2024 Infrastructure Market Capacity Report

23 December 2024

Chief Commissioner’s Foreword

With Australia’s infrastructure boom far from over, our Infrastructure Market Capacity research will be more important than ever in supporting governments and the infrastructure industry to navigate supply and demand as they deliver our nation’s pipeline.

For years, demand has been far outweighing supply leading to cost increases and project timelines being delayed.

While this year we find demand to be easing, it’s clear there is more work to do, with skills shortages and cost escalations persisting.

These challenges are not unique to Australia. You only need to look at the skills shortages Europe is grappling with in delivering its renewable energy transition, or the challenges Canada is facing to deliver more housing as proof points that we are not alone.

Now in its fourth year, our Infrastructure Market Capacity research has grown into a trusted and reliable source of information that captures the $1.08 trillion of construction activity happening right across the country. The report also continues to detail and explore the plant, labour, equipment and materials needed to deliver on the nation’s five-year Major Public Infrastructure Pipeline, which now stands at $213 billion.

The strength of this research lies in the collaborative relationships Infrastructure Australia has formed across industry and government. We acknowledge and thank all participants for the part they played in developing this year’s report, through data sharing and close collaboration.

Infrastructure underpins the growth of our economy – it supports the productivity and liveability of our nation.

The successful planning and delivery of infrastructure is critical in supporting our nation’s growing cities and regions, particularly as we navigate the growth in investment across renewable energy and social infrastructure projects, while continuing to deliver record levels of investment in major transport projects.

As governments grapple with these critical decisions, Infrastructure Australia is committed to supporting the Australian Government with the independent advice it needs to drive a thriving, efficient and productive construction sector for the economic and social prosperity of all Australians.

Tim Reardon

Infrastructure Australia

Chief Commissioner

Executive summary

Australia’s Major Public Infrastructure Pipeline is $213 billion across the 5 years from financial years 2023–24 to 2027–28 (‘five-year outlook’), down 8% compared with the projection of 12 months earlier for the corresponding outlook period 2022–23 to 2026–27. This outcome represents a significant management of demand by governments across Australia to reduce the gap between supply and demand, however demand continues to outstrip supply overall.

Transport continues to dominate demand with growth in buildings and utilities, while investment gradually shifts north across all three sectors

Infrastructure Australia has updated its Market Capacity database with relevant major public infrastructure project pipeline information provided by state and territory governments. A comparative analysis of the national Major Public Infrastructure Pipeline outlook versus the previous outlook period from 12 months earlier reveals:

- There is a significant geographical shift in investment to the north, with Queensland and Northern Territory major public infrastructure pipelines growing by $16 billion, while New South Wales and Victoria have reduced by $39 billion versus the previous outlook period.

- The projected increase in demand for these northern areas would intensify local supply constraints, especially in regional areas where attracting skilled workers is challenging. It is also difficult to source construction materials, plant and equipment due to their geographical distance, adding risk to on-time, on-budget project delivery.

- A jump in labour demand from the private infrastructure sector is observed over the next five years. This is driven by the renewable energy transition. Workforce preparedness is needed to deliver private-funded infrastructure demand.

Key changes in the Major Public Infrastructure Pipeline across the past 12 months include:

- Transport infrastructure investment is projected at $126 billion and remains the largest expenditure category, accounting for 59% of the Major Public Infrastructure Pipeline. This is a $32 billion reduction on the previous year’s outlook, driven by:

- Completions of megaprojects in 2023–24.

- Fewer new projects to commence in coming years versus the previous outlook period.

- Cost and schedule changes in the total investment estimates for some megaprojects due to commence construction in the outlook period.

- Buildings infrastructure investment is projected at $71 billion, which accounts for 34% of the Major Public Infrastructure Pipeline and is expected to peak in late 2026. This is up $8 billion on the previous year’s outlook. Buildings infrastructure is driven by health ($24 billion) and residential buildings ($17 billion), followed by other building types ($12 billion), such as convention centres, offices, art facilities and laboratories.

- Utilities infrastructure investment is projected at $16 billion, which accounts for 7% of the Major Public Infrastructure Pipeline and is made up predominantly of renewable energy and transmission line projects. This is up $6 billion on the previous year’s outlook.

Growth of the building and utilities sectors reflect governments’ ambitions to boost housing stock and transition our energy sources towards a net zero future.

The workforce shortfall has reduced, however shortages persist

Projected shortages for infrastructure workers have decreased (-32,000 compared to the 2023 forecast) as demand softens and supply grows, reflecting the impact of governments actively managing ambitious pipelines to align demand more closely with market capacity. Accounting for the impact of cost escalations, and coupled with the softening of demand, the volume of workers required on the Major Public Infrastructure Pipeline alone has reduced by 20% across 2023–24 to 2027–28 compared to the previous five-year outlook period, helping to close the gap between supply and demand.

However, shortages continue across each of the three occupational groupings (Engineers, Scientists and Architects; Trades and Labour; and Project Management Professionals).

This year, demand has shifted across certain occupation groups compared with the previous year’s forecasts, due to the natural progression of projects and adjustment of forward pipelines. For example, peak demand for engineers has now passed, as more projects move out of planning and design and into the construction phase. Notwithstanding, engineers remain in shortage.

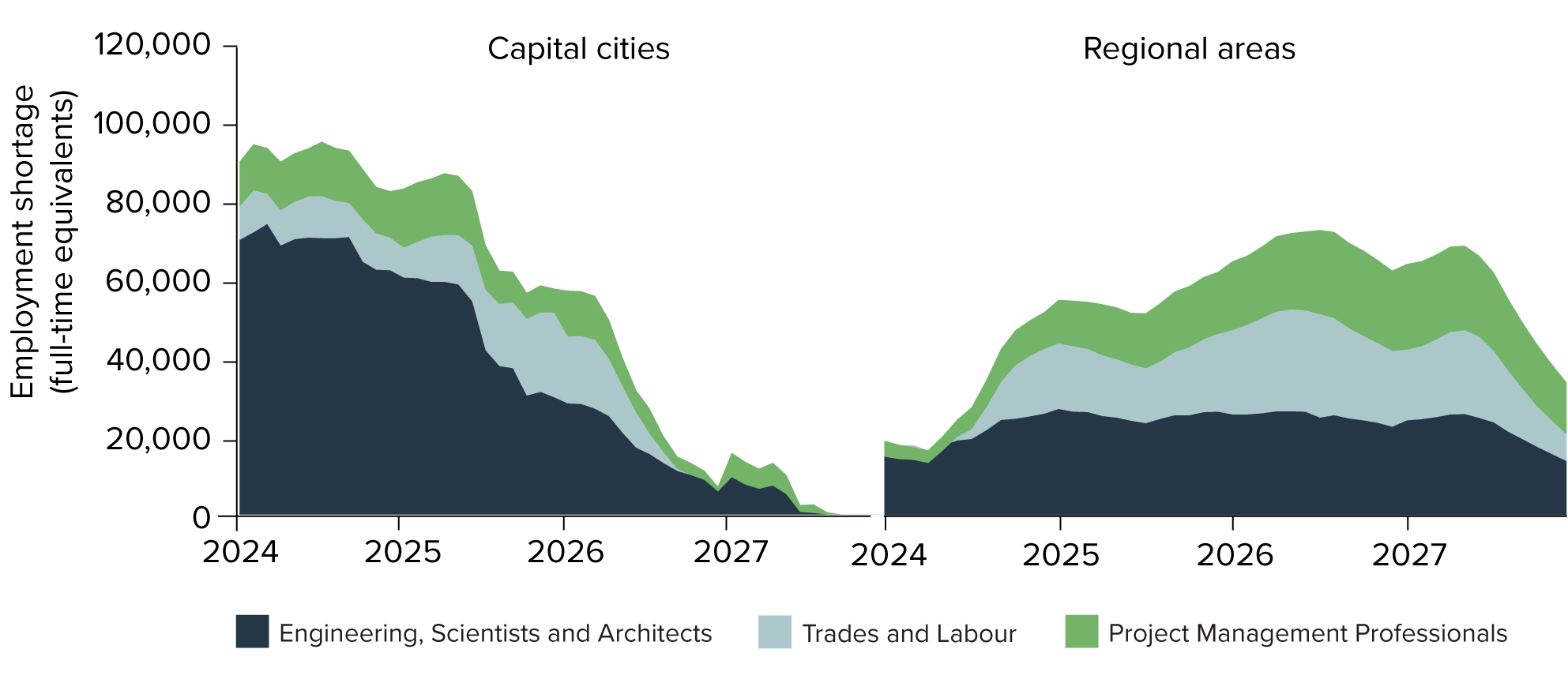

Nationally, shortages appear to have peaked in capital cities but are expected to rise in regional areas, due to significant new renewable energy projects announced in the regions alongside modest projected increases in supply.

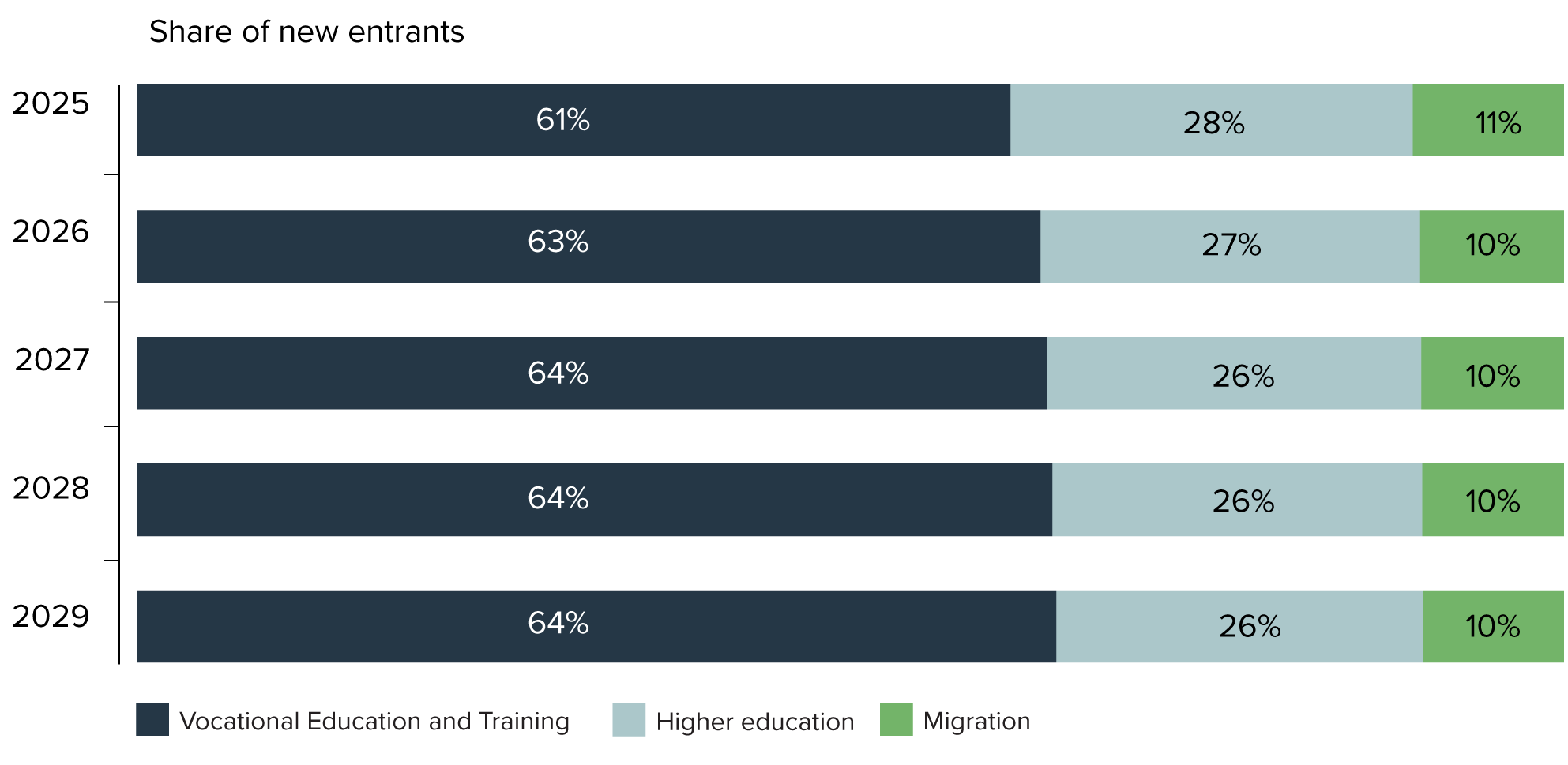

The majority (64%) of new entrant workers will come from Vocational Education and Training, with a quarter from higher education and the rest from migration (10%).

Changes to the size of the infrastructure workforce appear to be largely attributable to workers moving in and out of the construction industry, rather than shifting within construction sectors (examples include movements from infrastructure to housing, housing to infrastructure, or commercial/industrial construction to infrastructure).

Project cost escalations have largely been driven by rising materials cost pressures

We have seen extraordinary escalation in costs trends over the past three years since the establishment of the Market Capacity Intelligence System in 2021, especially in non-labour resources. Recent data has indicated that the volatility of the past three years has, however, reached a point of relative stability, with average price growth for construction materials easing from 11% in 2021–22 and 12% in 2022–23 to 4.3% in 2023–24 (see Section 2: Non-labour Supply for details). It, therefore, was the right time for Infrastructure Australia to revisit the cost assumptions that underpin the Market Capacity database. This involved an analysis of cost escalations in the past three years compared with trends over the previous decade.

Key findings from Infrastructure Australia’s analysis include:

- Cost increases: the costs of land transport infrastructure construction have increased by 51–53% since 2010–11, with as much growth in the past 3 years as there was in the preceding 10 years. Heavy civil-engineering construction costs, including road and rail, have seen significant increases, particularly in 2020–21.

- Labour sensitivity: labour accounts for roughly two-thirds of costs in land-transport infrastructure construction, making this sector more sensitive to labour cost changes than others, such as housing, where labour costs constitute less than 40% of the average house construction expenses.

- Materials cost pressures: the extraordinary rise in output costs over the past three years has been driven by pressures on material costs.

The cost of construction materials continues to remain high, with most materials experiencing year-on-year growth for three straight years. However, the rate of growth appears to have eased over the past twelve months, driven largely by drops in the price for some steel products. Industry sentiment suggests a reported price escalation of non-labour inputs over the last 12 months of about 10–20%, and that prices are yet to peak.

Concrete and steel, the construction materials most in demand, are vulnerable to cross-sector competition in the event of supply shortages. An analysis of Australia’s steel fabrication capacity shows that over two-thirds of domestic capacity is located across New South Wales, Queensland and Victoria. The Northern Territory has least access to local supply despite having the largest demand growth rate of the jurisdictions for steel fabrication products within the Major Public Infrastructure Pipeline.

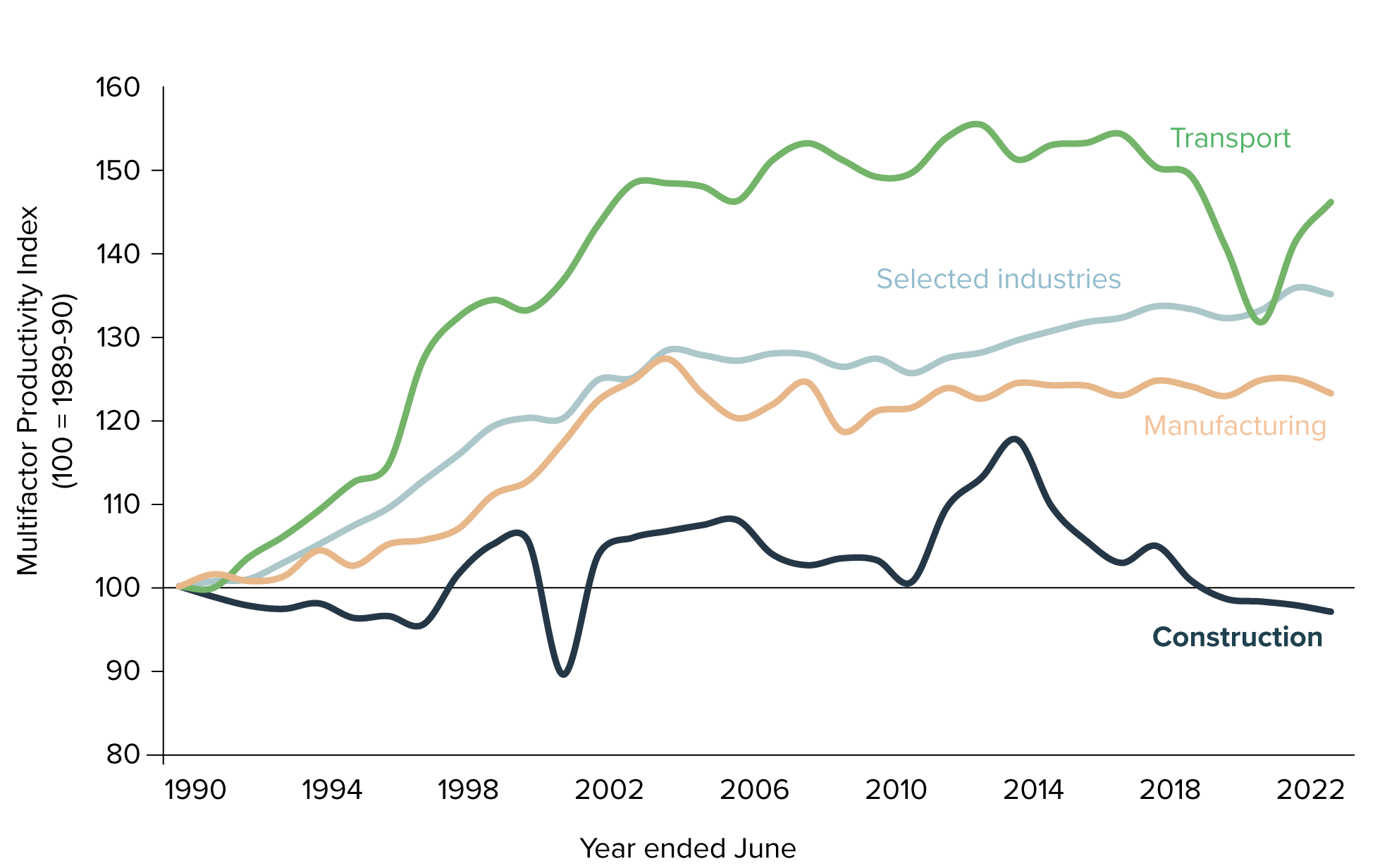

Construction industry productivity growth remains elusive, more detailed investigation on the supply chain is needed

