Annual Budget Statement 2024

Download a PDF of the full report or read the full report below

26 April 2024

Recommendation Summary

| Recommendation 1: | Prioritise investment in project planning, development and business case proposals to support a sustainable pipeline |

| Recommendation 2: | Prioritise proposals focused on better utilisation, maintenance and renewal of existing infrastructure assets alongside potential new investments to ensure a more sustainable investment mix |

| Recommendation 3: | Prioritise proposals that support decarbonisation and the circular economy |

| Recommendation 4: | Prioritise place-based infrastructure planning proposals |

Introduction and context

Purpose of this statement

As required under section 5DB of the Infrastructure Australia Act 2008 (Cth) (IA Act), Infrastructure Australia, during each financial year, must give to the Minister and table in both Houses of Parliament:

- an annual budget statement to inform the annual Commonwealth budget process on infrastructure investment; and

- an annual performance statement on the performance outcomes being achieved by states, territories and local government authorities in relation to the infrastructure investment program and existing project initiatives funded by the Commonwealth.

Context

In 2022, the Australian Government undertook an Independent Review of Infrastructure Australia. Following the release of the Government’s response to the Review, Parliament passed legislative amendments to the IA Act in December 2023. This included the requirement for Infrastructure Australia to produce and publish these annual statements.

With the passage of the amendments occurring late in 2023, the Annual Budget Statement 2024 was developed using readily available data within the time available.

The Annual Budget Statement 2024

This first edition of the Annual Budget Statement reflects on current infrastructure challenges and provides advice on the types of infrastructure proposals Infrastructure Australia recommends be considered during Budget processes. It considers recent observed trends both globally and in Australia, and evidence across infrastructure sectors, in particular for land transport. This advice is based on Infrastructure Australia’s own research, together with structured analysis of recent evidence from states and territories and the research community.

Future editions of the Annual Budget Statement will use Infrastructure Australia’s products, such as a targeted Infrastructure Priority List, to inform advice to Government on recommended projects for consideration in future Budget processes. Infrastructure Australia will also work with the Government to consider how broader Government reforms to infrastructure investment planning and decision-making and the availability of other data sources can inform future statements.

Key infrastructure challenges

Australia’s infrastructure networks and systems are vitally important. Secure and resilient infrastructure is critical to connecting people and businesses, powering the Australian economy and supporting communities in an increasingly unpredictable natural environment.

The environment in which infrastructure is planned, delivered and operated has changed significantly over time. Domestic and global challenges such as climate change and extreme weather events, global availability of resources and materials and changing movement patterns can create an environment of risk and uncertainty.

However, there are significant opportunities to evolve our approach to infrastructure planning, delivery and operation. Development of new technologies, increased use and access to data, modern methods of construction and a greater focus on renewables and recycled materials can transform our infrastructure system and assist in overcoming the challenges we currently face.

