between 2025 and 2027.

Various pilots and initiatives by governments, industry and the training and education sectors are underway to address construction workforce challenges. National alignment and coordination across these initiatives, and boosting industry confidence in the energy pipeline, will help firms invest more in building future workforce and capabilities.

Materials cost escalations have stabilised, but more attention is needed to ensure sovereign capability in steel manufacturing and increase uptake of low emissions materials

Lower emissions and recycled materials remain a largely untapped pathway to reduce emissions in infrastructure delivery. A range of state and territory policies encourage the use of low-emission and recycled materials in infrastructure construction. This creates a strategic opportunity for governments to lead a nationally coordinated approach that strengthens market capacity and accelerates industry growth. Stronger procurement levers, harmonised standards, and pathways beyond research and pilots are needed to scale adoption and fully realise the decarbonisation potential on an industrial scale.

Productivity

Productivity in Australia’s construction sector remains persistently low despite a short-term rebound, with multifactor productivity rising 2.0% in 2023-2024 after a decline the year before. The long-term trend is flat and well below mid-1990s levels.

Two major national initiatives could drive change: the National Construction Strategy, commissioned by governments as part of the Infrastructure and Transport Senior Officials Committee, and the Blueprint for the Future endorsed by the National Construction Industry Forum in September 2025. While these initiatives mark promising first steps to addressing systemic productivity challenges for construction, their real impact will depend on how they are implemented and the concrete actions that follow.

Infrastructure Australia’s 2025 Infrastructure Market Capacity report highlights future opportunities, including that Governments could explore ways to embed innovation in infrastructure project delivery to unlock significant productivity gains across the construction sector. This could include:

- Exploring new incentives and investment models to cover the initial upfront cost of demonstrating new innovations on projects, which can then be scaled to wider national adoption and generate transformational productivity uplift across the sector.

- Leveraging government investments in large megaprojects or infrastructure programs with the scale, duration, and strategic importance is needed to effectively trial and embed productivity-enhancing innovations.

Delivering Net Zero

Infrastructure and buildings are one of our biggest contributors to emissions, responsible for nearly a third of Australia’s emissions and indirectly linked to more than half. Decarbonising these projects – from rail and roads to buildings and bridges – will be critical to reaching Australia’s net zero target.

Despite efforts by Australian, state and territory governments, current uptake of low emissions and recycled materials for infrastructure construction remains low. The development of the National Sustainable Procurement in Infrastructure Guideline provides transport agencies and infrastructure bodies with consistent, best-practice approaches to reduce embodied emissions through procurement and contracting.

Infrastructure Australia’s Delivering Net Zero Infrastructure: Workforce report identifies the roles, occupations and skills that currently contribute to reducing emissions across the asset lifecycle (across planning, design, construction, operations and maintenance) within the broader infrastructure workforce. The report found that only about half the workforce delivering Australia’s Major Public Infrastructure Pipeline are contributing to net zero outcomes – about 105,000 workers. Among this group, many lack the understanding and confidence on how to best decarbonise.

It marks a starting point from which governments and industry will need to accelerate workforce supply and capability efforts in pursuit of Net Zero Infrastructure by 2050. The Delivering Net Zero Infrastructure: Workforce report recommends that the Australian Government, working with state and territory governments, should:

- Coordinate actions to boost infrastructure workforce supply and skills uplift across key sectors (transport, energy and the built environment) and jurisdictions.

- Track capability of the infrastructure workforce to achieve net zero over time and monitor the progress, identifying emerging needs and future opportunities to boost supply and uplift capability.

Overview

- Australian Government Treasury, 2025, Australia’s Net Zero Transformation: Treasury Modelling and Analysis, Australian Government, Canberra, available via: https://treasury.gov.au/publication/p2025-700922

Secure, Sustainable Water for Growth

Ports Capacity and Connectivity

High-Capacity Transport for Growing Cities

High Productivity Freight Networks

Overview

Overview

2026 Infrastructure Priority List: 10-year priorities (consolidated)

Delivering Net Zero and a Clean Energy Economy