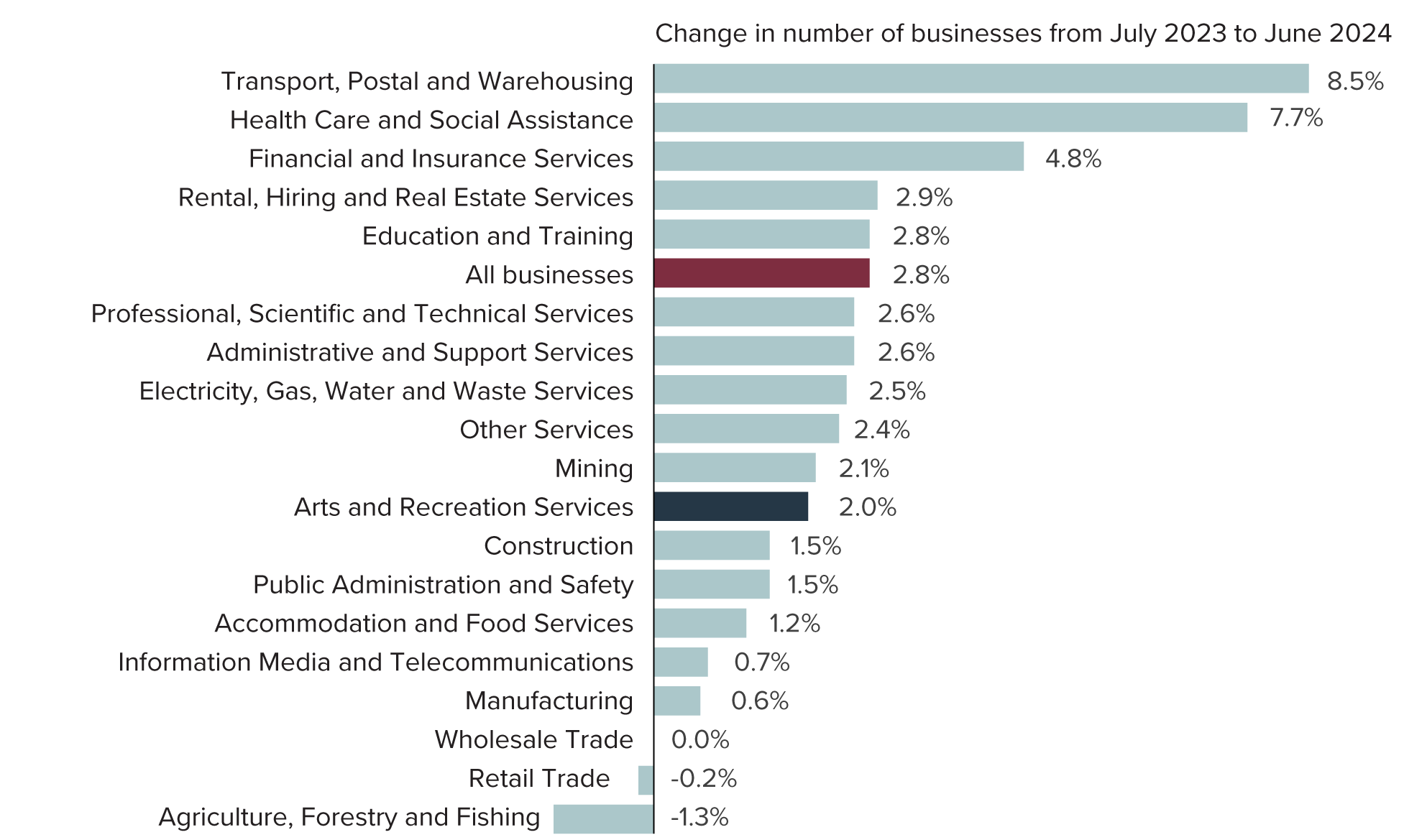

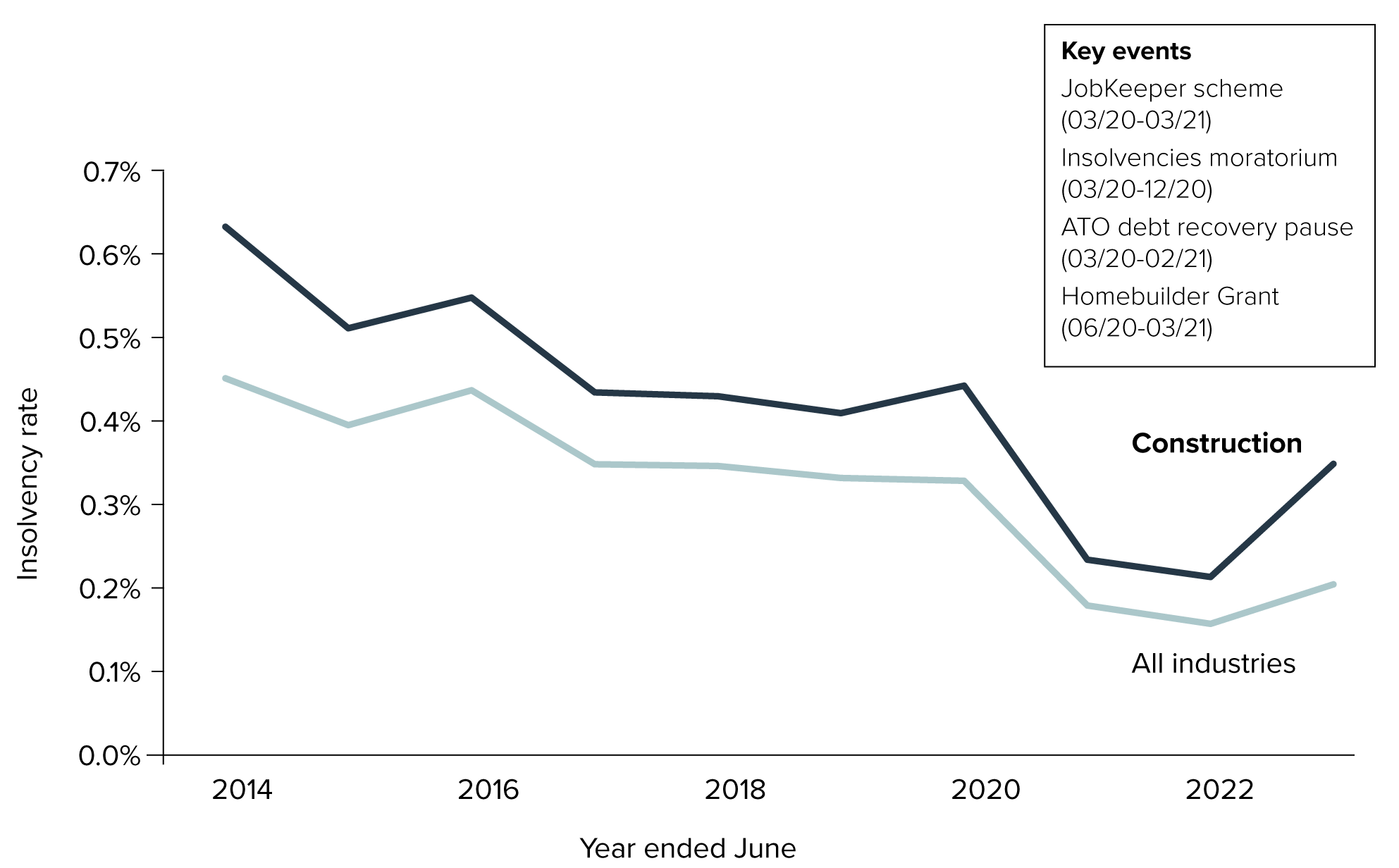

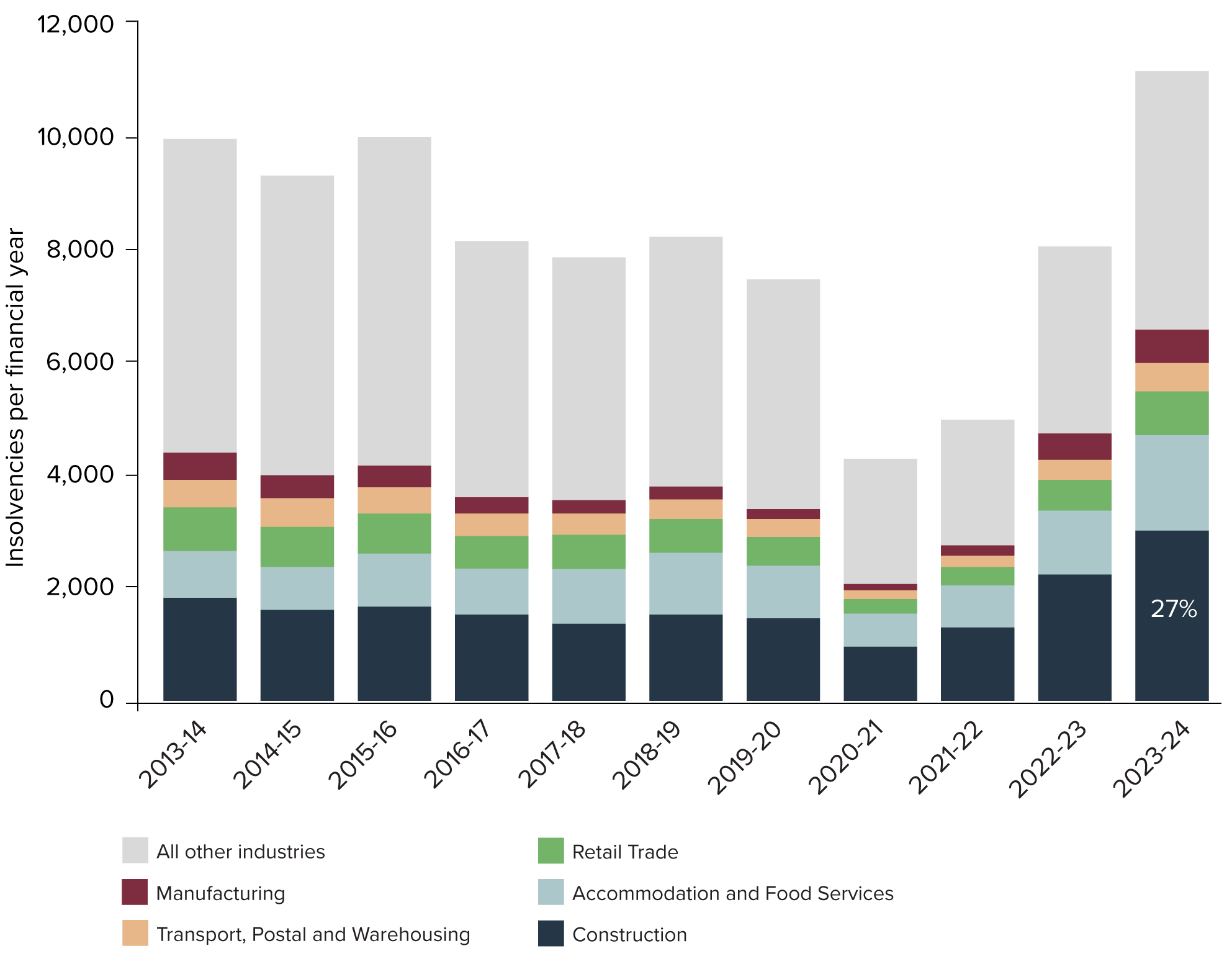

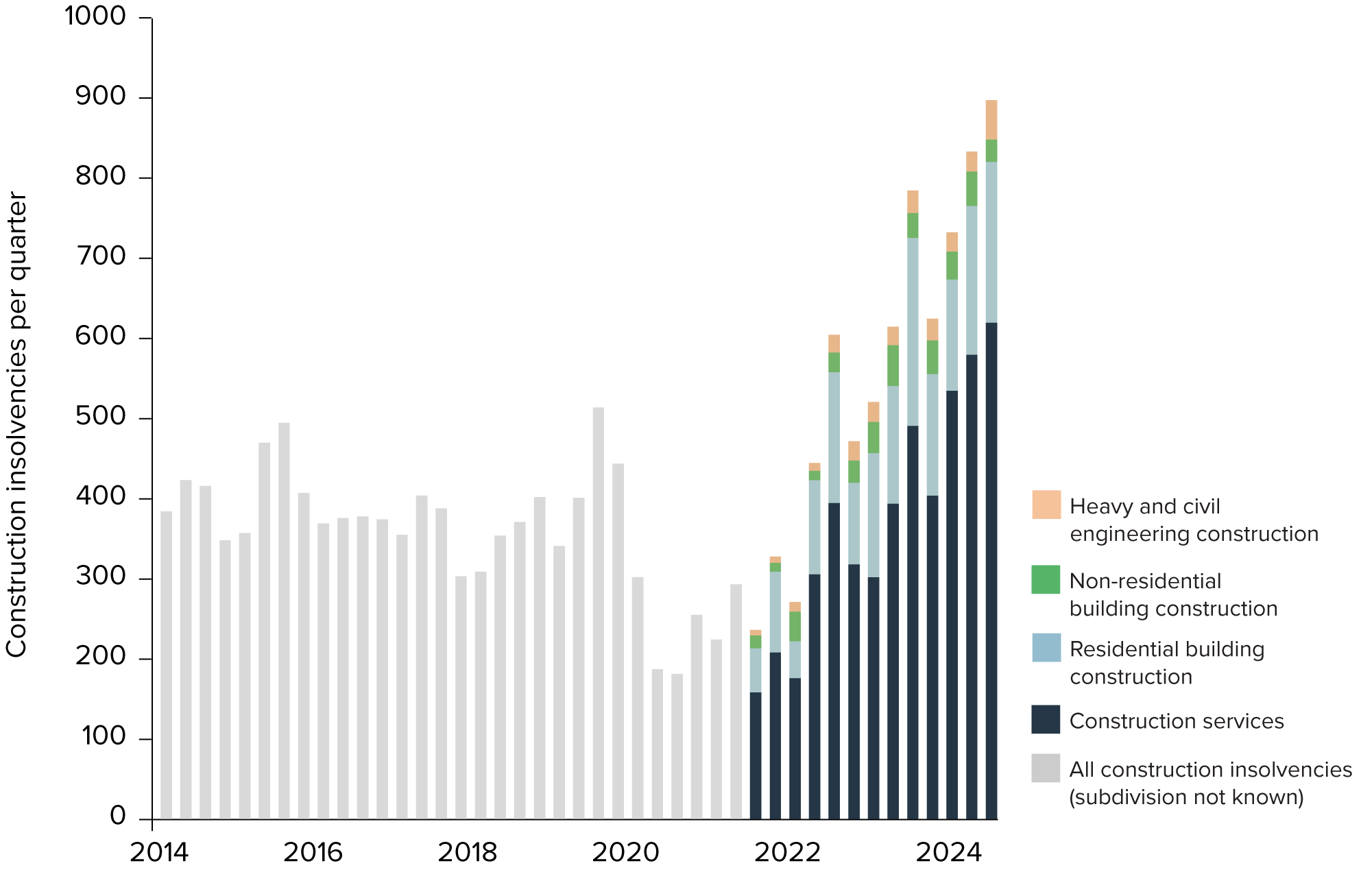

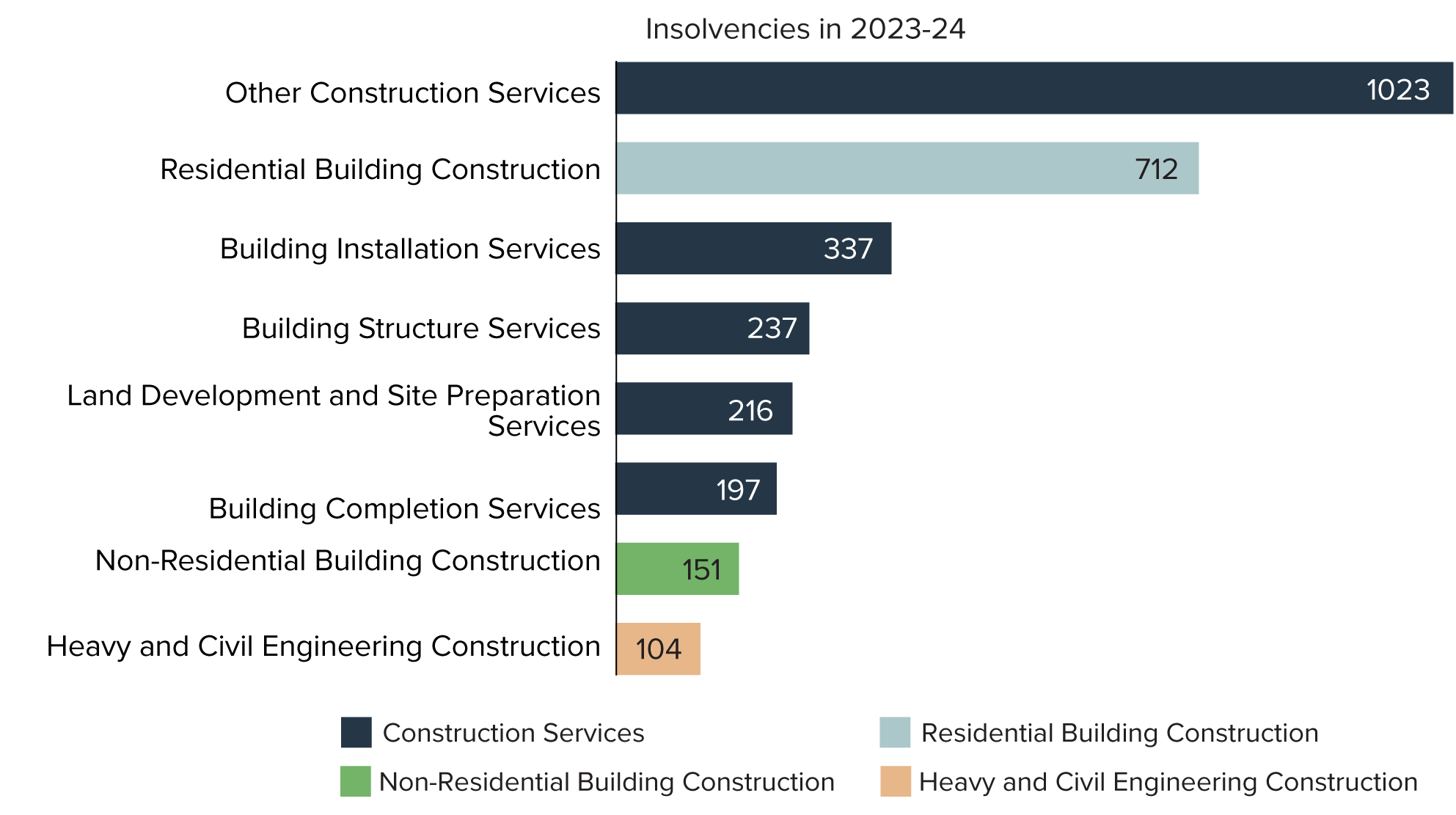

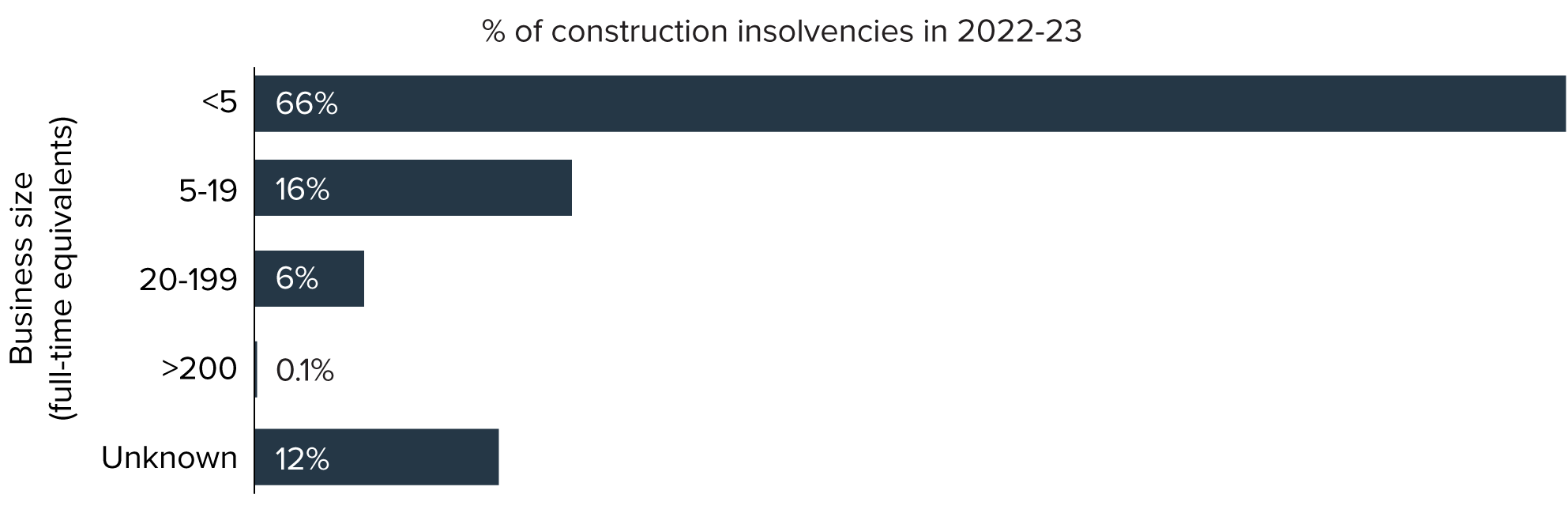

Construction industry insolvencies are disproportionately high compared to other sectors, accounting for almost 27% of total insolvencies in 2023–24. Small business insolvencies account for 82% of total insolvencies in construction and their profits are in decline. Within the sector, residential construction businesses account for a significant share of total construction insolvencies (24%), compared to non-residential construction businesses (5%) and heavy and civil engineering businesses (3%).