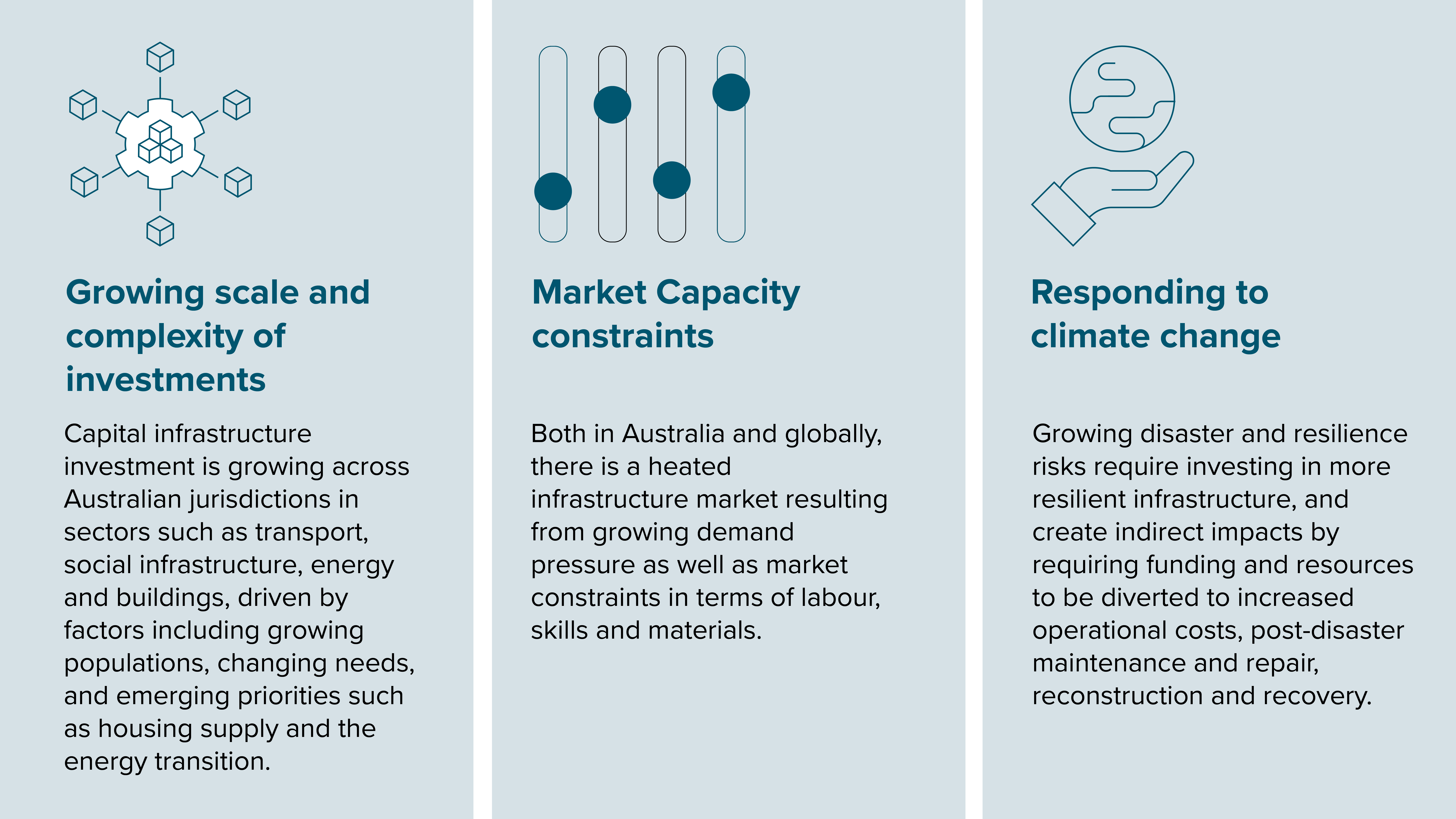

Figure 1: Key infrastructure challenges

Growing scale and complexity of infrastructure investments

Capital infrastructure investment is growing across Australian jurisdictions in sectors such as transport, social infrastructure, energy and buildings, driven by factors including growing populations, changing needs, and emerging priorities such as housing supply and the energy transition.1,2,3

There is also clear global and jurisdictional evidence of a trend towards an increasing number and scale of ‘megaprojects’ (cost over $1 billion) in recent years.4,5,6,7,8

This growth in spending has ramifications for project delivery across infrastructure sectors in terms of cost and risk, and longer-term ramifications due to a growing asset base and maintenance liability.

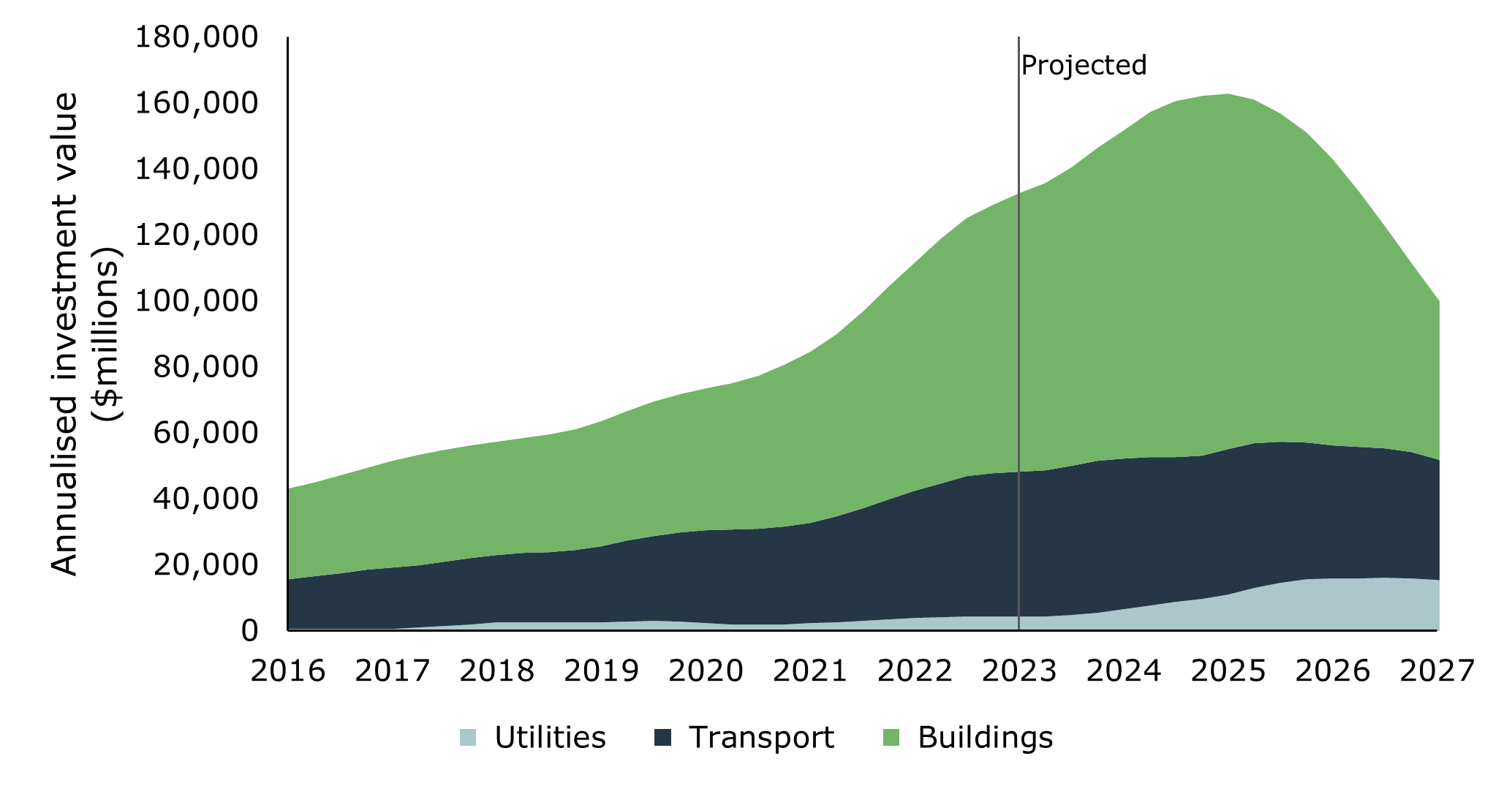

Figure 2 illustrates the significant increase in combined public and private sector infrastructure investments over recent years and the scale of the forward pipeline. The 5-year, $690 billion combined pipeline comprises building and transport investments of $427 billion and $210 billion respectively, and a further $53 billion utilities pipeline that includes an expected four-fold increase in energy investments over the next four years. This rapid growth in energy projects will need to compete for resources despite being overshadowed by building and transport investments.

Figure 2: Combined Infrastructure (public and private sector) - annualised investments by sector.

Source: Infrastructure Australia (2023).

Notes:

- Buildings: includes non-residential buildings for health, education, sport, justice, transport buildings (e.g., parking facilities and warehouses), other buildings (art facilities, civic/convention centres, and offices), limited coverage of detached and semi-detached residential buildings.

- Transport: includes roads, railways, level crossings and other transport projects such as airport runways.

- Utilities: includes water and sewerage, energy and fuels, gas and water pipelines, and telecommunications.

Figure 3: Recent trends in Australia’s public infrastructure investment across sectors

There are signals of shifts in investment trends. For example, Infrastructure Australia’s research indicates that energy sector investment is expected to grow nationally at around four times current activity levels.9

Jurisdictions such as Queensland are also seeing significant uplifts in energy sector funding.2

There are also indications of a greater balance of investment across sectors going towards regional areas. Infrastructure Australia’s 2023 Market Capacity Report indicates that regions across NSW, Queensland, and the Northern Territory will experience extraordinary growth in the three years from 2024-25, with investment up to three times higher than the three years prior in some regions.9

Market capacity constraints

Both in Australia and globally, there is a heated infrastructure market resulting from growing demand pressure as well as market constraints in terms of labour, skills and materials.10

Sustained Demand

Australia will continue to see prolonged pressure on construction capacity because of sustained cross-sectoral demand.