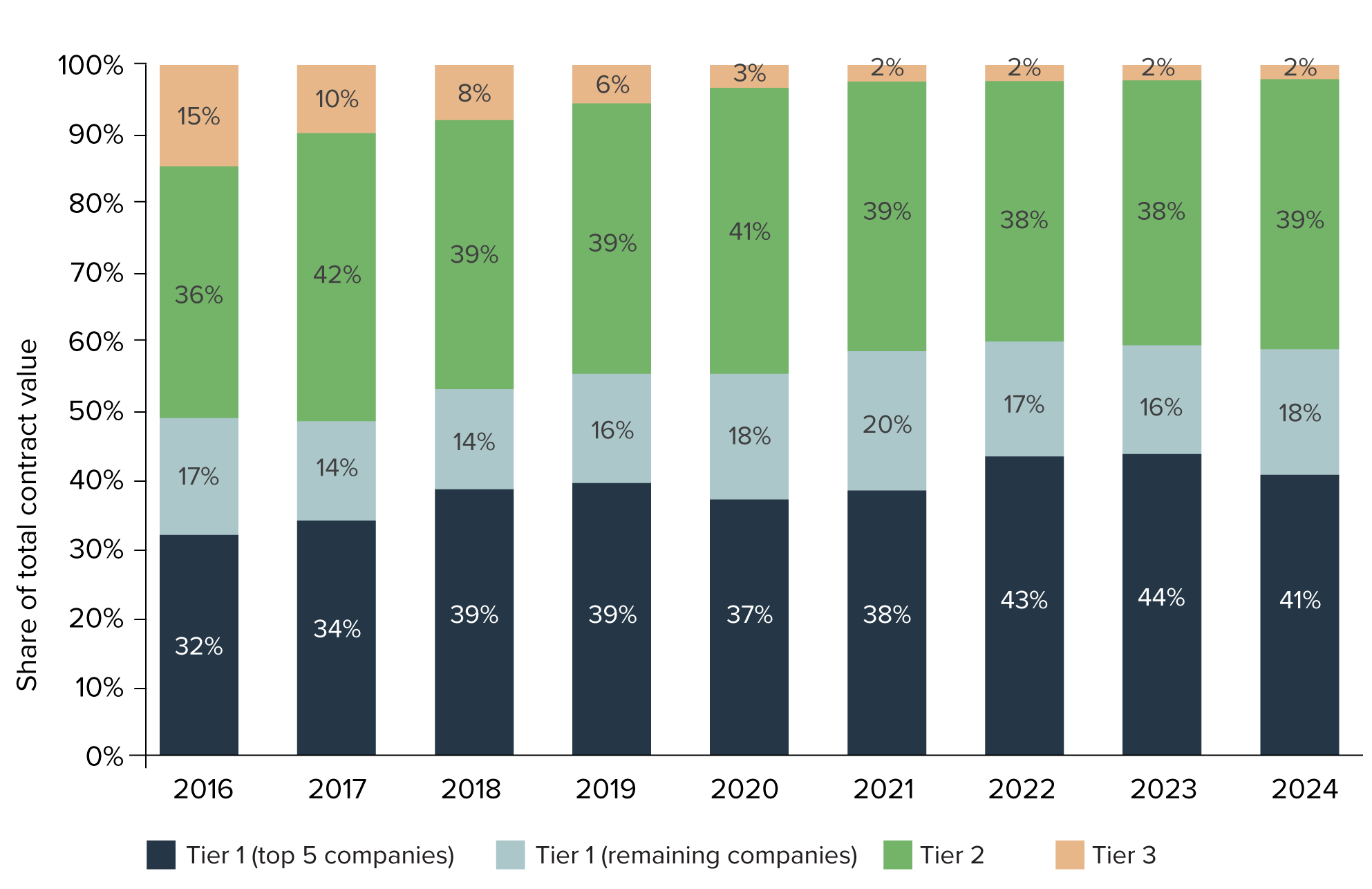

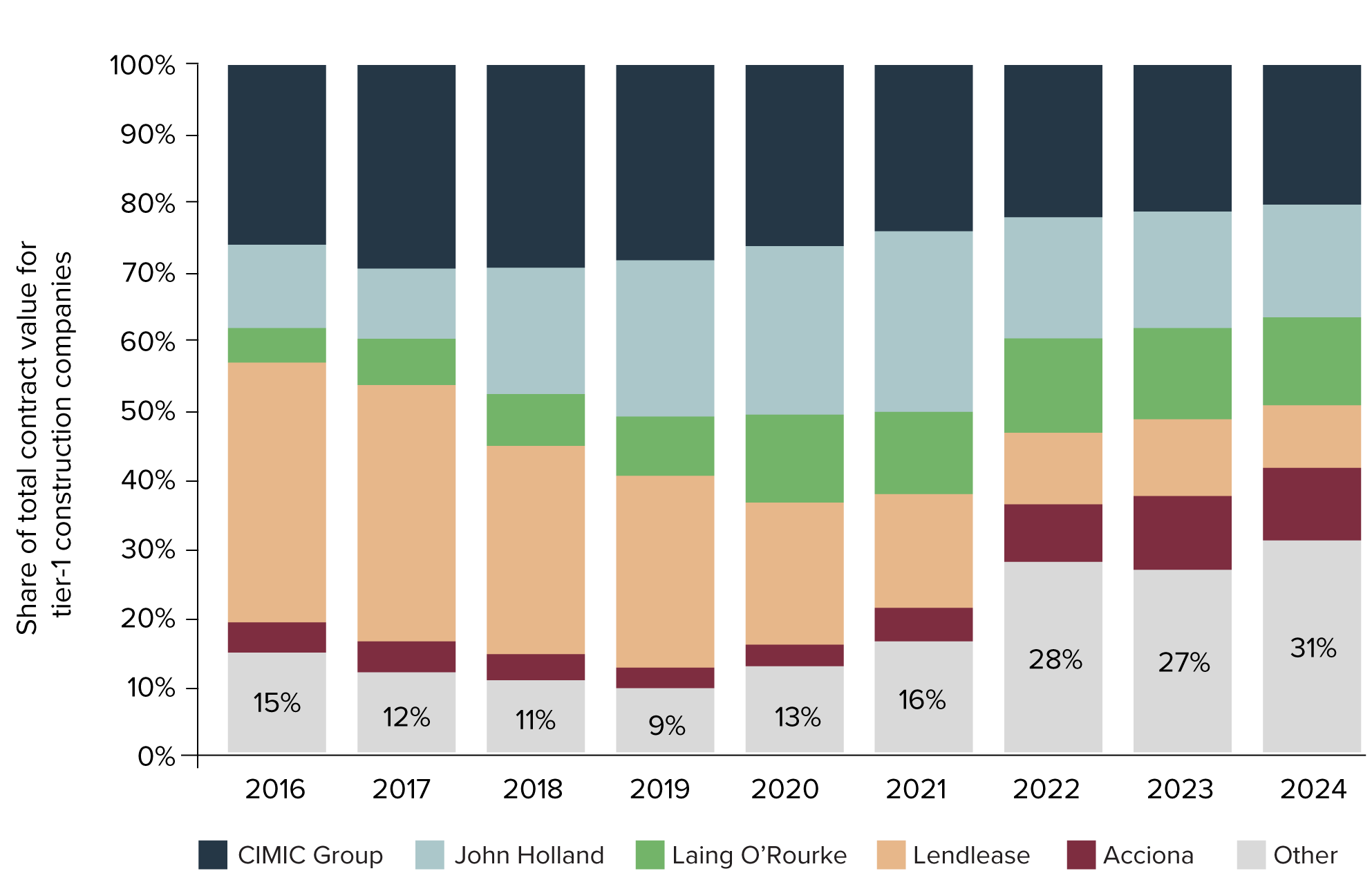

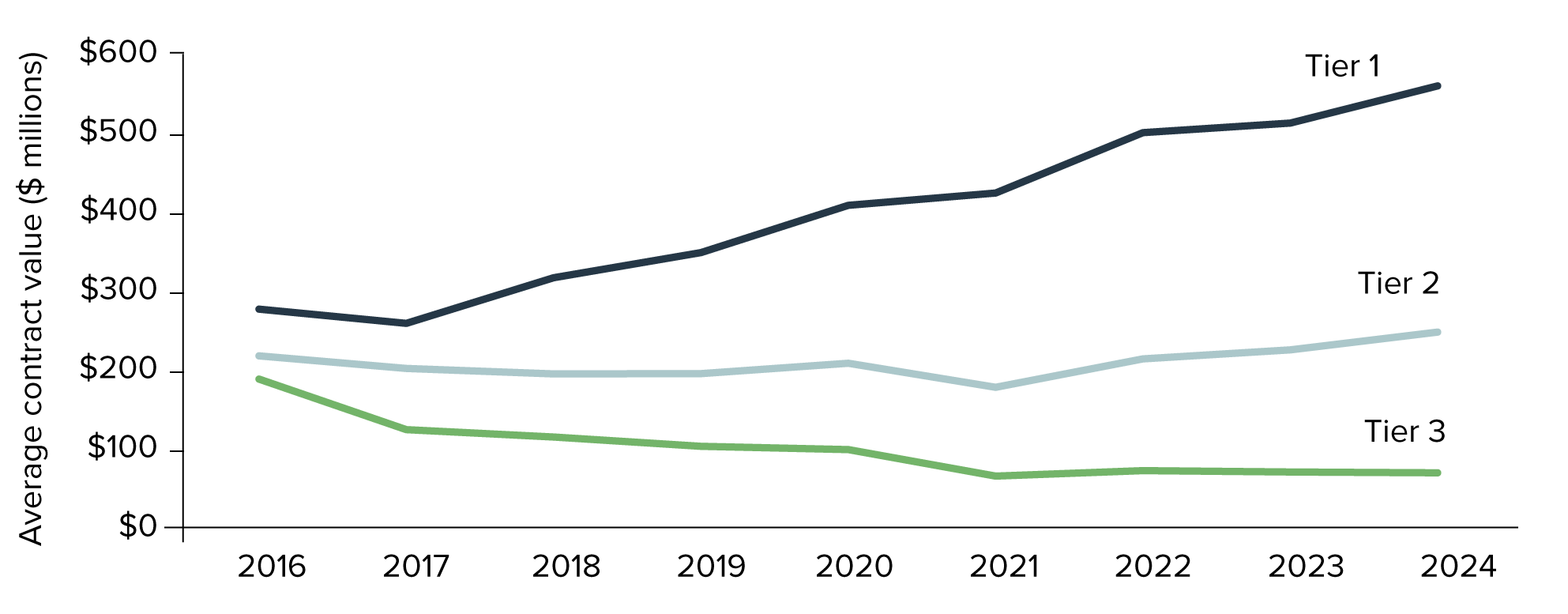

Tier-1 construction companies (that have delivered projects or been awarded contracts valued at over $1 billion) are taking a greater share of public infrastructure contracts, with the top 5 companies estimated to be holding over 40% of the infrastructure market’s current contract value in 2024.

While construction productivity growth remains stagnant, economic and financial indicators for the industry are up, with earnings up by 11.6% and contribution to national gross domestic product (Industry Value Added) up by 14.8% in 2022–23.

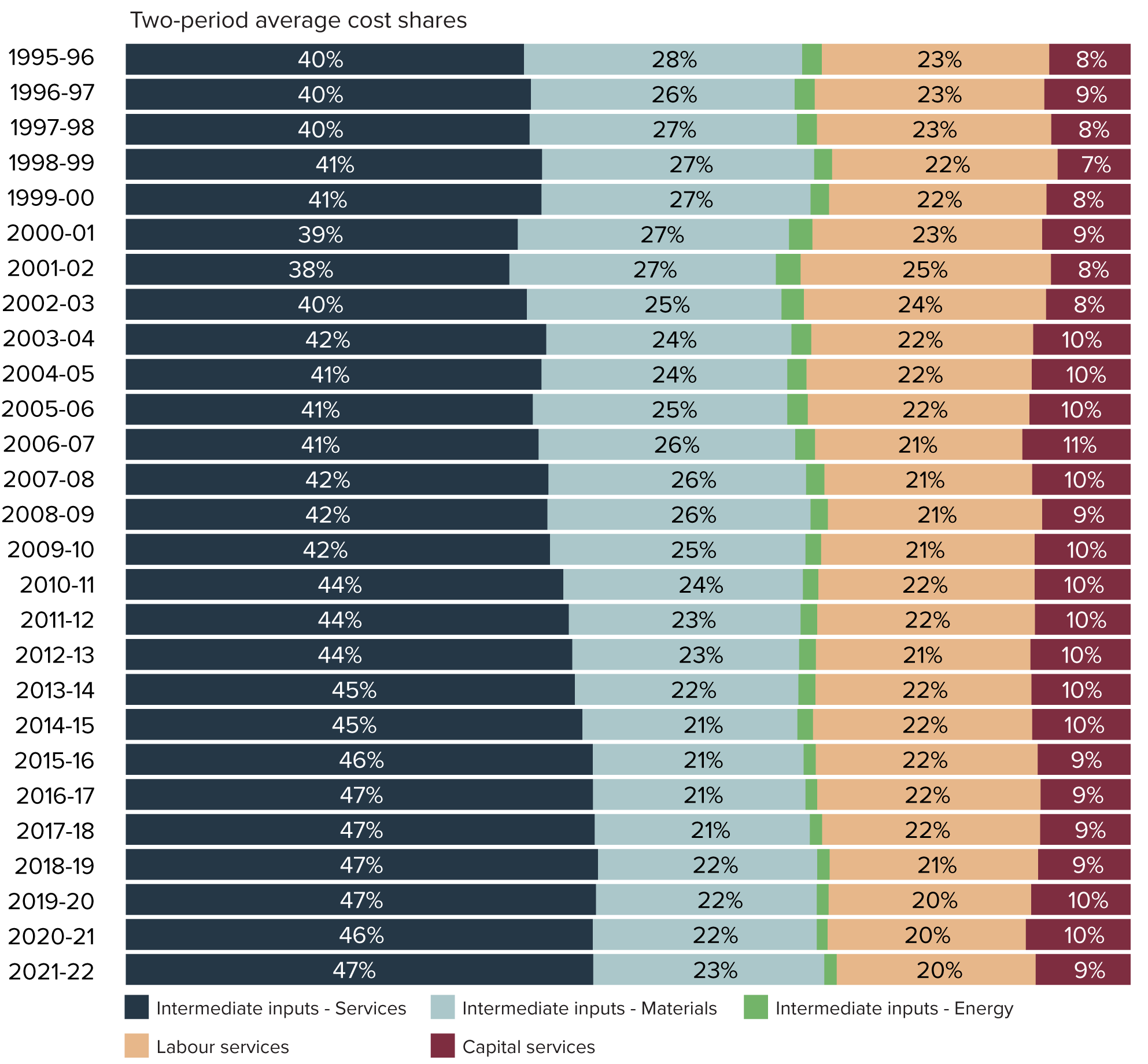

At an industry level, construction productivity is driven by sustainable construction output growth supported by growth in labour and capital productivity. Almost 47 cents in every dollar spent by a construction company goes to outsourcing services, such as labour hire for skilled trades workers, design and engineering consultants, and capital rentals such as hiring a crane (defined by the Australian Bureau of Statistics as ‘intermediate services inputs’). This has gradually grown from 40 cents in every dollar in 1995–96.

The high reliance on outsourced services reflects a structural characteristic of the construction industry, where work is delivered by larger businesses subcontracting further down the chain to smaller or specialist businesses. Further work to understand the impact of contracting arrangements between stakeholders (client, constructor, subcontractor, supplier) and outsourced services on construction supply-chain resilience would enable governments and industry to better identify project performance drivers that could drive sectoral productivity growth.

Despite stagnant levels of industry multifactor productivity growth, individual companies surveyed as part of Infrastructure Australia’s 2024 Industry Confidence Survey rate their current productivity levels as ‘good’. However, industry continues to call for a more balanced approach to risk allocation in contracts, citing issues such as overly complex and litigious contract models, governments’ low tolerance for risk and the threat of extreme weather events on project delivery. Parties need to continue working together to find the best balance of risk to minimise unnecessary costs and deliver best value for money.

Progress to mitigate market capacity constraints over the past 12 months

59% of the Major Public Infrastructure Pipeline is made up of land transport infrastructure projects, and since the previous Infrastructure Market Capacity Report, there have been significant enhancements to the Australian Government’s approach to priority setting, risk management, and the planning and delivery of land transport projects. This includes enhancements achieved through the new Federation Funding Agreement Schedule on Land Transport Infrastructure Projects (2024–2029), developed in partnership with the states and territories. The new Federation Funding Agreement Schedule replaces the preceding 5-year National Partnership on the Land Transport Infrastructure Projects (2019–2024).

Active demand management

Impactful reforms include:

- Articulation of the Australian Government’s key policy objectives, its role, and expectations for its investment via the Infrastructure Policy Statement (the ‘Statement’), which includes the preference to fund nationally significant land transport infrastructure projects on a 50:50 basis with state and territory delivery partners (with the possibility of a greater contribution in jurisdictions on a case-by-case basis).

- Changes to the investment profile for several projects as a result of the 2023 Independent Strategic Review of the Infrastructure Investment Program.

- Negotiation of the new Federation Funding Agreement Schedule, which defines the partnership between the Australian Government and state and territory governments through which land transport infrastructure will be delivered. It sets out investment objectives, outcomes and outputs; the roles and responsibilities of each of the parties; performance monitoring and reporting obligations; as well as financial and governance arrangements.

- Through the Federation Funding Agreement Schedule, the Australian Government and state and territory governments have committed to achieving their shared objectives, including:

- Introduction of a 2-pass process for investment, enabling more rigorous planning processes and alignment between governments.

- Introduction of a risk framework that is linked to the development of adequate due diligence for a project, using a confidence index throughout the project lifecycle that is central to the risk framework, and positive obligation reporting.

- Provision of Annual Infrastructure Plans by states and territories, which will inform the Australian Government’s investment funding decisions and ensure their alignment with a more strategic, long-term view (10 years).

- A commitment by governments to optimise their procurement practices to enable a range of agreed socio-economic outcomes that correspond with key recommendations provided in the 2023 Infrastructure Market Capacity Report, including:

- a reduction in embodied carbon in transport infrastructure in line with Australia’s Net Zero commitments

- an increase in women’s participation at all levels of the construction industry

- optimising recycled content in transport infrastructure to support Australia’s transition to a circular economy by 2030

- supporting opportunities for Australian and local businesses and industry

- optimising opportunities for trainees and apprentices, including Australian Skills Guarantee targets, to ensure a pipeline of skilled workers

- optimising opportunities to enhance construction sector culture and participation, including flexibility, wellbeing and diversity.

- Establishment of performance indicators and reporting arrangements to measure performance.

These reforms demonstrate governments’ intentions to actively manage their transport infrastructure pipelines and reduce the gap between the supply and demand for resources in infrastructure delivery. We are starting to see the impacts this year, with a more manageable public infrastructure pipeline coming off the exponential growth trajectory of the past few years. However, demand still significantly outweighs supply, and construction productivity growth remains stagnant compared to other industries (such as transport or telecommunications).

Adherence to the renegotiated Federation Funding Agreement Schedule processes will support active demand management of the transport infrastructure pipeline. Governments will need to remain vigilant and discerning in their infrastructure spend, including closely managing cross-sector demand in the face of budget and inflationary pressures over the short-to-medium term.

Long-term approaches to boosting supply

The Australian Government 2024–25 Budget aimed at helping built environment organisations acquire a larger share of the available workforce and boost workforce productivity. Under the Australian Universities Accord (released February 2024) and the National Skills Agreement (commenced January 2024), funding was committed in the 2024–25 Budget that would boost construction workforce supply. BuildSkills Australia, the Jobs and Skills Council for the building, construction, property and water sectors (launched in February 2024), has also released its 2024 Workforce Plan that aims to identify the most important strategic challenges facing the construction, property and water industries, and provides a framework for tackling these challenges in collaboration with industry, unions and government.1 Key challenges identified in the Workforce Plan include attracting and retaining highly skilled workers and improving productivity in the construction sectors.

The Australian Government 2024–25 Budget invests $22.7 billion over the next decade to secure Australia’s place in the net-zero global economy, through the Future Made in Australia plan. A key component of the Future Made in Australia plan is the National Interest Framework, designed to guide the Australian Government’s decision-making process for identifying and supporting priority industries.2 The Framework identifies green metals as a priority industry under the net-zero transformation stream, along with renewable hydrogen and low carbon liquid fuels. Two other priority industries, critical metals processing and clean energy manufacturing, are also included under a second economic resilience and security stream.

Steel is a key material used in construction and conventional means of steel production are carbon intensive. Australia can develop a long-term comparative advantage in green metals by drawing on our abundant metal and renewable energy resources. The Future Made in Australia plan may relieve pressure on supply chains and boost local workforce capability.

Create measures and take actions to enable an uplift in construction industry productivity

Another key area of progress is the development of a National Construction Strategy to improve construction productivity. Through the Infrastructure and Transport Senior Officials’ Committee (ITSOC), governments are working with industry on national approaches across four areas:

- Data collection and benchmarking: to establish measures to assess and track productivity performance.

- Workforce: to increase retention and attraction of diverse workers (including women’s participation).

- Procurement and contracting: for the use of procurement methods to deliver project outcomes.

- New technology and modern methods of construction: to explore ways to increase uptake of digital methods and modern methods of construction.

Looking ahead

In keeping with the recommendations made in the 2023 Infrastructure Market Capacity Report, this year’s edition refreshes existing demand and supply insights, while adding new evidence, all of which is oriented towards demonstrating progress against the recommendations.

For each recommendation area — managing demand, boosting labour supply, boosting non-labour supply and increasing productivity — we propose the future directions for the Australian Government to continue the momentum gained this year. Collectively, these recommendations present national priorities for monitoring and mitigating infrastructure market capacity constraints, across all infrastructure sectors. Table 1 sets this out in detail.

Table 1: Update on progress made against 2023 recommendations and future directions

Active demand management | |||

|---|---|---|---|

| 2023 recommendation | Progress over last 12 months | Current state | |

| 1 | Active pipeline management |

|

|

| 2 | Consider cross-sector whole-of-market capacity | ||

| Future directions | |||

| |||

Boost materials supply | |||

|---|---|---|---|

| 2023 recommendation | Progress over last 12 months | Current state | |

| 3 | Quarry supply |

|

|

| 4 | Steel supply | ||

| 5 | Local materials production data | ||

| 6 | Recycled materials | ||

| Future directions | |||

| |||

Boost workforce supply | |||

|---|---|---|---|

| 2023 recommendations | Progress over last 12 months | Current state | |

| 7 | Develop a National Infrastructure Workforce Strategy |

|

|

| 8 | Boost the higher education pipeline | ||

| 9 | Place more qualified onshore migrant engineers in engineering jobs | Future directions | |

| 10 | Boost the supply of apprentices and trainees |

| |

| Improve construction productivity | |||

|---|---|---|---|

| 2023 recommendations | Progress over last 12 months | Current state | |

| 11 | A productivity study and national baseline |

|

|

| 12 | Participation and workplace culture | ||

| 13 | New technologies and modern methods of manufacturing | ||

| 14 | Risk allocation between parties | ||

| Future directions | |||

| |||

Introduction

The annual Infrastructure Market Capacity reports respond to a request made by the Prime Minister and First Ministers in 2020: that Infrastructure Australia work with jurisdictions and industry bodies to monitor the infrastructure sector.

“Leaders considered analysis on the market’s capacity to deliver Australia’s record pipeline of infrastructure investment to support the country’s growing population. This analysis highlighted the importance of monitoring infrastructure market conditions and capacity at regular intervals to inform government policies and project pipeline development. Leaders agreed that Infrastructure Australia will work with jurisdictions and relevant industry peak bodies to monitor this sector.”

Source: Council of Australian Government Communiqué, 20 March 2020

The fourth publication on infrastructure demand and supply from Infrastructure Australia

Like the previous three editions of the Infrastructure Market Capacity Report, this report examines public infrastructure demand and market supply capacity over five years - in this case, 2023—24 to 2027—28. It provides an updated health check and analysis of our national construction market’s capacity to deliver public infrastructure works.

The report is structured as follows:

- Understanding demand: a quantification of total infrastructure demand across five years by sector, by project type, and detailed analysis of the Major Public Infrastructure Pipeline including year-on-year changes and escalation costs.

- Non-labour supply: an appraisal of the main supply-side risks to market capacity today, including industry views gleaned from interviews and surveys conducted for this report. The focus is on materials supply, which is the largest non-labour supply category by cost shares.

- Labour and skills supply: projections of infrastructure construction labour supply and shortage by jurisdiction and occupation groups. Plus, summary of emerging skills and an assessment of boarder construction workforce trends.

- Industry productivity: analysis of the current state of the construction industry, including productivity and insolvency trends, supplemented with industry perception obtained from our 2024 Industry Confidence Survey.

New for 2024: Expansion of demand-side coverage, updated demand-side resource cost assumptions, and steel fabrication capacity analysis

This edition of the Infrastructure Market Capacity Report advances the analysis on current and emerging influences on market capacity from previous reports, including:

Demand-side coverage: we have expanded our demand-side database by capturing investment in defence infrastructure works, private investment in mining and resources, and smaller scale residential buildings which have not previously been captured in earlier editions.

Demand-side resource costs: recent data has indicated that the cost-escalation volatility of the past three years has reached a point of relative stability, while analysis of the project cost estimates in our database verifies that cost pressures have been incorporated in estimates. To maintain accuracy of our modelled resource requirements, Infrastructure Australia updated its cost assumptions for resources demanded by applying appropriate increases (based on the Australian Bureau of Statistics Producer Price Index and Wage Price Index) to cost rates per resource.

Steel fabrication capacity analysis: The Australian Steel Institute initiated a collaboration with Infrastructure Australia to compare steel fabrication supply-side capacity by geography with nearby project-level demand. Similar supply-and-demand analysis on other materials could be included in future editions of this report if useful supply-side data is willingly shared following the positive example set by the Australian Steel Institute.

Continued emphasis on policy implications with acknowledgement of progress and looking ahead at future directions

Significant work has been undertaken against all four categories of recommendations from the 2023 Infrastructure Market Capacity Report to actively manage demand, boost materials supply, boost labour supply, and turn around construction productivity. This edition provides an update of market capacity conditions with respect to demand and points to future directions for the Australian Government to maintain the momentum for work in progress against each of the existing recommendation areas.

A brief explanation of our Market Capacity Program

The Market Capacity Program is an assumptions-based methodology for identifying market capacity risks. It was developed in collaboration with state and territory governments, industry, advisory bodies and other subject matter experts. These partnerships are integral to the ongoing evolution of the Market Capacity Program.

The Market Capacity Program is underpinned by two system components:

The National Infrastructure Project Database

The National Infrastructure Project Database aggregates and organises infrastructure project data supplied by the Australian Government (including defence), state and territory governments (public investments), the Australian Bureau of Statistics (housing building activity) and GlobalData (private investments).

The following infrastructure sectors are included in the Market Capacity Program:

- Buildings: non-residential buildings for health, education, sport, justice, transport buildings (such as parking facility and warehouse), other buildings (such as art facilities, civic/convention centres and offices), detached, semi-detached and multi-detached residential, apartments and renovation activities (using all residential building activities captured in the Australian Bureau of Statistics Building Approvals).