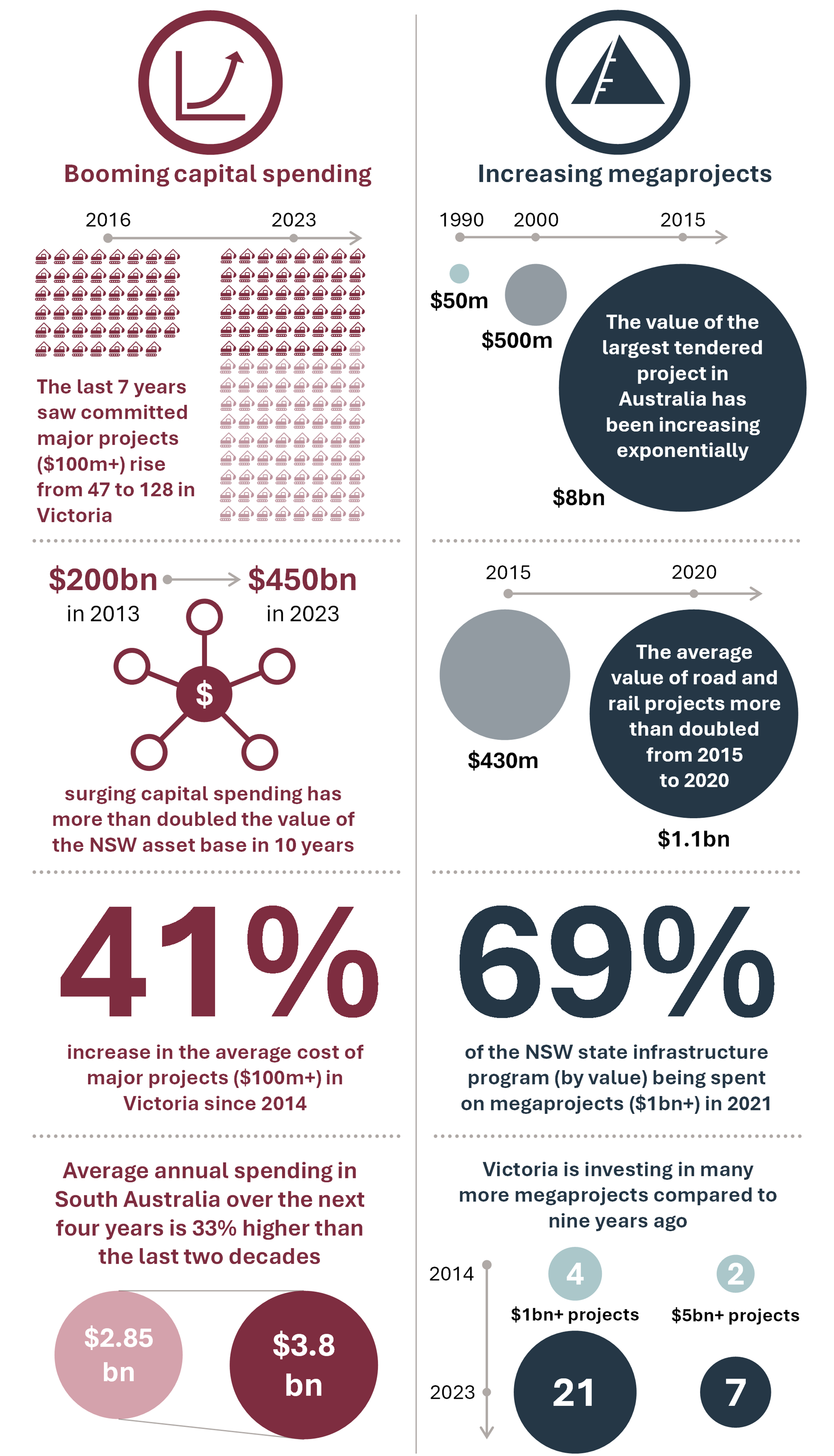

This includes uplifts in overall capital spending and/or accelerated delivery (where capital expenditure is brought forward to earlier than originally planned). In NSW, the number of projects in the state’s infrastructure program increased by 4.8% year-on-year in 2022-23, while increasing numbers of megaprojects are also moving into delivery, putting pressure on the market’s capacity to deliver (both globally and locally) and leading to cost increases on projects.11,1 Queensland has also seen substantial increases in overall infrastructure project costs, partly resulting from the accelerated delivery of capital projects such as rail and highway upgrades.2

Governments are recognising and acting to manage demand challenges, in both the short and longer term, for example through:

- Proactive management and re-sequencing of projects in response to market constraints – such as the Australian Governments review of the Infrastructure Investment Program (IIP), the NSW Government’s 2023 Strategic Infrastructure Review and the WA Government’s measures to smooth procurement and delivery of projects to align to industry capacity.

- Improving visibility, transparency and detail of information on planning infrastructure projects and procurement – such as the Major Projects Pipeline Portal in NSW, the Infrastructure Projects in Western Australia report and Tasmania’s 10-year Infrastructure Pipeline database.

- Recognising a need to shift the balance away from large-scale capital projects towards a more sustainable investment mix, including greater emphasis on utilisation and maintenance of existing assets to maximise spare capacity and optimise outcomes.

In an environment of increasing demand pressure, factors such as rising material costs, disrupted or under-supply of materials, labour and skill shortages in the construction industry, and increasing labour costs have been identified by multiple Australian jurisdictions as a major cause of cost increases and delays to the delivery of infrastructure projects and represent an ongoing challenge.8,12,13,2

Labour Constraints

Infrastructure Australia’s 2023 Market Capacity Report demonstrates that labour remains the top capacity constraint. Labour supply capacity is expected to recover to pre-COVID levels by mid-2024 and to continue to increase steadily. However, the expected rate of supply increase is not projected to close the construction sector’s labour gap indicating longer-term structural barriers. Further, the Report asserts the workforce must continuously upskill to keep pace with evolving job designs and ways of working, and that improving workplace culture in construction overall will unlock productivity benefits. However, a range of cultural problems such as inflexible and extended working hours, lack of diversity in teams and mental health issues, are reported to hinder women’s participation in the sector and increasingly, that of young men. Many of these issues may be addressed through reforms outlined by the Australian Government in recent months (see below).9

Key Australian Government reforms addressing structural barriers to labour capacity and productivity include:

- Working Future – The Australian Government’s White Paper on Jobs and Opportunities – a roadmap with aims which include achieving sustained full employment, promoting job security and reigniting productivity growth

- Australian Universities Accord – to improve the quality, accessibility, affordability and sustainability of higher education.

- National Skills Agreement – designed to strengthen the vocational education and training (VET) sector focused on addressing critical skills and workforce shortages.

- Australian Government Migration Strategy – address skills shortages, improve pathways, and enhance the overall migration experience.

- Build Skills Australia – the national Jobs and Skills Council for the built environment sector identifying solutions to the workforce challenges facing the construction, property and water industries.

- Australian Skills Guarantee – to introduce new national targets for apprentices, trainees and paid cadets working on Australian Government funded major projects, as well as introduce national targets for women to increase the proportion of women working on major projects.

Significant levels of public investment in priority growth areas such as energy, housing, heavy industries, and defence, will also compete for access to human resources. Our latest Market Capacity analysis indicates a shortage of 229,000 full-time infrastructure workers as of October 2023, with shortages in all occupational groups. These shortages are driven by heightened activity in public and private infrastructure investments. Labour demands total 405,000 full-time infrastructure workers, with transport accounting for 56% of total labour demand, buildings 34%, and utilities the remaining 10%. Further, extraordinary growth in public and private investments are expected to create labour gaps in coming years in some regional hot spots. The top five regional hot spots are Murray, mid-North Coast and the Riverina in NSW, the NT outback and central Queensland.