- Transport: roads, railways, level crossings, and other transport projects such as airport runways.

- Utilities: water and sewerage, energy and fuels, gas and water pipelines, and telecommunications.

- Resources: base metals, precious metals, critical minerals, hydrogen and ammonia, chemical & pharmaceutical plants, oil and gas, and ports.

Market Capacity Intelligence System

The Market Capacity Intelligence System is a set of analytical tools that interrogates and visualises project demand sector, project type and resource inputs, for the following infrastructure pipelines:

- Major Public Infrastructure Pipeline: Publicly funded infrastructure projects valued over $100 million in New South Wales, Victoria, Queensland and Western Australia, and over $50 million in South Australia, the Australian Capital Territory, the Northern Territory and Tasmania.

- Small Capital Public Infrastructure Pipeline: Publicly funded infrastructure projects valued $100 million and under in New South Wales, Victoria, Queensland and Western Australia, and $50 million and under in South Australia, the Australian Capital Territory, the Northern Territory and Tasmania.

- Private Infrastructure Pipeline: Privately funded public infrastructure, such as a wind farms, that is funded, delivered and operated by the private sector.

- Private Buildings: Residential and non-residential buildings projects.

- Road Maintenance: Resource demands for road-maintenance projects.

Enhancements to the Market Capacity Program in 2024: accounting for cost escalations

We have comprehensively reviewed and updated our Market Capacity Program assumptions this year to ensure our cost estimates and assumptions reflect current economic conditions.

Step 1 involved a comparative analysis of 2024 data collection from jurisdictions to compare the average investment by infrastructure asset class across all jurisdictions, compared with 2022 project estimates before inflation accelerated. We found that those estimates had increased in line with cost pressures. Because this revision to estimates occurred across the pipelines of states and territories, it meant Infrastructure Australia’s modelling assumptions needed to be updated to reflect inflation, such that we are forecasting the right number of workers needed or material tonnages needed.

Step 2 involved work to integrate relevant price indices, including the Australian Bureau of Statistics’s Producer Price Index and Wage Price Index, to ensure differential escalation rates of construction inputs are factored into our cost estimates and assumptions.

Step 3 involved the application of resource-specific escalation rates. Different resource categories were found to have unique escalation rates. For example, the cost of materials like steel or concrete have increased at a different rate compared to labour costs or equipment rental fees. This variation is due to factors such as supply-chain dynamics, market demand, and industry-specific constraints. By incorporating differential escalation rates, the updated assumptions provide a more accurate and realistic representation of the current cost environment, ensuring that the project estimates are aligned with the latest economic conditions.

Industry confidence research

Supporting the quantitative analysis research each year, Infrastructure Australia also undertakes industry research to gauge industry confidence levels and better understand their perspectives on current market conditions.

This year, three surveys were undertaken of Australian businesses in the building and construction industry, supplemented with in-depth interviews:

- The 2024 Industry Confidence Survey (n=200) captured views across the infrastructure life cycle, across identification/planning, design, construction, operations and management. The survey sample were actively delivering contracts that ranged in value from less than $10 million to more than $1 billion over the last 12 months.

- The 2024 Civil Contractors Federation Survey of its members (n=122) captured views of civil-construction businesses, comprised of majority (63%) smaller Tier-3 and Tier-4 businesses with annual turnover of less than $100 million.

- The 2024 Infrastructure Australia Labour Shortage Survey (n=40), as one of various inputs into the workforce analysis, supplements quantitative data and provides additional nuanced insights into projected shortages. Surveyed businesses had operations covering all jurisdictions and all construction sectors (transport, residential, commercial and social infrastructure).

- In-depth interviews (n=20) with randomly selected building and construction businesses, with each tier represented, to get a more detailed understanding of the key issues for the year.

All state and territories were represented in this year’s industry surveys and were roughly representative of construction industry geographical spread across the country – most in New South Wales and Victoria, followed by Queensland, Western Australia and South Australia, and the smaller jurisdictions Australian Capital Territory, Tasmania and the Northern Territory.

For more details on the survey methodology, see Appendix F: Industry Confidence surveys.

Detailed methodologies in Appendices

See the Supporting Appendices for detailed explanations of the Market Capacity methodology:

- Appendix A: Demand-side analysis methodology

- Appendix B: Supply-side analysis methodology

- Appendix C: Infrastructure typecasts

- Appendix D: Resource classifications

- Appendix E: Workforce and skills methodology

- Appendix F: Industry confidence surveys

- Appendix G: Revision of cost escalation assumptions.

Section 1: Understanding demand Summary

This section presents Infrastructure Australia’s 2024 demand projections for major public infrastructure works over the five-year outlook (2023–24 to 2027–28), within the context of the wider construction market. It includes analysis of changes over the last 12 months compared to projections last year, covering views of the demand profile by construction sectors, geographies, workforce and materials.

The demand analysis is supplemented with industry assessments of current delivery capacity, including changes over the last 12 months and confidence to scale up over the forward estimates, collected from our 2024 industry surveys and interviews.

Key points

- A reduction of 8% in major public infrastructure demand, compared with the projection of 12 months earlier, represents a significant management of demand by governments across Australia.

- Transport infrastructure investment remains the largest expenditure category, accounting for 59% of the Major Public Infrastructure Pipeline, but has dropped by $32 billion from the previous year’s projections.

- Building and Utilities infrastructure investment continues to grow this year, accounting for 34% and 7% of the Major Public Infrastructure Pipeline respectively. Growth of these sectors reflects governments’ ambitions to boost housing stock and advance the energy transition towards net zero.

- The Major Public Infrastructure Pipeline sees a geographical shift in investment to the north, with Queensland and the Northern Territory growing by $16 billion, while New South Wales and Victoria have reduced by $39 billion versus the previous outlook period.

- The demand for workers on major public infrastructure has reduced by 20% (average monthly FTE) versus the previous outlook period, reducing the gap between supply and demand compared to what Infrastructure Australia had previously reported (further detailed analysis on workforce supply is provided in Section 3: Workforce and Skills).

- The industry reports moderate confidence in its ability to scale up, with over half expressing confidence in scaling up operations by 25% in the future. The residential sector is the least confident about scaling up, while the transport sector shows the highest confidence to scale up in response to changes in public investment in future project pipelines.

Section 1: Understanding demand

Active demand management – future directions

The Australian Government, in partnership with state and territory governments, should continue to actively manage public infrastructure demand through:

- adoption and adherence to the new Federation Funding Agreement Schedule on Land Transport Infrastructure Projects (2024-2029) processes to support active pipeline management.

- building on the analysis from this 2024 Infrastructure Market Capacity Report, quantifying the construction workforce engaged in sectors outside infrastructure (such as housing and energy) to identify adjacencies and potential worker mobility between sectors to fill labour gaps.

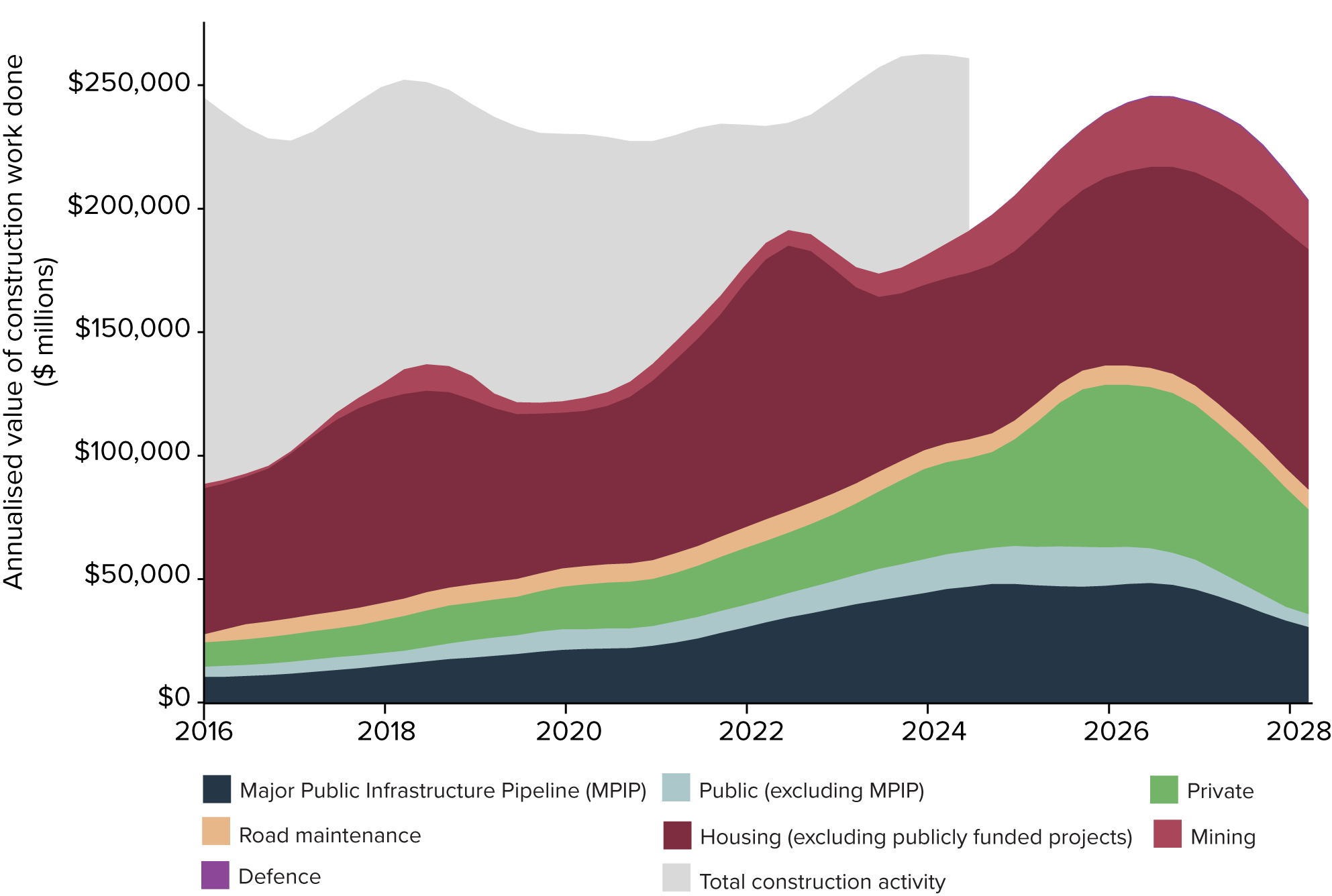

The market capacity analysis now captures more construction activity than ever before

Figure 1 shows the Infrastructure Australia pipeline of forecast construction activity based on cost estimates against the backdrop of total construction activity as reported by the Australian Bureau of Statistics. The main difference between the two measures is that the Australian Bureau of Statistics incorporates the impact of cost escalations, while the Infrastructure Australia database shows cost estimates with far less certainty about the value of future escalations. This key difference makes it difficult to assert how much of total construction activity is captured in our database. However, by expanding our database this year to include more residential activity, mining projects and defence capital projects, our database now forecasts a volume of construction activity that peaks in 2026 almost in line with current levels of construction work done as reported by the Australian Bureau of Statistics.

Even though we do not expect all projects to proceed as announced, this approach provides valuable insight into market ambition in the coming years. It also provides the added benefit of enabling a more comprehensive analysis of market demand than was possible in previous editions.

Figure 1: Forecast construction spend, as captured in the Infrastructure Australia database, in the context of historic total construction activity (2016 to 2028)

Note: Infrastructure Australia no longer displays a projection for future total construction activity as exists in previous editions of the Infrastructure Market Capacity Report.

Source (for total construction activity): Australian Bureau of Statistics (2024)4

Total construction demand captured in our database covers $1.08 trillion in the five years from 2023–24 to 2027–28. This level of forecast activity is almost in line with current run rates where the total construction activity reported by Australian Bureau of Statistics in the five years from to 2019–20 to 2023–24 was $1.2 trillion.

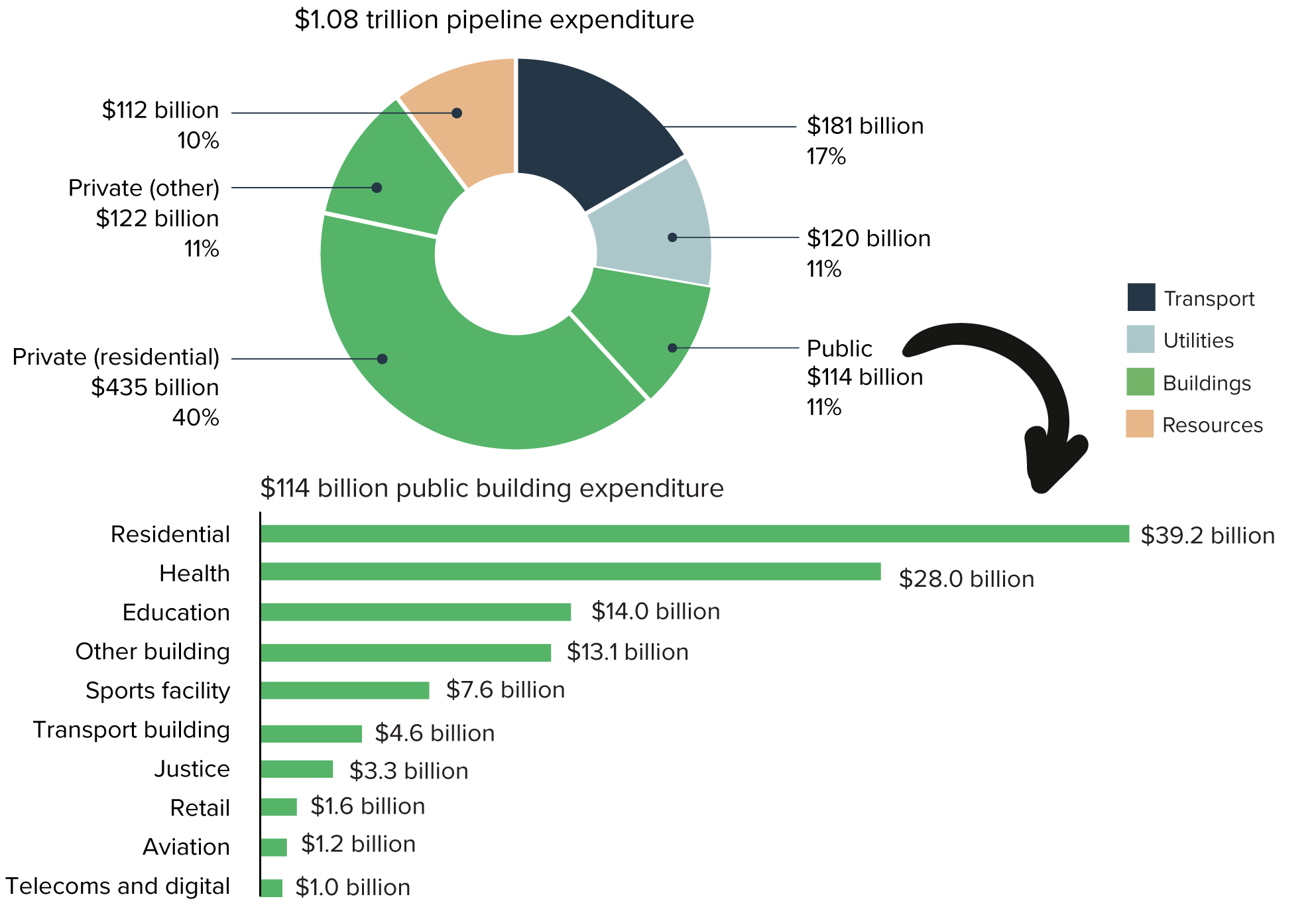

Figure 2 shows the total infrastructure pipeline, as captured in our database, broken down by sector. Buildings account for most of the expected expenditure (62%), followed by transport (17%), utilities (11%) and resources (10%).

Of the $671 billion in buildings, $71 billion is from the Major Public Infrastructure Pipeline, with another $43 billion invested in buildings by governments, totalling $114 billion of public investment. Figure 2 includes a breakdown of this public investment in buildings, which is dominated by residential and health projects.

For the period 2023–24 to 2027–28, public spending accounts for 25% of the $1.08 trillion construction market, of which the Major Public Infrastructure Pipeline totals $213 billion and $58 billion is planned on Small Capital Projects. The rest of this section provides an analysis of the Major Public Infrastructure Pipeline.

Figure 2: Combined construction pipeline, as captured in the Infrastructure Australia database, by sector (2023–24 to 2027–28)

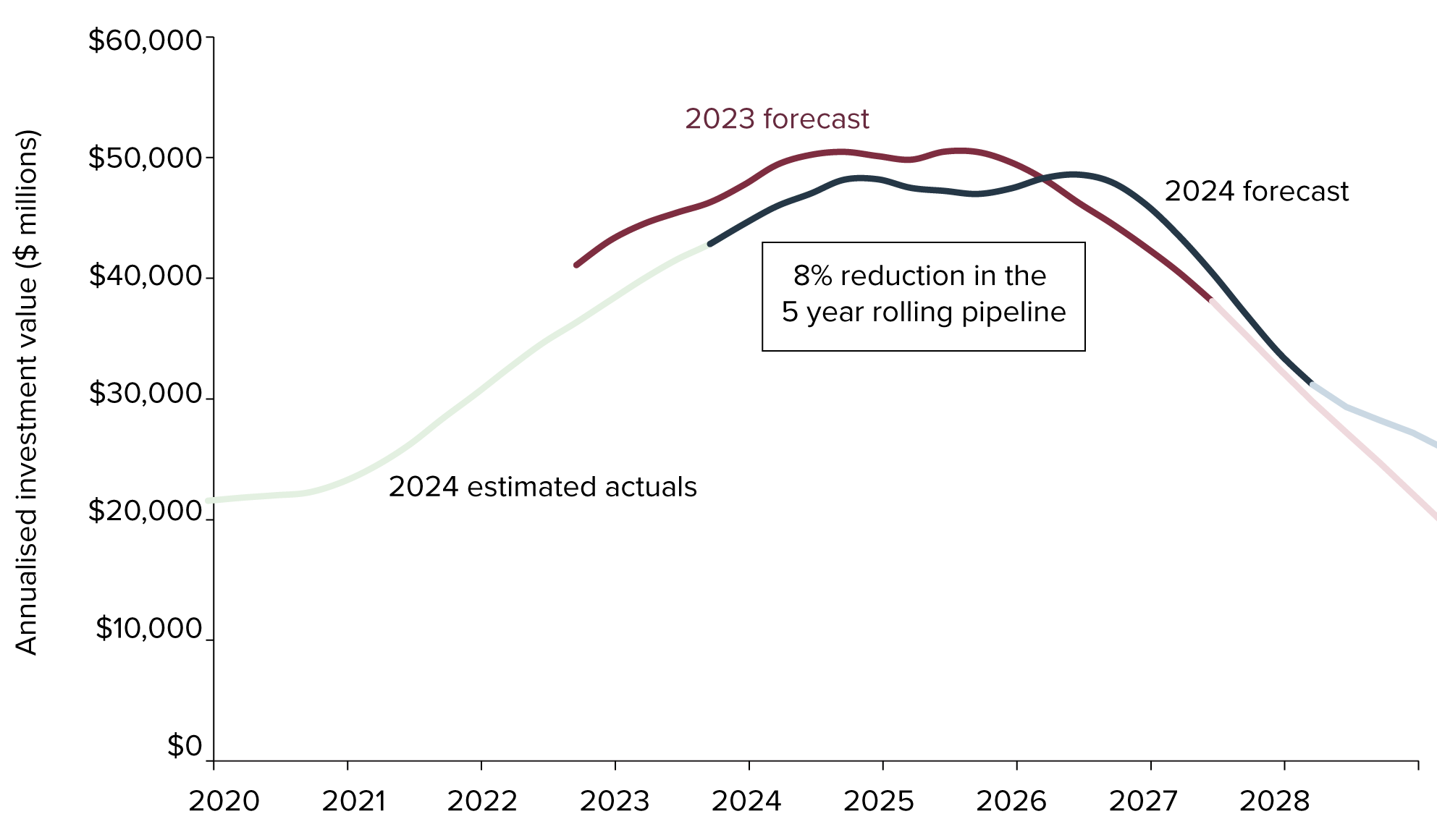

The 5-year Major Public Infrastructure Pipeline has dropped by 8% to $213 billion, with a flatter peak demand moving out one year to mid-2026

As shown in Figure 3, the 5-year rolling Major Public Infrastructure Pipeline has dropped from $230 billion projected last year (2022–23 to 2026–27) to $213 billion this year (2023–24 to 2027–28).

Peak investment has moved one year out to 2026 compared to the projection last year. These changes are consistent with a continuing trend each year observed by Infrastructure Australia of projected investment peak shifting into outer years, suggesting that the market struggled to deliver on an overly ambitious pipeline.

The peak demand is also flatter compared to previous years projections (2022, 2023) when demand rose exponentially to a high peak before dropping over outer years. The shape of the demand curve this year suggests a more realistic and achievable pipeline for a constrained market to deliver.

Figure 3: Comparison of 2023 and 2024 rolling forecasts of Major Public Infrastructure Pipeline activity (2022–23 to 2026–27 versus 2023–24 to 2027–28)

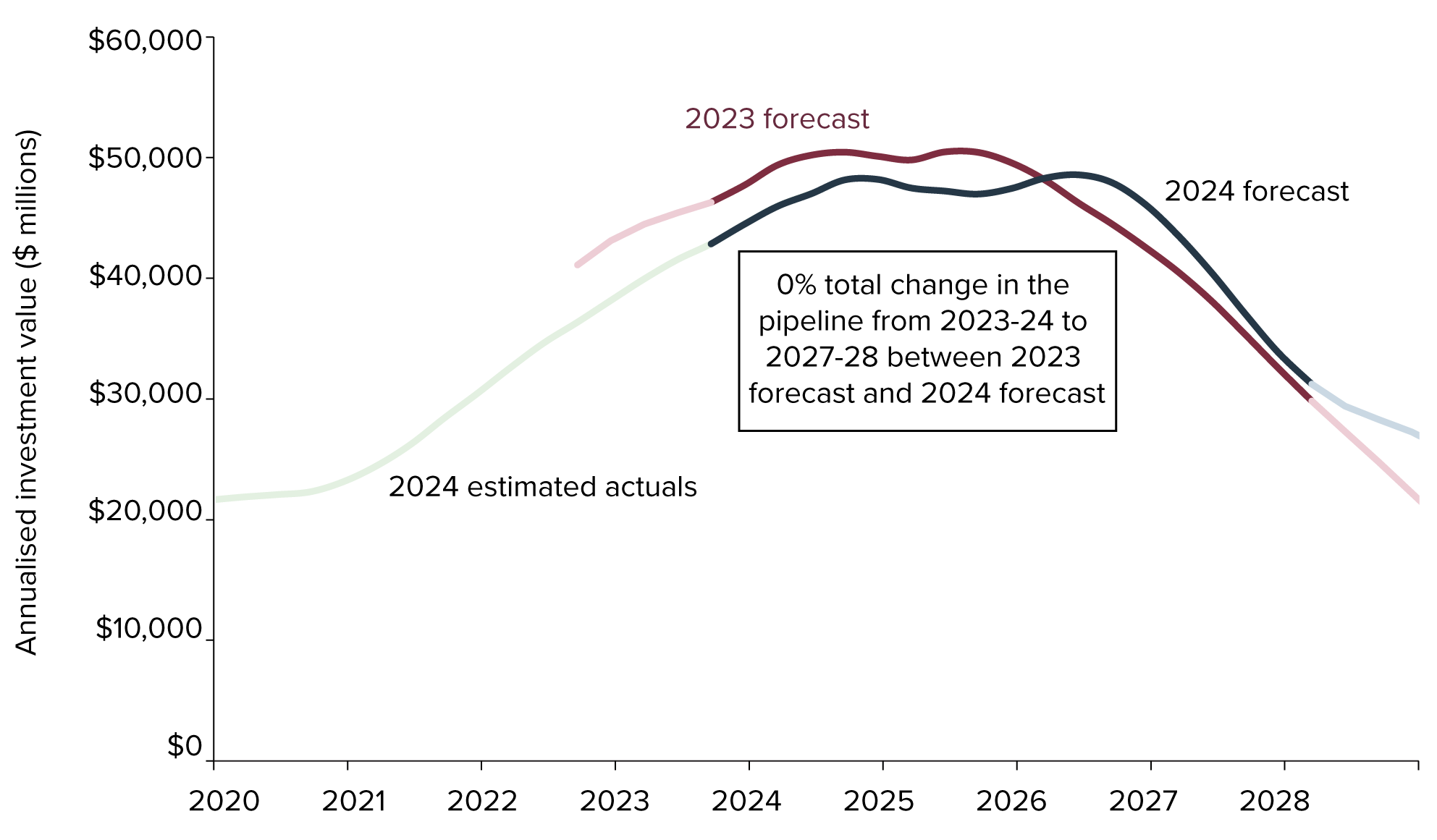

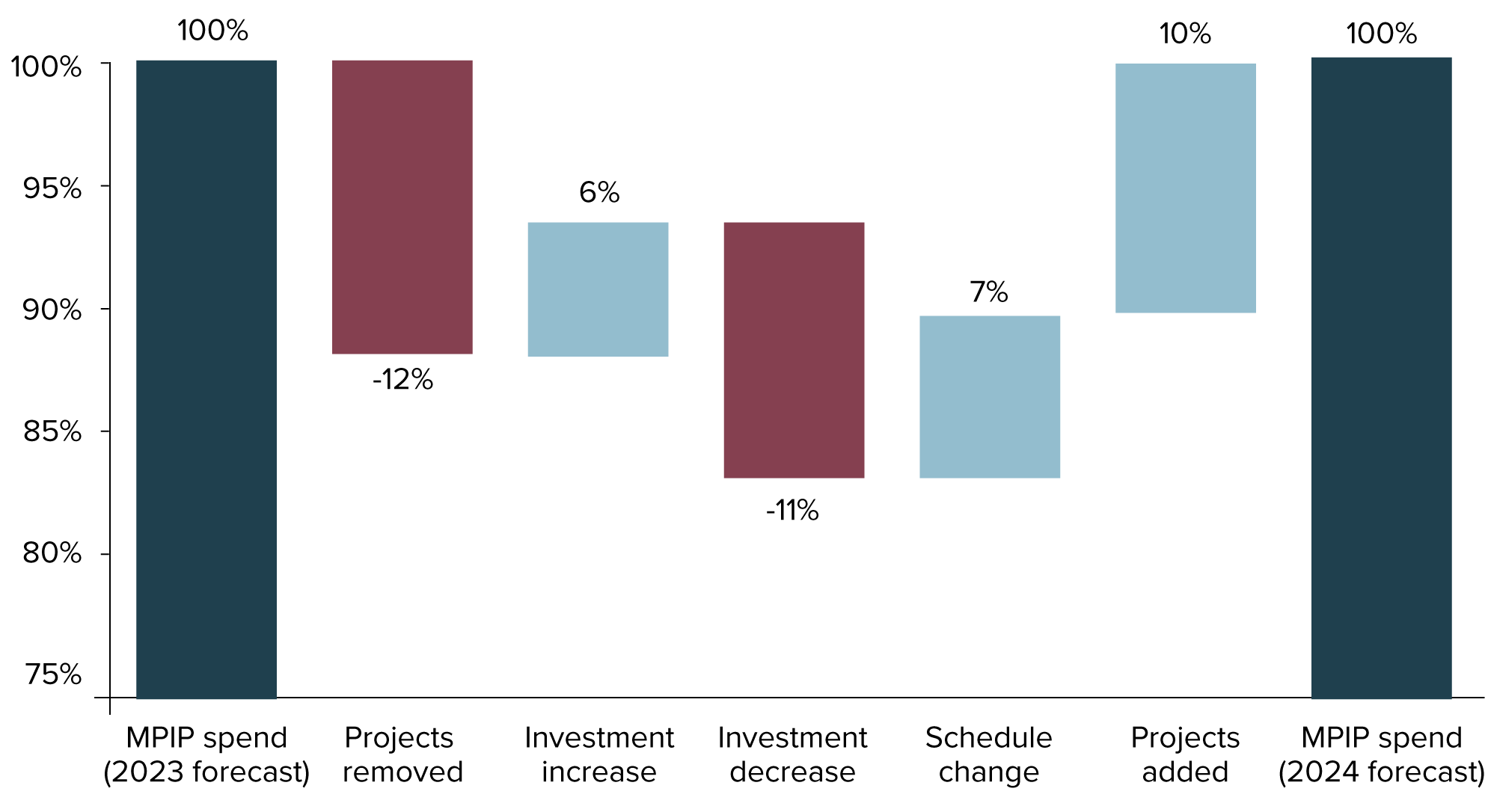

Like-for-like analysis of how project estimates have changed in the past 12 months reveals the drop in demand is primarily driven by projects recently completed or removed from the pipeline

Infrastructure Australia conducted an in-depth year-on-year analysis, comparing estimates of the Major Public Infrastructure Pipeline from 2023 and from 2024 for the same 5-year period (2023–24 to 2027–28, as shown in Figure 4). Unlike last year when we reported that the pipeline had increased by 13% for this exercise, this year the 2024 forecast is the same as the 2023 forecast for the specified time period.

Figure 4: Comparison of 2023 and 2024 forecasts of Major Public Infrastructure Pipeline activity (2023–24 to 2027–28)

By studying a sample of over 600 on-going major public infrastructure projects in the 2023–24 to 2027–28 pipeline using data from both the 2023 and 2024 pipeline estimates, we identified changes in the pipeline, as visualised in Figure 5.

The pipeline decreased by 12% due to projects being removed or recently completed, with a further 11% drop from investment cuts in continuing projects.

The magnitude of 23% in reductions has not quite been netted out by new projects coming into the pipeline (10%, predominantly in the buildings sector) and increases to investment estimates (6%), leaving another 7% in increases still to be explained.

The remaining 7% increase year on year is explained by delays to project schedules. Schedule changes to several projects where construction has been delayed versus the estimates of one year earlier, had the effect of shifting project investment from 2022–23 out to later years. Where this shift occurred, we quantified the 2024 estimate as being 7% higher than the 2023 estimate for 2023–24 to 2027–28.

Figure 5: Major Public Infrastructure Pipeline spend from 2023–24 to 2027–28, changes from 2023 forecast to 2024 forecast

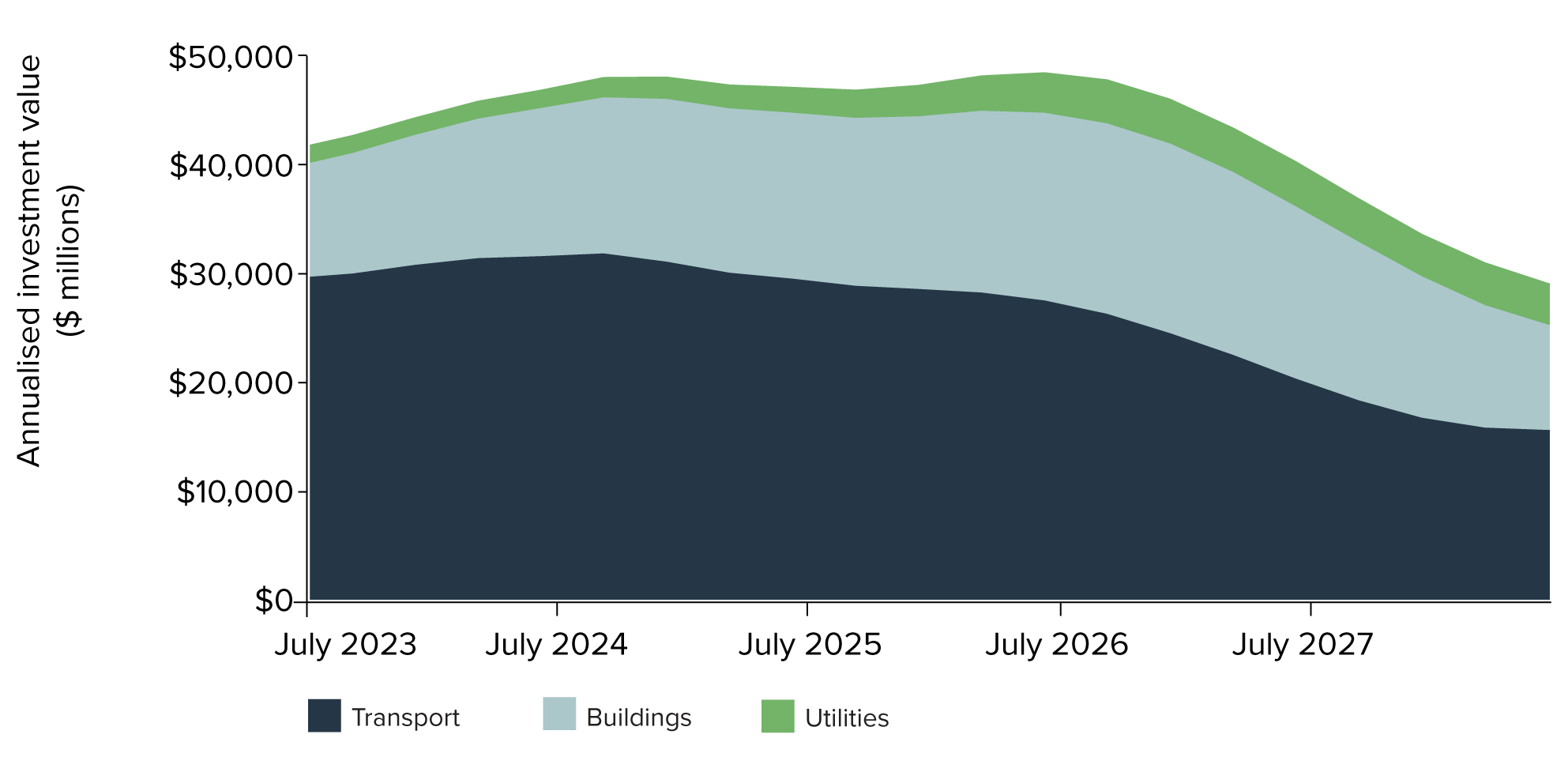

Transport remains the largest public infrastructure expenditure category but has declined this year, while building and energy investment continue to grow

Figure 6 shows investment in the Major Public Infrastructure Pipeline over the 2023–24 to 2027–28 outlook period, as broken down by sector.

Transport infrastructure investment is projected at $126 billion and remains the largest expenditure category, accounting for 59% of the Major Public Infrastructure Pipeline. This is a $32 billion reduction on the previous year’s outlook, driven by:

- Completions of megaprojects in 2023–24.

- Fewer new projects to commence in coming years versus the previous outlook period.

- Cost and schedule changes in the total investment estimates, for some megaprojects due to commence construction in the outlook period.

Buildings infrastructure investment is projected at $71 billion, which accounts for 34% of the Major Public Infrastructure Pipeline. This is up $8 billion on the previous year’s outlook. Buildings infrastructure is driven by health ($24 billion) and residential buildings ($17 billion), followed by other building types such as convention centres, offices, art facilities and laboratories ($12 billion).

Utilities infrastructure investment is projected at $16 billion, which accounts for 7% of the Major Public Infrastructure Pipeline. This is up $6 billion on the previous year’s outlook. While investment in energy projects is mainly driven by the private sector, significant public investment can be seen in large transmission projects.

Analysis of projected demand peaks by sector over the five-year outlook shows that while transport investment is expected to continue to decline, buildings infrastructure is expected to peak in 2026, while energy investment is expected grow steadily. The staggered demand peaks by sectors have an effect of maintaining a steadier level of overall investment across infrastructure.

When interpreting these projections, it should be noted that the Major Public Infrastructure Pipeline accounts for only a quarter of the total construction market and there is significant private investment in buildings and particularly in energy infrastructure.

Figure 6: Major Public Infrastructure Pipeline spend by sector (2023–24 to 2027–28)

Analysis of regional demand sees growth across northern Australia

Regional analysis of the pipeline has been made possible for the first time this year, through the development of analytical tools created in 2023 by Infrastructure Australia in collaboration with state and territory governments. These tools are designed to help government decision makers diagnose labour-supply bottlenecks, spot growth opportunities and build strong evidence bases for investment decisions.

Two analytical tools are fundamental to this regional analysis: a national heat map of construction demand and supply, and a demand pipeline simulator – both of which analyse investment demand, material demand, and labour demand and supply.

In the five years from 2023–24 to 2027–28, when compared with the corresponding period in the 2023 forecast, there is a significant geographical shift in public investment to the north, with the Major Public Infrastructure Pipeline in Queensland and Northern Territory growing by $16 billion, while New South Wales and Victoria have reduced by $39 billion.

Deep dive: contribution of cost pressures by resource type

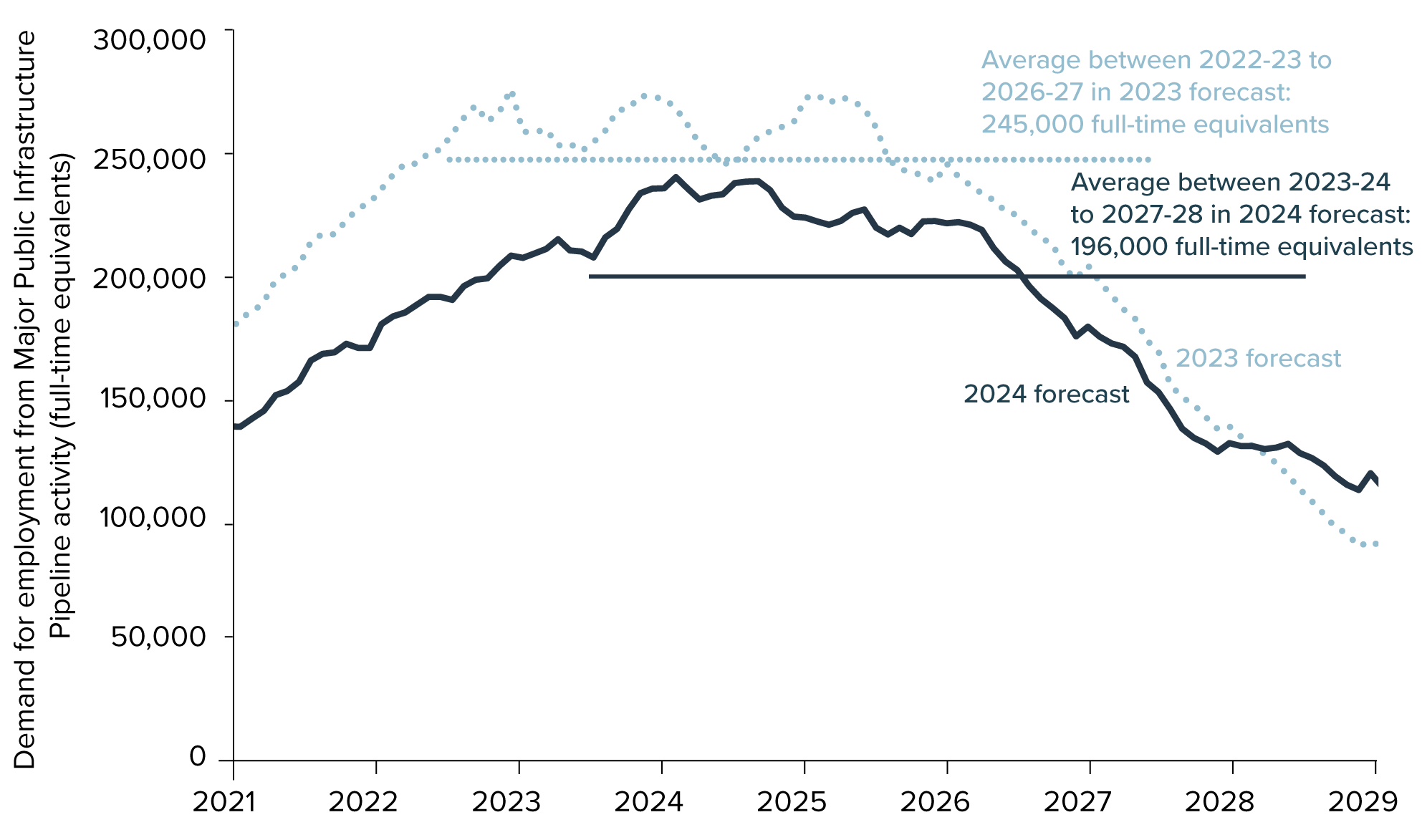

In 2024, Infrastructure Australia undertook a deep dive of the contributions to cost escalation on the Major Public Infrastructure Pipeline by PLEM (Plant, Labour, Equipment, Materials) resource types. This analysis breaks down the total project cost escalation into its constituent parts, allowing us to identify the contribution of each resource type to the overall escalation.

We have comprehensively reviewed and updated our Market Capacity Program cost assumptions this year (based on the Australian Bureau of Statistics Producer Price Index and Wage Price Index) to ensure our cost estimates and assumptions reflect current economic conditions.

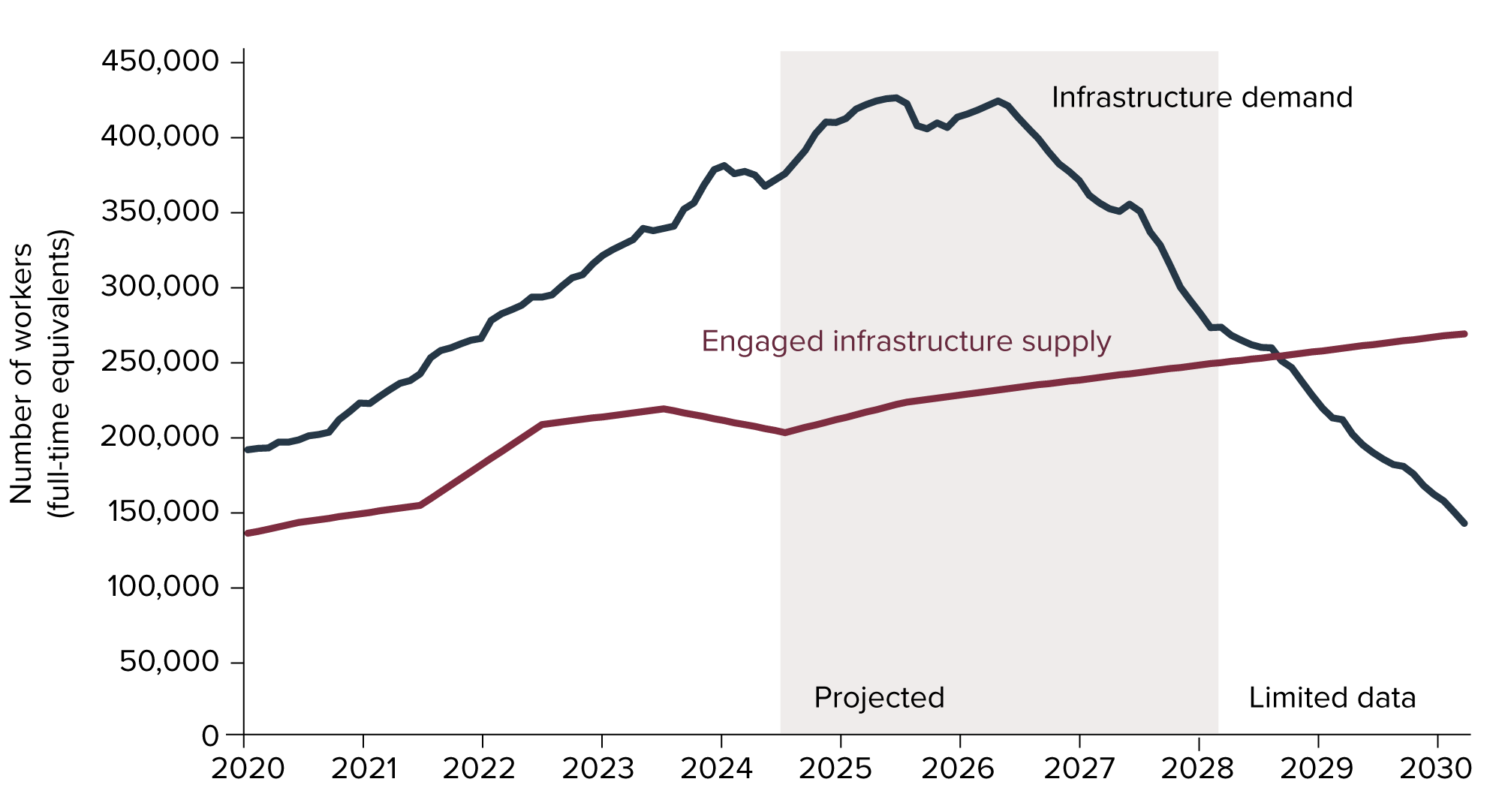

As shown in Figure 7, applying the updated cost assumptions to the Major Public Infrastructure Pipeline this year, average labour demand dropped by 20% in full-time equivalents per month compared to last year’s projection.