Materials Constraints

Industry research indicates concerns that the domestic capacity of materials supply – particularly steel and quarry products – cannot meet demand in particular hotspots.9 Acute quarry shortages loom in a few hotspots across the country, notably Melbourne, mid-North Coast NSW and South East Queensland. Quarry materials are important to a range of infrastructure projects including roads, bridges, houses, railways and other infrastructure. Projects carry the risk of higher transportation costs, vehicle emissions and schedule delays if forced to source quarry materials from further afield.

A focus on productivity

Productivity in the construction sector has not improved for over 30 years. This is partly due to the absence of diagnostic productivity measures, low participation of women in the workforce, inconsistent adoption of new technologies and modern manufacturing methods, and unfair risk allocation in procurement and contracting.

State and territory governments have initiated or are in the process of implementing reforms to increase industry productivity. However, joint effort by all governments is necessary to support ongoing work and raise reform outcomes to the national level. This effort should focus on developing diagnostic productivity measures, establishing a national productivity baseline, and creating national metrics and indicators to track progress. Regular progress reporting against these measures should be provided to relevant intergovernmental forums and/or Ministerial Councils.

Responding to climate change

Climate change impacts such as extreme weather, fires and floods are directly impacting existing infrastructure across sectors and jurisdictions and represent a significant and growing risk to assets, systems and user outcomes. There is growth in the frequency and intensity of these impacts, and this poses episodic but extreme risk to both developing infrastructure and existing assets.14

Increasing disaster and resilience events require investment in more resilient infrastructure, and create indirect impacts by requiring funding and resources to be diverted to increased operational costs, post-disaster maintenance and repair, reconstruction and recovery. As jurisdictions such as South Australia and New South Wales have observed, this places significant added pressure on already-constrained public finances as well as on market capacity for infrastructure delivery.17,7

As identified by Infrastructure Western Australia in their State Infrastructure Strategy, considering resilience not only includes a focus on the resilience of an individual infrastructure asset, but also the contribution that piece of infrastructure makes to resilience of the community overall.15 Fundamental to this is an understanding of likely future climate change impacts, auditing of existing infrastructure systems, adequate planning, along with appropriate consideration of resilience in existing and new infrastructure projects and networks.

Similarly, infrastructure planning, investment and design decisions need to be in step with national goals for decarbonisation and the circular economy. To date, the transition to more sustainable approaches to infrastructure, such as adoption of recycled materials as well as efforts to minimise embodied carbon through project delivery, has been slow and inconsistent.

For example, approximately 43% of conventional materials used in road construction could be replaced by a range of recycled materials. Cost savings from the application of recycled alternatives in roads infrastructure range from 2% to 83%. Supporting the increased uptake of recycled materials in construction can help to lower project costs, and support Australia’s decarbonisation efforts to reach Net Zero by 2050.

Efforts to reduce embodied carbon would make a significant contribution to Australia’s decarbonisation agenda. This can be achieved through the decarbonisation of building materials on the supply side, and changes in how Australia plans, designs and procures assets so that embodied carbon is considered early. Research by Infrastructure Australia shows that low carbon building materials and construction methods have the potential to achieve a 23% saving of upfront carbon from the public infrastructure pipeline over the next five years.

Other infrastructure delivery challenges

- Increasing risks for project development and delivery due to complexity, emerging technologies and integration with existing operations and other systems and sectors.

- Ensuring appropriate timing and engagement for planning and environmental approval processes, including community engagement.

Key implications for infrastructure investment

Risks to on-time, on-budget delivery

Infrastructure Australia’s 2021 National Risk Study highlighted that, both globally and in Australia, larger projects are more likely to face increased risks, costs and schedule overruns.14 This is reinforced by global research, which demonstrates that:

- Projects across sectors (including land transport, water and energy) experience average cost increases of between 10-39% from announcement to delivery, and these levels of cost overrun have changed little over time.16,11

- Most (86%) major transport infrastructure projects experience cost increases or delays.17

- Cost increases on land transport projects are common and significant across modes, project types and project sizes, with over half (53%) of major transport projects exceeding initial estimated costs. Rail projects generally perform worse, with 73% exceeding costs compared to 43% of road projects.11

- Delays to transport projects typically range from 7-33% compared to original plans, while 35% experience delays of more than six months, with delays a key contributing factor for many cost overruns.18,11

The performance of infrastructure projects in Australia is broadly in line with these global trends. Australian studies indicate that the average cost increases on transport infrastructure projects in Australia typically range from around 12-52%.19,20,21 This is reinforced by evidence from Australian jurisdictions. For example:

- A 2023 review of 20 major infrastructure projects in Western Australia shows total cost increases of almost $2 billion (22.5%) compared to original budgets, with 14 projects exceeding budgeted costs by 10% or more and four seeing costs more than double.12

- In New South Wales, cost escalation was reported as a major contributing factor for 15% of underperforming Tier 1 projects.1

- Self-assessments by Victorian agencies indicate 13% of major projects face cost increases of 11-20% over budget, with 4% of projects expecting more than 20% increases. 28 out of 101 projects included in a Victorian review saw total estimated project investment increase by over 10%, and costs on 12 projects rose by more than 50% over original estimates.8

The evidence is clear that major infrastructure projects, irrespective of their types, sectors and locations, often experience cost increases and delivery delays. Infrastructure Australia’s 2021 National Risk Study highlighted key strategies in the planning, scoping and development of projects to manage these risks and their underlying causes, including:

- early engagement with contractors

- streamlined planning approvals

- avoiding premature project announcement of solutions, budgets and timeframes

- more in-depth investigations and use of early works packages.