Figure 7: Comparison of 2023 and 2024 forecasts of demand for labour from the Major Public Infrastructure Pipeline (2020–21 to 2027–28)

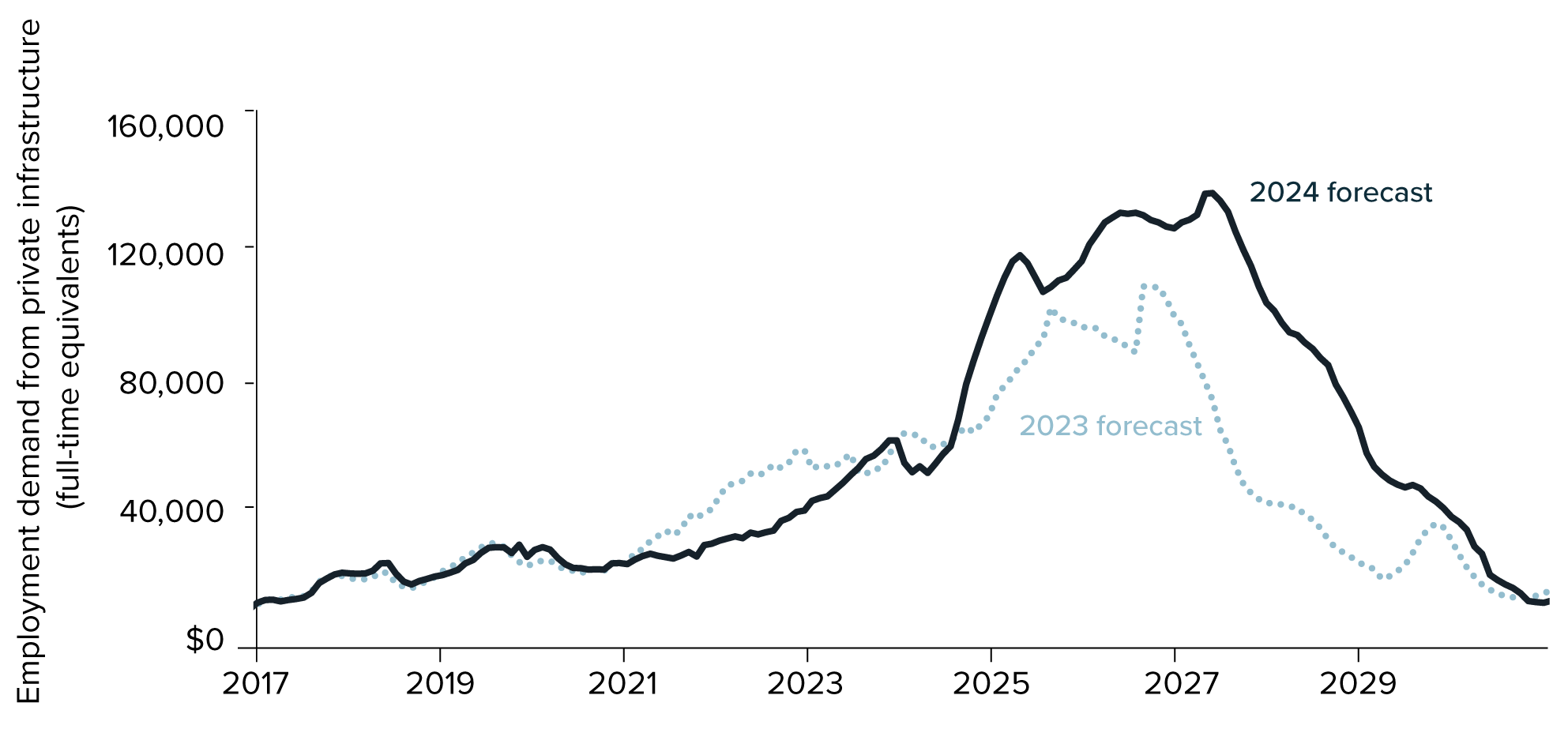

Preparedness is needed for the workforce to deliver private-funded infrastructure demand

In terms of private investment (that is, separate to the Major Public Infrastructure Pipeline), we observed a jump in labour demand from the private infrastructure sector in the near future. This is driven by the renewable energy transition. As shown in Figure 8, from early 2027, labour demand from private infrastructure will almost double when compared with the forecast from 2023.

The top 5 occupations needed to deliver energy projects over the five-year outlook are Other Professional Engineers (those not classified as civil, electrical, industrial, mechanical or production engineers), General Construction Labourers, Electricians, Plant Operators and Project Managers.

Figure 8: Comparison of 2023 and 2024 forecasts of demand for labour from private infrastructure (2020–21 to 2027–28)

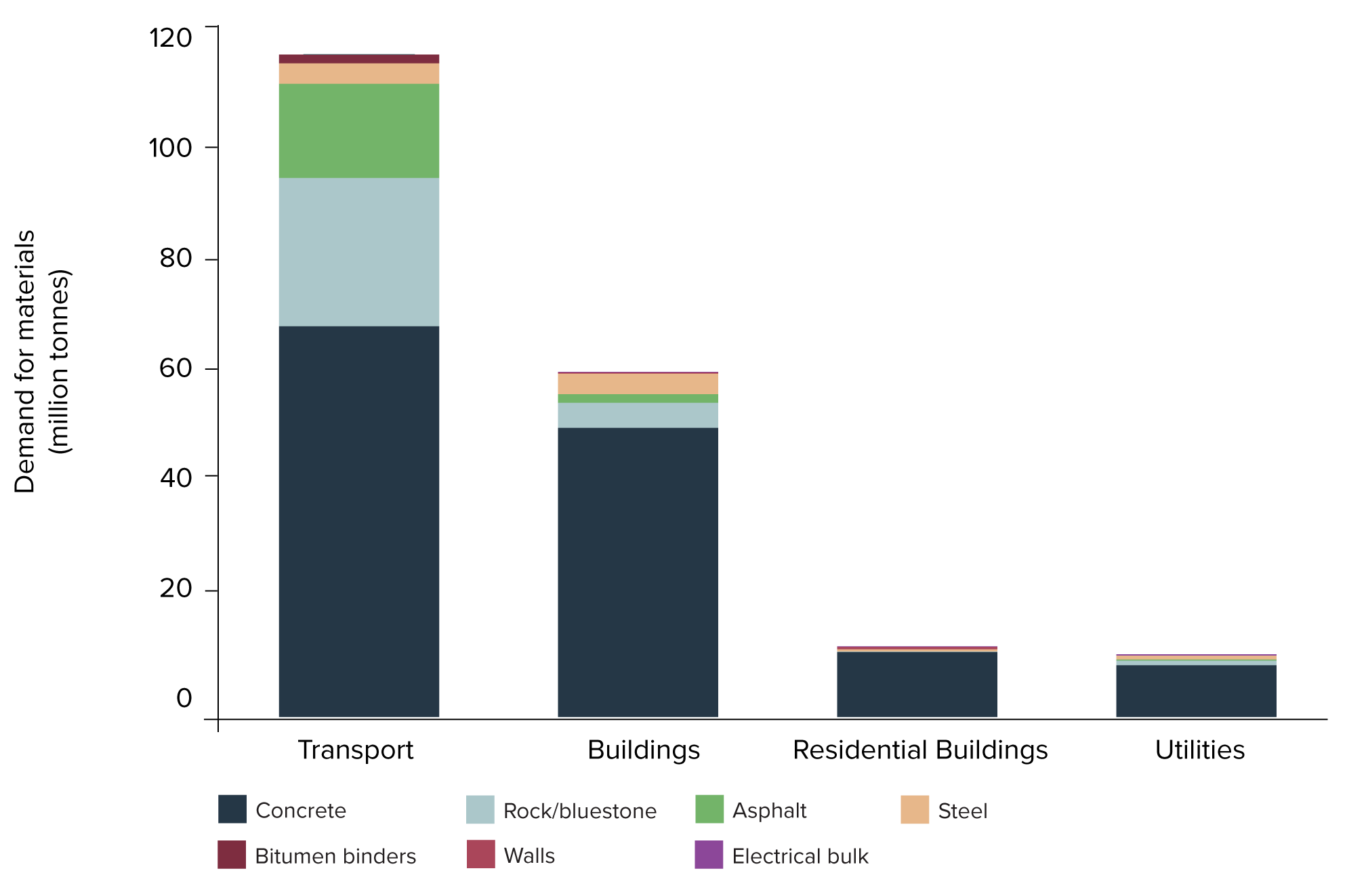

Demand for concrete and steel cuts across all construction sectors, while demand for other materials varies by sector

By cost shares, materials accounts for the largest proportion (73%) of total non-labour spend on the Major Public Infrastructure Pipeline, followed by plant (15%) and equipment (11%).

As shown in Table 2, concrete is the top construction material needed by volume to complete major infrastructure works over the five-year outlook (137 million tonnes), followed by rock/bluestone (31 million tonnes), asphalt (18 million tonnes) and steel (8 million tonnes).

Table 2: Demand for materials from the Major Public Infrastructure Pipeline (2023–24 to 2027–28)

| Material | Demand (million tonnes) | |

|---|---|---|

| Concrete | 136.8 | |

| Aggregate | 80.0 | |

| Cement | 22.4 | |

| Sand | 34.4 | |

| Rock/Bluestone | 30.6 | |

| Asphalt | 18.0 | |

| Steel | 8.1 | |

| Steel – Structural Elements | 3.8 | |

| Steel Reinforcement | 3.6 | |

| Girders | 0.6 | |

| Rail Track | 0.1 | |

| Bitumen Binders | 1.5 | |

| Walls | 0.7 | |

| Timber | 0.3 | |

| Plasterboard | 0.3 | |

| Bricks | 0.1 | |

| Electrical Bulk | 0.2 | |

| Aluminium | 0.1 | |

| Copper | 0.04 | |

| Plastics and Polymeric Materials | 0.03 | |

| Electric Bulk | 0.01 | |

| Fibreglass | 0.01 | |

| PV Panels | 0.003 | |

As shown in Figure 9, across major public infrastructure works, materials demand is mostly driven by transport, due to its dominant position on the Major Public Infrastructure Pipeline, followed by buildings and utilities. As all sectors will be consuming concrete (aggregate/sand/cement) in bulk, it may be subject to cross-sector competition in the event of supply shortages.

To remove the impact of pipeline size, we analysed materials required per $ million to normalise data and understand material requirement per sector. In doing so, we observe that steel is another material that is critical to delivery shared cross all sectors.

To deliver $100 million of investment, we need:

- 64 tonnes of steel for other buildings

- 44 tonnes for utilities

- 28 tonnes for transport

- 23 tonnes for residential buildings.

Asphalt and rock/bluestone are materials heavily needed for transport projects and non-residential building types. Wall materials (bricks, plasterboard, timber) on the other hand are unique to residential buildings.

Figure 9: Demand for materials from the Major Public Infrastructure Pipeline by sector (2023–24 to 2027–28)

Industry view

Most businesses report capacity as being the same or worse than last year, and a third expect work will increase in the next two years

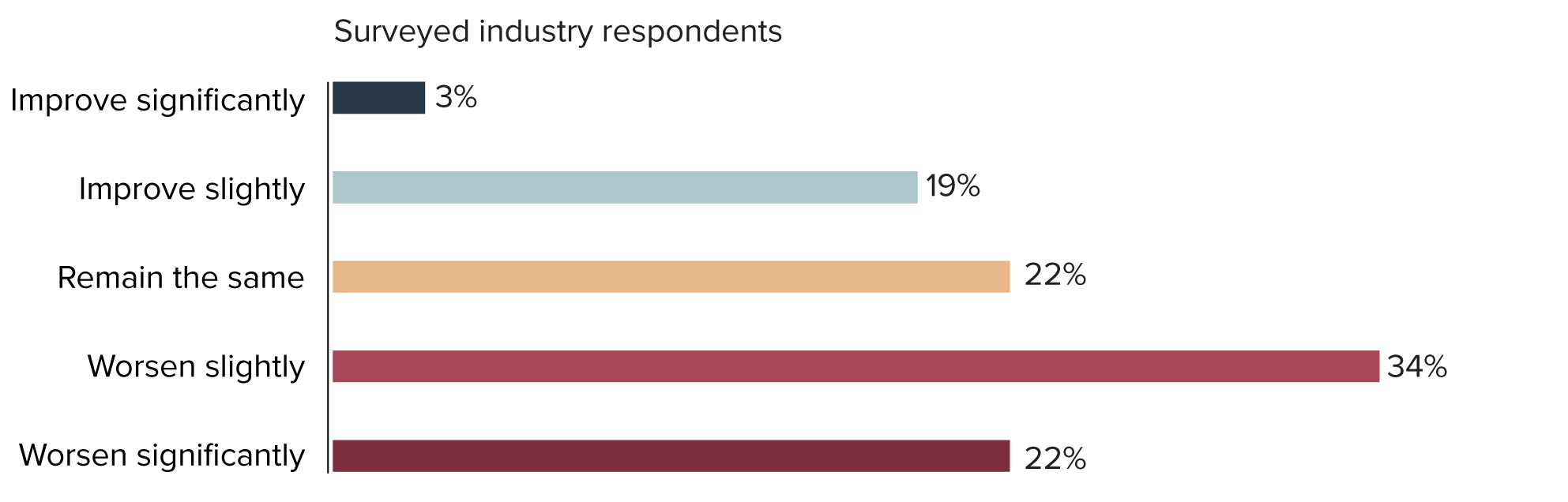

When it comes to industry’s assessment of current market capacity compared to the previous year, 64% of surveyed building and construction businesses felt it was the same, 26% believed it was worse and 6% felt it is ‘not as challenging’ as last year. There were no significant variations in responses across industry subsectors or size of contracts delivered.

When looking two years ahead, approximately 40% of surveyed businesses expect capital project activity to stay about the same as current levels, with almost a third (32%) believing it will increase and a fifth (22%) believing it will decrease.

By sector, more businesses in the utilities and transport sectors (over 40%) anticipate an increase in activity levels over the next two years than other sectors (housing, mining and commercial). A smaller proportion (32%) of residential-construction businesses expect activity levels to increase compared to 42% expecting activity to stay the same. These responses are slightly at odds with the pipeline-demand data that shows growth in residential buildings investment and a decrease in transport investment over the forward estimates compared to the previous years’ projections.

The market observes a ‘two speed’ economy with demand driven by Queensland and falling in the New South Wales and Victoria

Industry notes diverging pipeline pressures in different states, observing many active or large infrastructure projects planned in some states such as Queensland, while in New South Wales and Victoria, government spending has reduced, and pipelines are lengthening.

These views align with Infrastructure Australia’s analysis of the Major Public Infrastructure Pipeline over the forward estimates, with more subdued overall demand compared to previous projections characterised by weaker investment in east-coast states and growth up north.

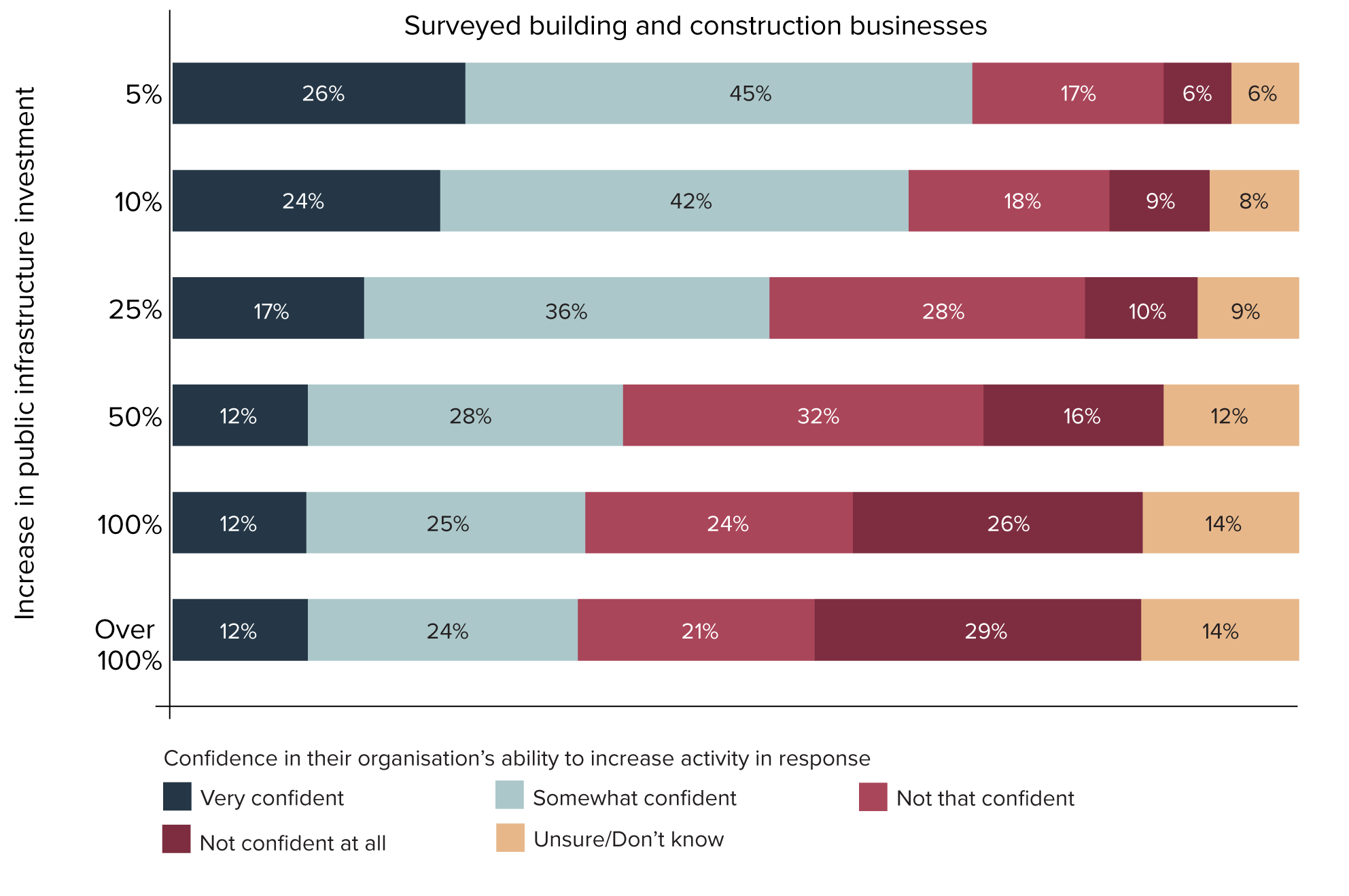

Industry is confident to scale up operations moderately, with residential sector least confident to scale up

As shown in Figure 10, when asked to rate their confidence to scale up in response to increased investment in public infrastructure across a few growth scenarios (scale up by 5%, 10%, 25%, 50%, 100% or over 100%), most businesses believe they have the capacity to scale up to meet increased activity to a degree. Over half (53%) were very or somewhat confident in their ability to scale up their activity by 25%. However, confidence to push beyond this then starts to drop with 40% of businesses confident to scale up their activity by 50%, and 37% confident to scale up by 100%.

Figure 10: Confidence of building and construction businesses in their ability to increase activity to meet increased public infrastructure investment

Source: Infrastructure Australia Industry Confidence Survey (2024)

Consistently, businesses in the mining sector reported highest confidence to scale up, followed in order by the utilities, transport and commercial sectors. Businesses in the residential construction sector reported the lowest confidence levels to scale up. This suggests the residential construction sector is experiencing more significant capacity constraints of all construction sub-sectors.

Businesses delivering larger contracts have greater confidence to scale up. Across all growth scenarios, companies delivering contracts over $100 million are more confident to scale that those delivering contracts between $10 million and $100 million. Companies delivering contracts less than $10 million in value have consistently less confidence to scale up than the two prior-mentioned groups.

Of those surveyed among the Civil Contractors Federation’s member base, representing a majority smaller Tier-3 businesses, nearly a third (31%) reported that if there was an increase in the number of projects tendered in their respective state, they could take on between 10–25% extra work. This is compared with a little over a fifth (21%) who said they could take on between 25–50% more work. Where these members suggest they have extra capacity to take on additional projects, nearly 80% said they could take on the most work in rural and regional areas, compared to 64% who reported capacity to take this extra work within metropolitan areas.

During interviews, businesses also noted the current economic environment, including inflation, rising costs and interest rates, as a challenge affecting project viability and profitability, which in turn is impacting on overall capacity

Section 2: Non-labour supply Summary

This section provides an assessment of non-labour demand and supply. It includes an overview of supply risks for key construction materials, as viewed by industry, and a snapshot on the status of key materials, plant and equipment supply this year.

Following from the recommendation made in the 2023 Infrastructure Market Capacity Report to “undertake analysis of domestic steel production and fabrication capacity…to strengthen and support sovereign supply chain capability and grow new capacity for future industries”, we provide a deep dive on domestic steel fabrication capacity using data provided by the Australian Steel Institute.

The section concludes with industry views of non-labour supply issues, collected from our 2024 industry surveys and interviews.

Key points

- The cost of construction materials continues to remain high with most materials experiencing year-on-year growth for three straight years. However, the rate of growth appears to have eased over the past twelve months, driven largely by drops in the price for some steel products.

- Industry reports price escalation of non-labour inputs over the last 12 months of about 10–20%, and believe prices are yet to peak.

- Concrete and steel, the construction materials most in demand, are vulnerable to cross-sector competition in the event of supply shortages.

- An analysis of Australia’s steel fabrication capacity shows that over two thirds of domestic capacity is located across New South Wales, Queensland and Victoria. The Northern Territory, with less than 1% of national steel-fabrication capacity while requiring 7% of demand, will be the most challenged to source local supplies and rely heavily on imports.

- Less is known about domestic capacity to supply steel fabrication needed for renewable energy projects, which requires specialised components that are typically imported, nor the roads infrastructure needed to transport large equipment, such as wind turbines, from supply source (domestic or imports) to project site.

- Improved visibility of demand against local supply of key construction materials gives the market a clearer understanding of gaps and opportunities. This enables industry to expand capacity to support planned infrastructure delivery and achieve net-zero targets via new growth areas such as green steel and recycled materials.

Section 2: Non-labour supply

Boost non labour supply – future directions

The Australian Government, in partnership with state and territory governments, should continue to expand construction non-labour supply through:

- improving monitoring local production capacity of key construction materials. This could include industry collaborations such as the work done with the Australian Steel Institute for this report.

- exploring opportunities to coordinate national demands for specific materials or equipment facing strong global competition and long lead times in light of the energy transition and the enabling infrastructure needed to deliver it.

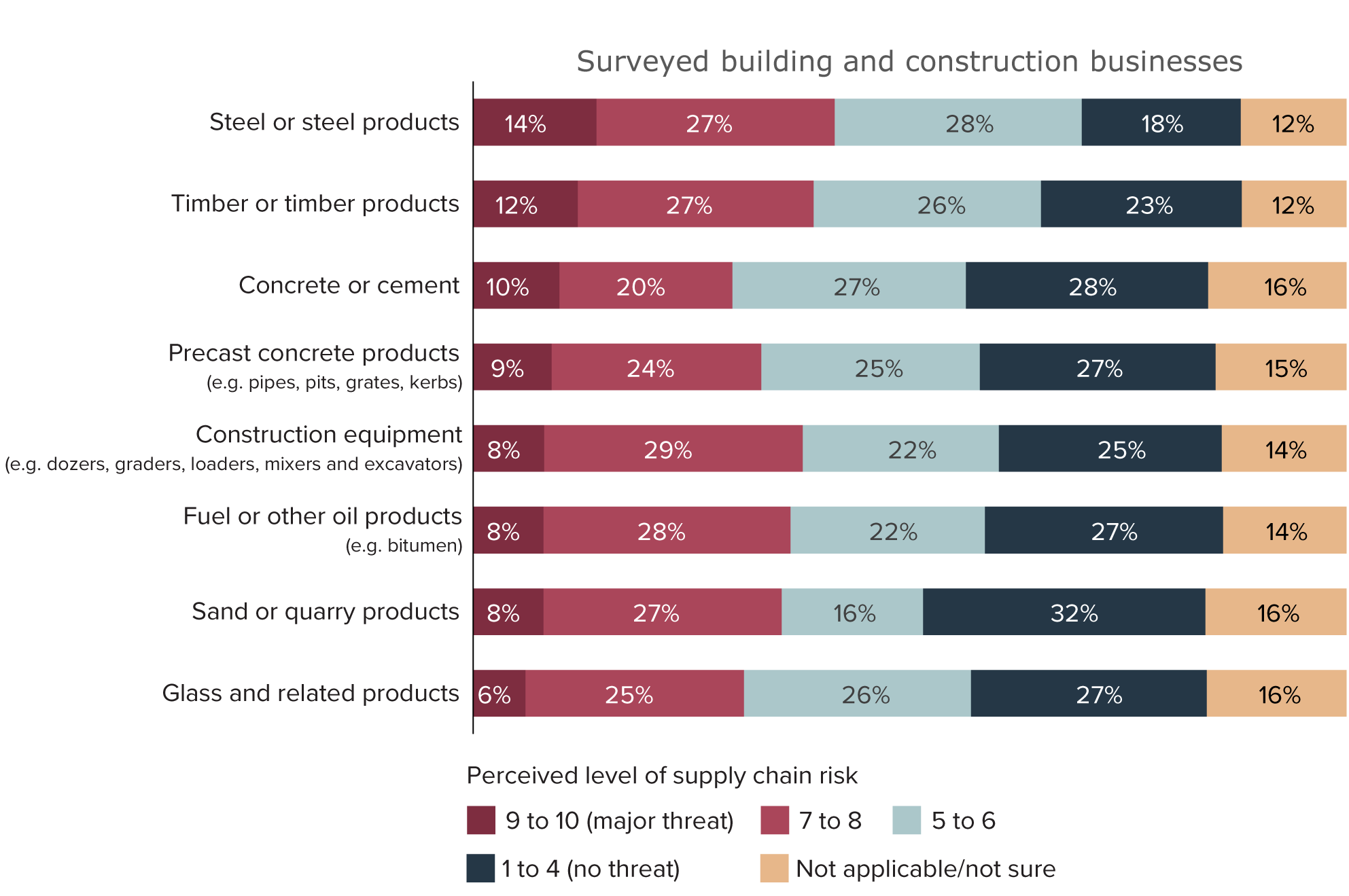

Supply of steel and timber cited by industry as being a critical delivery risk this year

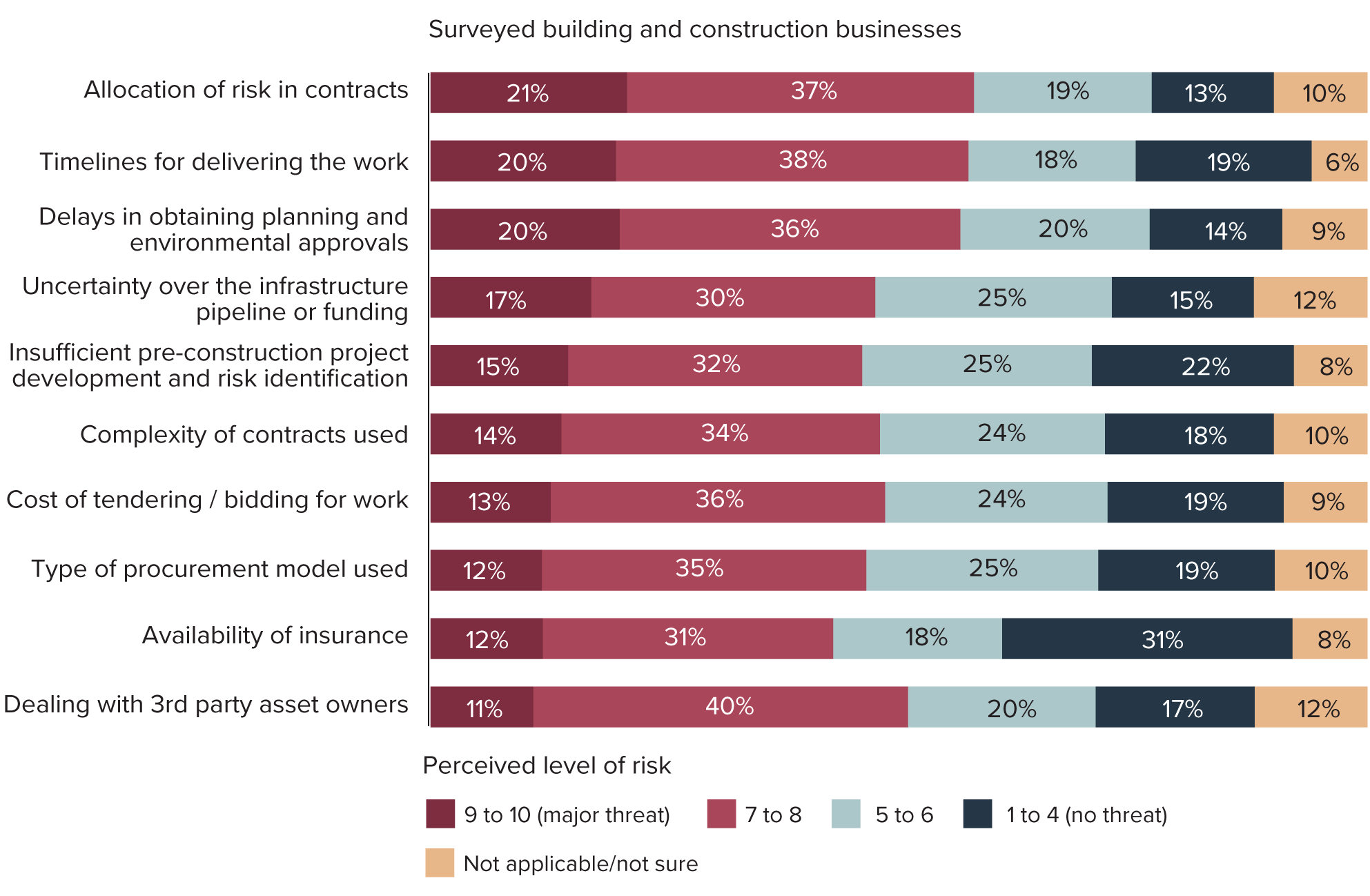

Businesses surveyed as part of the 2024 Industry Confidence Survey regarded most materials as posing some level of supply-chain risk. As shown in Figure 11, steel and timber supply were most often cited (rated as 9-out-of-10 or 10-out-of-10 risk by 14% and 12% of surveyed businesses, respectively), followed by concrete/cement and construction equipment as posting a threat to project delivery.

Figure 11: Views of building and construction businesses on materials supply threats to infrastructure projects delivery

Source: Infrastructure Australia Industry Confidence Survey (2024)

Table 3 provides a snapshot of key construction material, plant and equipment supplies in 2024.

Table 3: Key construction non-labour supply – 2024 insights

| Construction material/plant and equipment | 2024 insights and implications |

|---|---|

| Steel and steel fabrication | Steel product prices have dropped this year, driven by a combination of factors, including weakening global demand, increased production capacity, and fluctuations in raw material costs (such as for iron ore).5 Imports of steel products, particularly specialised ones like stainless steel and tool steel, remain significant (see Figure 16). A majority of surveyed local steel fabricators and manufacturers (86%) report reduced profit margins due to cheap imported fabricated steel, which is priced between 15% and 50% lower than locally produced steel (as reported by the Australian Steel Institute survey conducted in in July 2024). Reliance on imported steel exposes construction projects to risks related to fluctuating prices, transport costs, and potential supply disruptions. |

| Quarry products | Some governments have taken measures to address quarry supply risks. The Victorian Government has ramped up approvals for new quarries to meet growing infrastructure demands and aims to stabilise supply and reduce costs, with 300 million tonnes of new quarry resources approved for development.6 Queensland quarry demand and supply risks report indicates that demand for hard rock and sand can be met by reserves in existing quarries.7 |

| Concrete | Concrete production depends heavily on quarry product availability. Stricter sustainability standards and environmental regulations could lead to higher concrete production costs and potential supply delays.8 Precast concrete continues to experience long lead times due to high demand, particularly in infrastructure projects.9 These factors are putting pressure on the availability of concrete for large-scale projects. |

| Plant and equipment | The construction industry continues to experience delays in securing plant and equipment, driven by high global demand and geopolitical issues. Ongoing supply-chain bottlenecks are expected to extend lead times for essential equipment, affecting project timelines. The Australia construction machinery market size is expected to reach USD 3.29 billion by 2029, growing at a compound annual growth rate of 3.35% during 2024–2029, indicating supply responses to demand pressures driven by increased infrastructure investment.10 |

| Timber | Australia’s timber supply is facing significant challenges due to the combined effects of regulatory changes and environmental risks. Hardwood can be replaced with more expensive composite wood alternatives.14 |

| Cement | Cement production remains under pressure due to rising energy costs and stricter environmental regulations, which have forced some local cement plants to scale back operations or shut down.15 This has led to an increased dependence on imported clinker and other materials necessary for cement production. The global cement market is also experiencing disruptions due to geopolitical tensions and trade restrictions, which are affecting the availability and cost of imports. Price of cement products increased 2.4%, driven by fibrous cement products (3.3%), linked to increase in costs in labour, energy and freight inputs.16 |

| Plasterboard | The plasterboard industry faces rising energy costs, which are increasing production costs. No significant supply issues are currently reported, but higher energy expenses are expected to impact the price of plasterboard.17 The industry is also beginning to face increased demand for sustainable products, which may require additional investment in innovative technologies and processes. |

| Bitumen | The global bitumen market is expected to grow from $53.66 billion in 2023 to $56.23 billion in 2024 at a compound annual growth rate of 4.8%.18 Australia’s reliance on imported bitumen continues to pose risks, especially as global oil markets face volatility due to geopolitical tensions and environmental regulations. |

Cost of materials still increasing but at lower rate

The cost of construction materials continues to remain high, with the majority of materials experiencing year-on-year growth for three straight years. However, the rate in which these materials have grown has largely eased over the past twelve months, with average annual price growth for all materials being 8% lower than in 2023 (average growth of 4.3% in 2024 versus 12% in 2023).

As shown in Figure 12, while this slow down in price escalation was felt across the board, it was largely driven by large drops in the price for steel beams and sections, and reinforcing steel, which decreased over the year by 16% and 8%, respectively. For these materials, this is a notable shift in the annual changes in the prices Infrastructure Australia observed in 2022, when the prices for these materials had increased beyond 30%. There were, however, some outliers to the broader trend for this year, with clay bricks, coating, and electrical products experiencing significant increases.

Some of these material cost escalations are being driven by conflicts in Ukraine and the Middle East, which are disrupting international supply chains. The conflict in the Middle East, for example, has seen disruptions to shipping routes, which are adding substantial costs to the transportation of materials. However, overall the increases in costs are stabilising and becoming more predictable, especially as Australia continues to move past the post-COVID-19 period.

Figure 12: Annual % input price changes for house construction materials (2021–22 to 2023–24)

Source: Australian Bureau of Statistics (2024)19

Prices of imported materials have been stable over the last 12 months

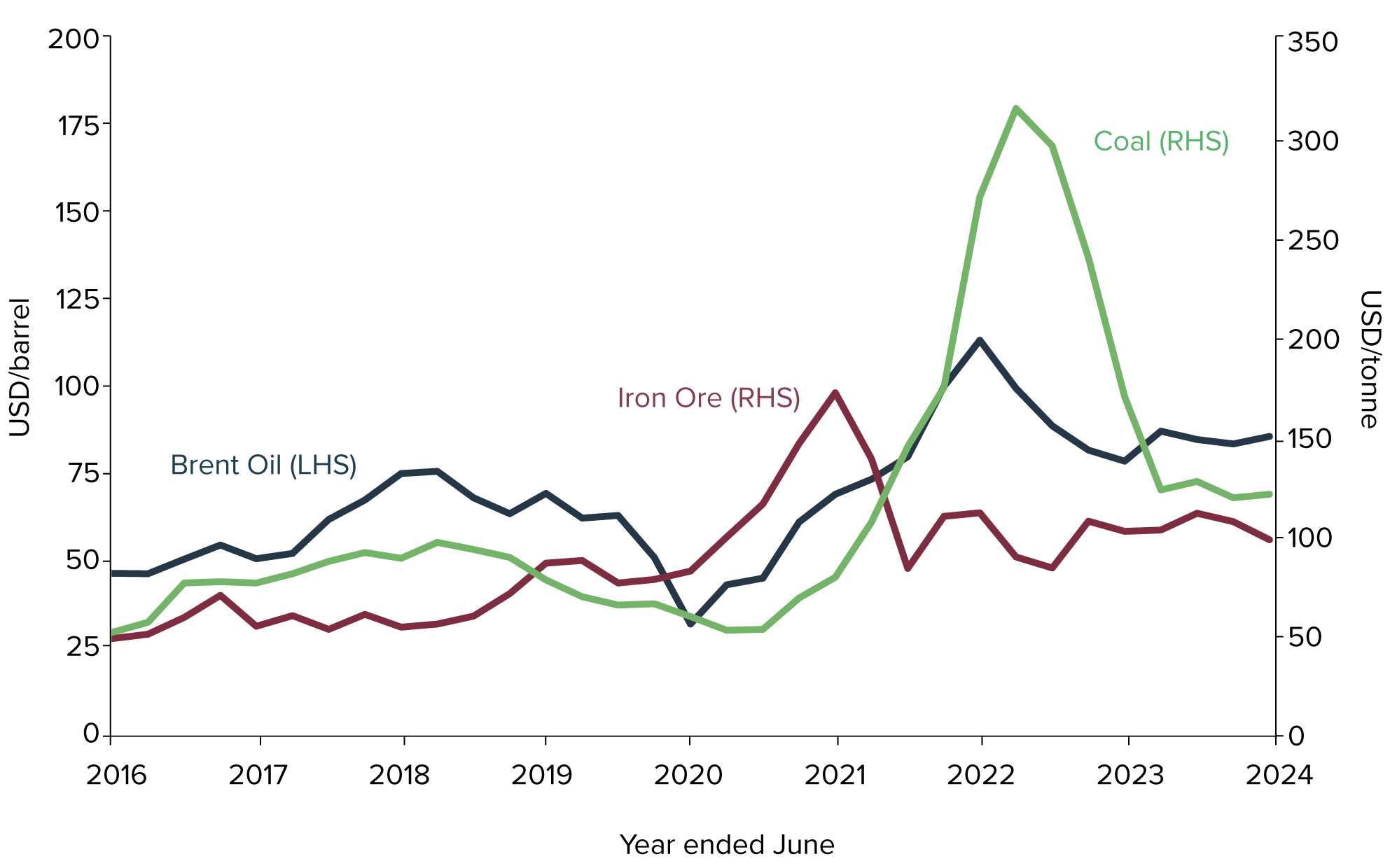

Over the past 12 months, the prices of oil, coal and iron ore have continued to fluctuate. While these prices are expected and not unusual, these fluctuations were not as extensive as they were in previous years.

When compared with the nature of the price fluctuations in 2021, 2022 and 2023, the prices for these materials throughout 2024 can be described as being much more stable. That is, they did not experience such wild swings in price points, which were caused by the COVID-19 pandemic, the start of the conflict in Ukraine, and renewed geopolitical tensions and conflicts within the Middle East. These events saw significant disruptions to supply chains and demand. For instance, conflict in the Middle East, especially disruptions to shipping routes in the Red Sea, has driven up shipping costs as companies are forced to reroute, resulting in longer and more expensive journeys.

Additionally, there is strong demand for materials such as iron ore from China, driven by the country’s significant infrastructure boom. As conflicts in Ukraine and the Middle East persist, along with global demand for materials, these factors will continue to influence material prices. However, this impact is likely to be more predictable than what has been experienced in the past. Figure 13 shows minimal change in the price of imported oil, iron ore and coal over last 12 months, following periods of greater variability.

Figure 13: Changes in oil, coal and iron ore prices (2016 to 2024)

Source: Department of Industry, Science and Resources (2024)20

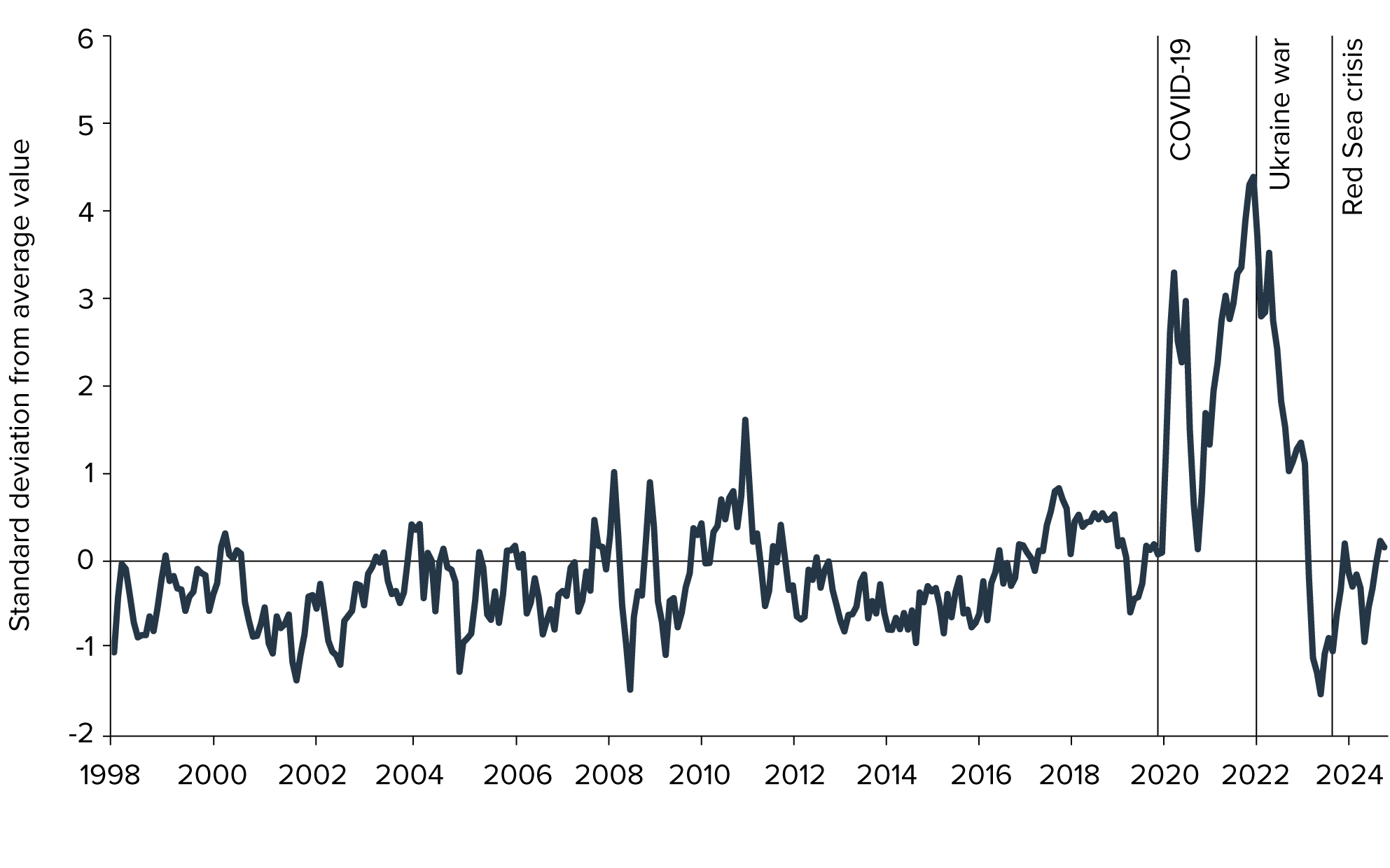

Freight schedules and costs were impacted by global supply chain disruptions

Events such as conflicts in Ukraine and the Middle East continued to disrupt global supply chains earlier in 2024. Figure 14 shows their impact on the Federal Reserve Bank of New York’s Global Supply Chain Pressure Index.