The need for a sustainable investment mix

Increased risks associated with megaprojects

The trend towards an increasing number and scale of ‘megaprojects’ (described earlier) adds to the risk in governments’ infrastructure portfolios because of their size, complexity and greater exposure to risk.4,7

Across sectors, megaprojects consistently exceed cost and time estimates to a greater degree than other lower value projects that experienced overruns.11 This global evidence is reinforced by recent infrastructure delivery trends observed in Australian jurisdictions.8,7

The increased risks associated with megaprojects are partly due to their unique characteristics. In particular, these issues relate to higher complexity – including planning and delivery within dense, built-up areas with extensive existing infrastructure, as well as challenges in the investment planning process – and longer project timeframes, resulting in greater exposure to cost and schedule risk.4,1,11

The trend towards increasingly large and complex infrastructure projects also has implications for the complexity of procurement and contracting processes. This trend is observed internationally, leading to greater prevalence of adversarial engagements and issues with risk transfer during delivery, impacting project delivery costs and delays.11 In recent years, states and territories have reported similar challenges with procurement and contract management processes as factors impacting on costs, timeframes and delivery confidence of infrastructure projects.12,1

Megaprojects in sectors such as transport can also represent much more complex, multi-dimensional urban development and renewal interventions than more typical road or rail infrastructure projects. This complexity can make approaches to investment planning, appraisal and business case development more challenging for agencies based on standard guidelines.

At the same time, international research shows that integrated planning, business case assessments and front-end due diligence are some of the most important areas for improving the performance of megaprojects.4 In NSW, key identified causes of increased megaproject risks also include unclear project roles and responsibilities and inadequate approaches to risk management and procurement.1

Growing maintenance liabilities and ageing assets

Some jurisdictions indicate a growing challenge with ageing assets. The Queensland Audit Office reports that estimated actual capital expenditure across all agencies in Queensland was 14% higher than expected in 2022-23, in part due to additional costs required to maintain ageing infrastructure in the energy sector, as well as rising supply costs and severe weather events.2 Infrastructure NSW’s State of Infrastructure Report 2022-23 indicates that all infrastructure sectors in NSW reported issues with ageing assets, with evidence that more ageing assets are linked to an increase in high-risk safety incidents, maintenance challenges and impacts on service delivery.7

In addition to a growing challenge, understanding the problem at hand is another concern. Infrastructure WA notes that asset management practices, for the state’s approximate $159 billion asset base, varies considerably across government. This presents a challenge in determining both the size and cost of the backlog in maintenance across the state. Infrastructure WA also found that the variability of reported maintenance expenditure is suggestive of a large amount of reactive maintenance.15

Recommendations for future infrastructure investments

Australian governments will play a critical role in meeting the challenges outlined above. As a major planner, funder, procurer and owner of infrastructure, governments have an important role in ensuring that infrastructure investments help to progress broader national goals and objectives, such as decarbonisation, waste action and improving productivity.

Productivity growth has slowed over the past decade in Australia.22 Infrastructure investments can support productivity and economic growth by improving the efficient movement of freight and people, increasing a network’s reliability and/or resilience, and reducing ongoing maintenance costs. Infrastructure Australia recommends that the Australian Government considers productivity benefits at the early stages of project planning and ensures that productivity-enhancing proposals form the majority of its investment portfolio.

Taking appropriate time to plan and select the right mix of infrastructure investments will improve the ability of governments to take these broader objectives into consideration.

For example, an appropriate mix of build and non-build investments can deliver greater capacity in our infrastructure with less resources, balance portfolio risk, support meeting Australia’s climate targets and assist with addressing significant market capacity demand. An important enabler to this is ensuring the consideration of a range of options when considering infrastructure interventions. Conversely, a portfolio comprising a large proportion of megaprojects can significantly increase risk and the likelihood of

cost overruns.

In concluding the 2024 Annual Budget Statement, Infrastructure Australia makes the following recommendations for the Australian Government to consider in determining and prioritising projects for investment.

Recommendation 1

Recommendation 1: Prioritise investment in project planning, development and business case proposals to support a sustainable pipeline

Infrastructure Australia encourages the Australian Government to keep in mind existing pressures on the infrastructure construction market when contemplating new and additional investments in infrastructure. This includes considering:

- the relative priority of the Australian Government’s infrastructure investments across sectors, such as housing, energy and transport, which are often competing for the same construction resources.

- the impact and timing on existing commitments in considering any potential new investments, especially in regions with identified ‘hotspots’ in terms of labour and materials supply challenges.

As infrastructure construction market demand still significantly outweighs supply, active demand management will be an ongoing area for action. Governments will need to remain vigilant and discerning in their infrastructure spend, in the face of budget and inflationary pressures over the short to medium term.

Infrastructure Australia is very supportive of government-led demand management initiatives such as the Australian Government’s recent review of the IIP to ensure the right projects are prioritised for funding and delivered at the right time.

With this in mind, and coupled with the priority of a sustainable, deliverable infrastructure pipeline, Infrastructure Australia recommends the Australian Government continues to work with jurisdictions, across all sectors, to prioritise the development of planning and business case proposals for consideration in the next Budget process.

This will assist in both managing existing market capacity constraints and ensuring that infrastructure proposals delivered in future are robustly scoped and costed, reducing the risk of scope changes and cost increases. It also assists in developing a clear, well-planned pipeline of work for the market to respond to and is particularly important to appropriately manage the increased risk associated with megaprojects outlined above.

In relation to land transport infrastructure, this approach also aligns with recommendations in the Government’s Independent Strategic Review of the IIP and the Independent Review of the National Partnership Agreement on Land Transport Infrastructure Projects.

Recommendation 2

Recommendation 2: Prioritise proposals focused on better utilisation, maintenance and renewal of existing infrastructure assets alongside potential new investments to ensure a more sustainable investment mix

The evidence of a growing imbalance towards capital expenditure over asset maintenance and renewals is a significant concern to the long-term financial sustainability of managing the existing asset base and the continued ability of infrastructure assets to serve the needs of the community.

Optimising current assets and networks can be a more efficient and cost-effective method of meeting current and future needs than constructing new expensive, long-lived assets that further add to the growing whole-of-life costs of asset portfolios and increase pressure on the market’s capacity to deliver. Ensuring an appropriate investment mix can assist in managing the infrastructure portfolio risk profile, derive lower cost solutions, lessen market capacity constraints and assist in reducing greenhouse gas (GHG) emissions.

Infrastructure Australia recommends that the Australian Government work with jurisdictions to prioritise development of proposals focused on better utilisation, maintenance and renewal of existing infrastructure assets alongside potential new investments. This includes potential enhancements required to improve the resilience of existing infrastructure assets.

Recommendation 3

Recommendation 3: Prioritise proposals that support decarbonisation and the circular economy

Infrastructure is a key contributor to Australia’s GHG emissions footprint. It is estimated that 70% of Australia’s emissions are directly attributable to or influenced by infrastructure.23 Decarbonising infrastructure presents opportunities to reduce costs and improve productivity through design choices that minimise or avoid emissions, and through the use of low carbon and recycled materials.

To meet Australia’s emissions reduction targets, governments must integrate decarbonisation into business-as-usual infrastructure processes. This includes reducing the embodied carbon intensity of public infrastructure projects, the emissions associated with materials and construction and throughout an asset’s lifecycle, across all sectors.

Governments can leverage their purchasing power to create circular economy supply chains and lower the adoption costs of recycled and low emissions building materials. By encouraging innovation in construction practices and use of low emissions materials, governments can help make these materials more viable substitutes for use in the private sector.

In support of driving more sustainable approaches to infrastructure, Infrastructure Australia recommends the Australian Government prioritise new investments that clearly demonstrate an aim to maximise, where appropriate, the proportion of recycled materials used in project design and construction, as well as potentially recycling or reusing materials during the project’s lifecycle.

Recommendation 4

Recommendation 4: Prioritise place-based infrastructure planning proposals

Infrastructure Australia supports the Government’s commitment to place-based, corridor and precinct planning through mechanisms such as the regional and urban Precinct and Partnerships programs and reforms to the IIP. It is recommended that the Australian Government continues to provide funding to projects and programs with a place-based, corridor or precinct focus.

Coordinated cross-sectoral planning across all levels of government is critical for the Australian Government to be able to identify ‘investments that ensure the planned development of cities and suburbs and regions by linking strategic planning, population growth, the supply and availability of housing and land transport infrastructure investment’ which forms part of the Australian Government’s Infrastructure Policy Statement.

For example, understanding the new or upgraded enabling infrastructure required to support the 1.2 million homes to be delivered under the National Housing Accord, such as transport, water communications and community facilities, will be critical to achieving the shared ambition of well-located, affordable homes.24

In addition, in an era of increasing investment in megaprojects, strategic planning can ensure that these significant investments are delivered in the right place and at the right time, sequenced appropriately, manage community disruption appropriately and maximise their wide-ranging benefits to the community.

This will be important for geographical locations where multiple government investments are being considered to facilitate different government priorities. For example, a geographical location earmarked for critical minerals development will also need to consider enabling infrastructure such as energy, communications, transport and potentially housing.

References

- Infrastructure NSW 2022, Trends and Insights Report 2022, NSW Government. Available via: https://www.infrastructure.nsw.gov.au/investor-assurance/project-assurance/resources/trends-and-insights/

- The State of Queensland (Queensland Audit Office) 2023, Major Projects 2023 (Report 7: 2023–24). Available via: https://www.qao.qld.gov.au/sites/default/files/2023-12/Major%20projects%202023%20%28Report%207%20%E2%80%93%202023%E2%80%9324%29.pdf

- Victorian Auditor-General’s Office 2022, Quality of Major Transport Infrastructure Project Business Cases: Independent assurance report to Parliament 2022-23:5. Available via: https://www.audit.vic.gov.au/sites/default/files/2022-09/20220921%20Business%20Cases_0.pdf

- Ninan, J., Clegg, S., Burdon, S., and Clay, J. 2023, Reimagining Infrastructure Megaproject Delivery: An Australia—New Zealand Perspective. In: Sustainability 15, no. 4: 2971. Available via: https://doi.org/10.3390/su15042971

- Ryan, P. and Duffield, C. 2017, Contractor Performance on Mega Projects–Avoiding the Pitfalls. Mahalingam, A (Ed.) Shealy, T (Ed.) Gil, N (Ed.) pp.1-34. Engineering Project Organization Society. The University of Melbourne, Melbourne, Australia. Available via: http://hdl.handle.net/11343/168246

- Terrill, M., Emslie, O., & Moran, G. 2020, The rise of megaprojects: counting the costs. Grattan Institute. Available via: https://grattan.edu.au/wp-content/uploads/2020/11/The-Rise-of-Megaprojects-Grattan-Report.pdf

- Infrastructure NSW 2023, 2022-23 State of Infrastructure Report, NSW Government. Available via: https://www.infrastructure.nsw.gov.au/investor-assurance/asset-management-assurance/resources/soir/

- Victorian Auditor-General’s Office 2023, Major Projects Performance Reporting 2023: Independent assurance report to Parliament 2023-24:9. Available via: https://www.audit.vic.gov.au/sites/default/files/2023-11/20231130_Major-Projects-Performance-Reporting-2023.pdf

- Infrastructure Australia 2023, Infrastructure Market Capacity 2023 Report. IA, Sydney. Available via: https://www.infrastructureaustralia.gov.au/sites/default/files/2023-12/IA23_Market%20Capacity%20Report.pdf

- Boston Consulting Group (BCG) 2021, International Major Infrastructure Projects Benchmarking Review: Final Report. Prepared by BCG for the Office of Projects Victoria (OPV). Available via: https://content.vic.gov.au/sites/default/files/2023-02/International-Major-Infrastructure-Projects-Benchmarking-Review.pdf

- Infrastructure NSW 2023, Annual Report 2022-23, NSW Government. Available via: https://www.parliament.nsw.gov.au/tp/files/187101/INSW Annual Report 2023.pdf

- Office of the Auditor General (Western Australia) 2023, 2023 Transparency Report: Major Projects, Report 6: 2023-24. Available via: https://audit.wa.gov.au/reports-and-publications/reports/2023-transparency-report-major-projects/

- Infrastructure SA 2023, Capital Intentions Statement 2023. Available via: https://www.infrastructure.sa.gov.au/our-work/capital-intentions

- Infrastructure Australia 2021, A National Study of Infrastructure Risk: A report from Infrastructure Australia’s Market Capacity Program. IA, Sydney. Available via: https://www.infrastructureaustralia.gov.au/sites/default/files/2021-10/A%20National%20Study%20of%20Infrastructure%20Risk%20211013a.pdf

- Infrastructure Western Australia 2022, Foundations for a Stronger Tomorrow State Infrastructure Strategy. Available via: https://prod-iwa-public-files.s3.ap-southeast-2.amazonaws.com/public/2022-07/strategy_download/2022 Final SIS.pdf

- Flyvbjerg, B. 2016, The Fallacy of Beneficial Ignorance: A Test of Hirschman’s Hiding Hand. In: World Development, Vol. 84, Available via: https://ssrn.com/abstract=2767128

- Flyvbjerg, B., Holm, M. and Buhl, S. 2002, Underestimating Costs in Public Works Projects: Error or Lie? In: Journal of the American Planning Association, Vol. 68, No. 3,pp 279-295. Available via: https://ssrn.com/abstract=2278415

- Flyvbjerg, B., Holm, M. and Buhl, S. 2004, What Causes Cost Overrun in Transport Infrastructure Projects? In: Transport Reviews, vol. 24, no. 1, January 2004, pp 3-18. Available via: https://doi.org/10.1080/0144164032000080494a

- Duffield, C., Raisbeck, P. and Xu, M. 2008, Report on the performance of PPP projects in Australia. In: Construction Management and Economics, 28:4, pp 345-359. University of Melbourne. Available via: https://doi.org/10.1080/01446190903582731

- Love, P., Wang, X., Sing, C.-P. and Tiong, R. 2013, Determining the Probability of Project Cost Overruns. In: Journal of Construction Engineering and Management 139.3, pp. 321–330. Available via: https://doi.org/10.1061/(ASCE)CO.1943-7862.0000575

- Terrill, M. and Danks, L. 2016, Cost overruns in transport infrastructure. Grattan Institute. Available via: https://grattan.edu.au/wp-content/uploads/2016/10/878-Cost-overruns-on-transport-infrastructure.pdf

- Commonwealth of Australia 2023, Working Future. The Australian Government’s White Paper on Jobs and Opportunities. Available via: https://treasury.gov.au/sites/default/files/2023-10/p2023-447996-working-future.pdf

- ClimateWorks Australia 2020, Reshaping Infrastructure for a Net Zero Emissions Future. ClimateWorks Australia, Victoria. Available via https://www.climateworkscentre.org/resource/issues-paper-reshaping-infrastructure-for-a-net-zero-emissions-future/

- The Treasury 2022, Delivering the National Housing Accord. Australian Government, Canberra. Available via: https://treasury.gov.au/housing-policy/accord

-

Annual Statements

Find out more about the Annual Statements here

-

Annual Performance Statement 2024

Read the Annual Performance Statement 2024 here