Figure 14: Global Supply Chain Pressure Index including key events (1998 to 2024)

Source: Federal Reserve Bank of New York (2024)21

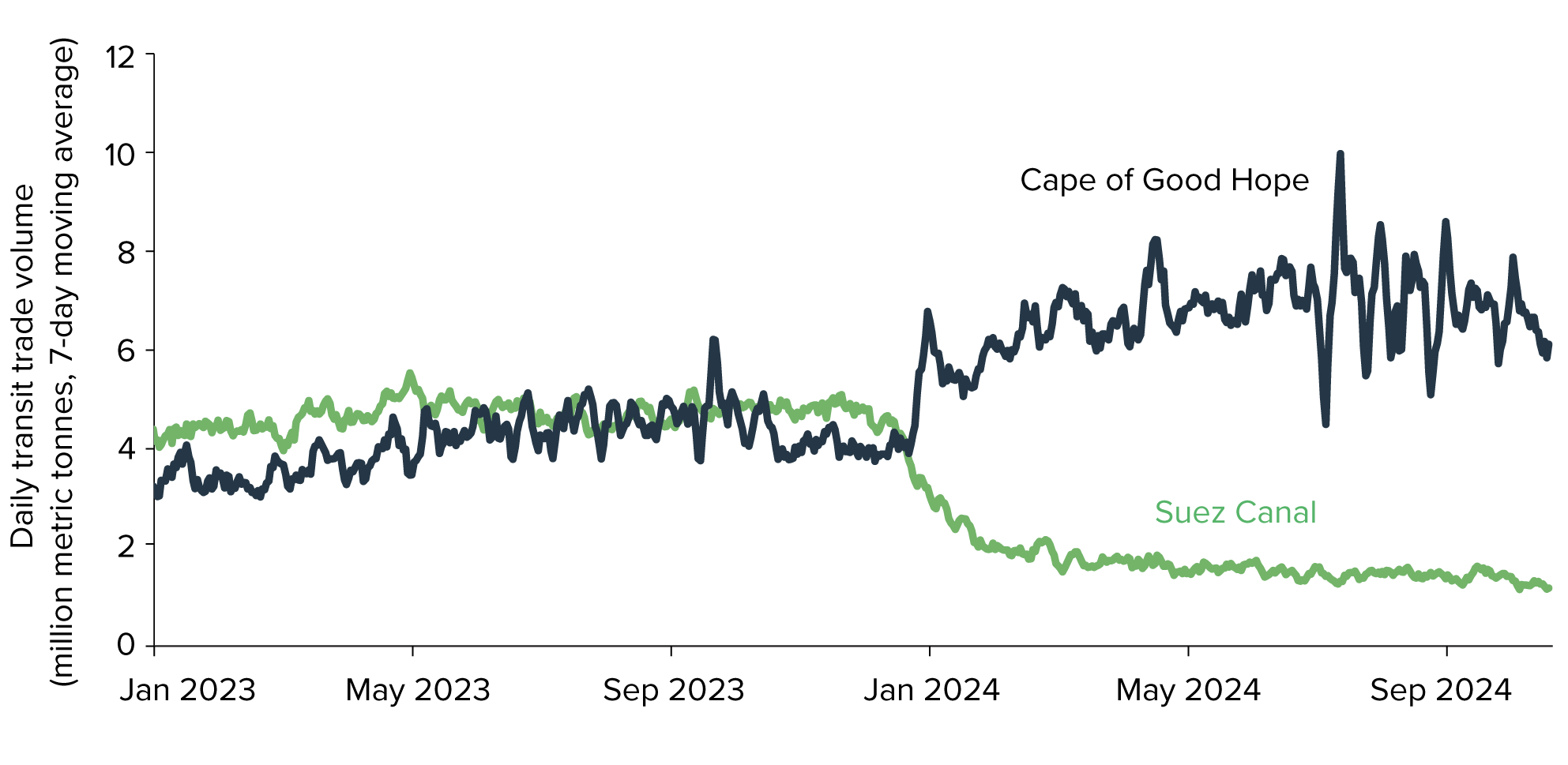

In January and February, conflict in the Red Sea had a major impact on key global trade routes. As shown in Figure 15, trade volumes through the Suez Canal – the crux of Europe and Australasia’s shortest maritime route – were 50% lower than in 2023. As a result, trade levels surged around South Africa’s Cape of Good Hope due to re-routed freight.

Cost impact: The Australian Bureau of Statistics links a 1.2% rise in water freight (shipping) prices to the Red Sea conflict, while noting the increase followed six consecutive quarters of price drops.22

Schedule impact: The average journey time of rerouted freight was 26 days, which is 19 days (55%) longer than average equivalent freight trips through the Suez Canal.23

Figure 15: Daily transit trade volumes for Suez Canal and Cape of Good Hope (January 2023 to October 2024)

Source: International Monetary Fund Port Watch (2024)24

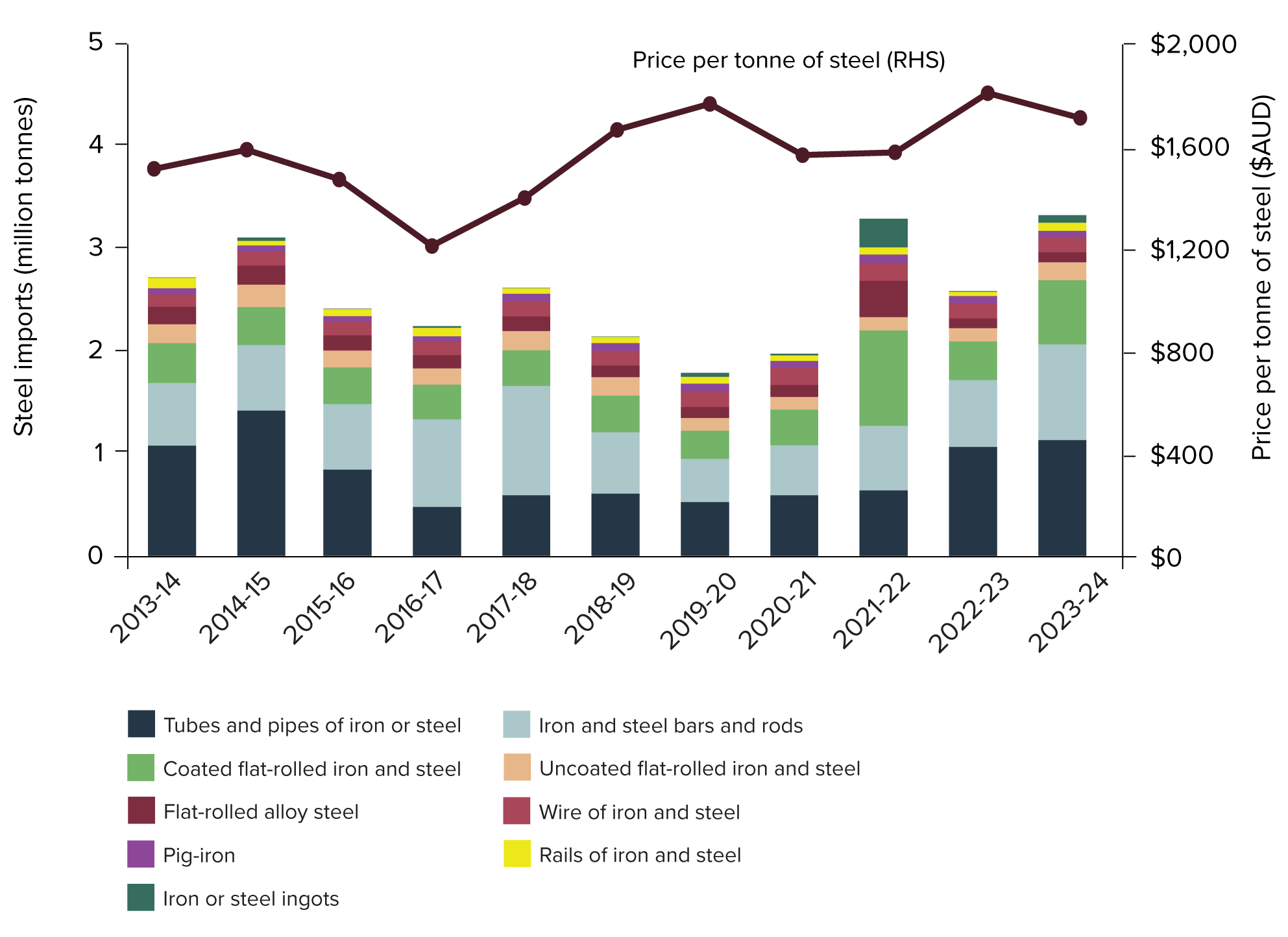

Imported steel is fulfilling local demand for products that are not manufactured anywhere in Australia

In Infrastructure Australia’s 2023 Infrastructure Market Capacity Report, we noted a 20% increase in steel imports over the previous two years compared with the past two decades. It is evident that this reliance on imports has continued with specialised products such as stainless steel and tool steel,25 and Figure 16 shows an increase in overall steel imports in 2023–24. Over the same period, steel prices have decreased due to a combination of factors such as lower global demand, greater global production capacity and changing raw material costs, such as for iron ore.26

Figure 16: Steel imports by type compared to price of steel (2013–14 to 2023–24)

Source: Australian Bureau of Statistics (2024)27

Industry view

Industry is cognisant of both global and domestic risks to supply

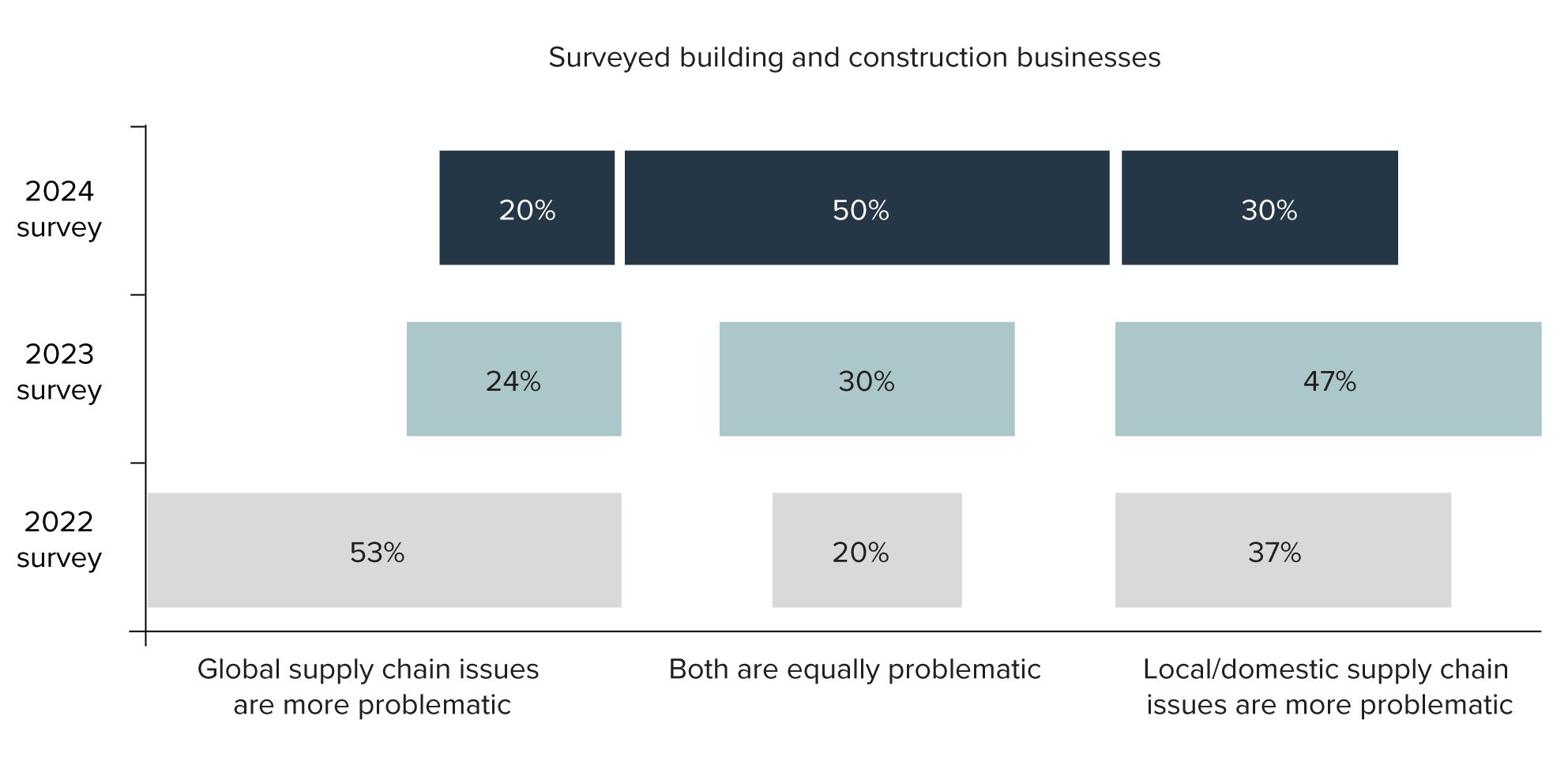

Infrastructure Australia has been tracking industry’s sentiments, through the Industry Confidence Survey, for four years. As shown in Figure 17, there have been shifts in how industry assesses domestic versus global supply risks over that time.

In 2022, just over half (53%) of building and construction businesses surveyed thought global issues alone were responsible for supply-side risks, while 37% thought it was domestic issues and 11% thought it was due to both. In 2023, industry’s opinion switched to viewing domestic factors being the predominant source. This year, half of respondents regarded both global and domestic supply chain issues being equally problematic, compared to 30% who viewed domestic and 20% who viewed global supply-chain risks as being more problematic.

The Russian invasion of Ukraine and the impacts of the COVID-19 pandemic on global supply chains in the preceding years may have elevated industry’s assessment of global risks in 2022. This year, industry is aware of the impacts of both global and domestic supply risks to their business. This aligns with our observations on the need to balance reliance on imports with domestic production capability to mitigate supply risks of key construction materials.

Figure 17: Views of building and construction businesses on whether global or domestic supply chain issues are more problematic, changes over 2022 to 2024

Note: These figures exclude ‘not sure’ responses.

Source: Infrastructure Australia Industry Confidence Survey (2022, 2023, 2024)

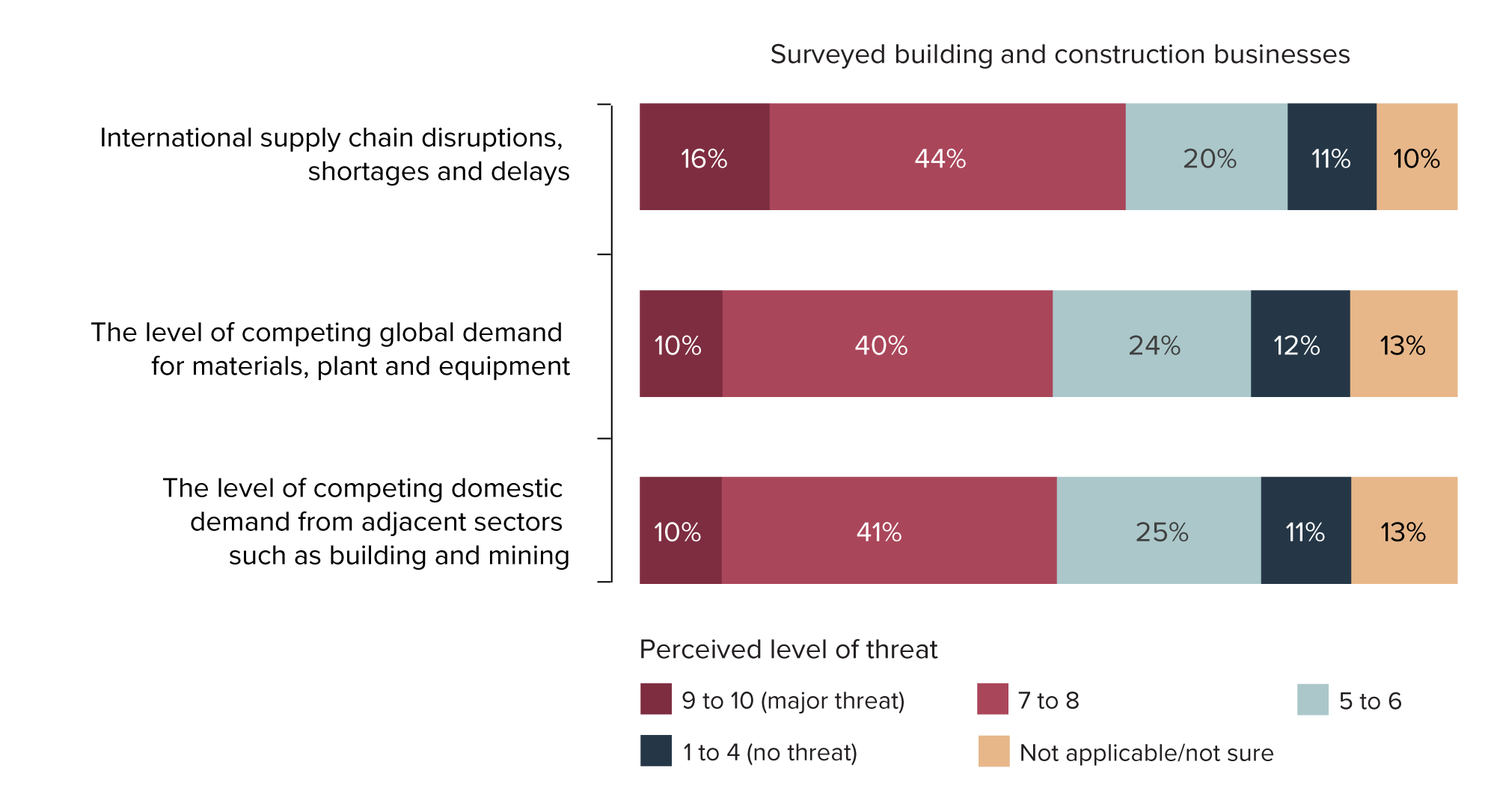

Figure 18 presents industry views on the main risks in sourcing global supplies for infrastructure project delivery. Industry regarded international supply-chain disruptions, delays and shortages as the highest threat (60% ranked as a threat, including 16% as a major threat).

Competing domestic demand from adjacent sectors (such as building and mining) and competing global demand were both regarded by industry as relatively similar levels of threat to the global supply chain (50–51% ranked both as a threat, including 10% as a major threat).

Figure 18: Views of building and construction businesses on the threat level of global supply-chain risk factors to successful delivery of infrastructure projects in Australia

Source: Infrastructure Australia Industry Confidence Survey (2024)

Businesses have noticed a 10–20% price escalation of non-labour costs over the last 12 months and believe prices are yet to peak

62% of surveyed businesses noted an increase in price escalation in terms of non-labour costs over the last 12 months. The vast majority (62%) of industry surveyed noted the increase in price for non-labour resources this year. Of those that noticed this increase in costs, 64% reported a 10–20% increase.

Many believe a peak in non-labour costs is still yet to come. In fact, 43% say that prices are increasing at an accelerating rate, whereas 36% believe they have been doing so at a steady rate.

Looking specifically to those surveyed within the Civil Contractors Federation membership, the largest group (45%) said they had noticed an increase of between 10–25% in the cost of project inputs. Only 18% noted an increase of more than 25%. However, these figures reflect respondents’ views of both labour and non-labour inputs combined, not solely materials.

These industry perceptions on cost increases are largely consistent with Infrastructure Australia’s analysis of the Australian Bureau of Statistic’s price index data,28 which shows that non-labour inputs are 80% higher now than in 2010–11.

Spotlight

Spotlight: Steel and steel products

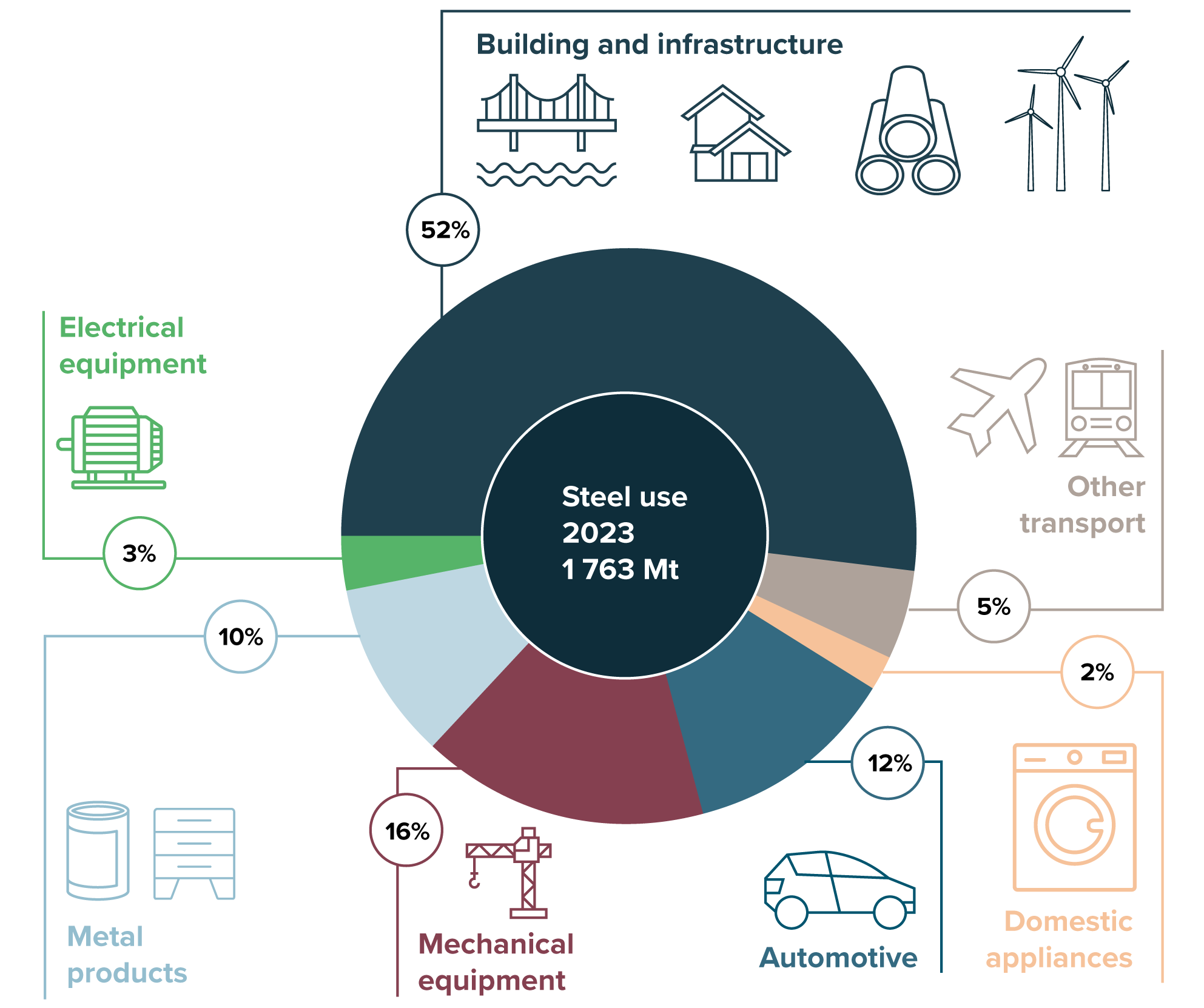

Australia needs 8 million tonnes of steel to deliver the pipeline of public and private sector construction projects over the next five years.

Steel is a critical input of transport, energy and other infrastructure projects, and a critical construction input overall. As shown in Figure 19, over half the world’s annual steel output (52%) was used within buildings and infrastructure.

Figure 19: Global steel use by sector

Source: World Steel Association (2024)29

Imported steel and global supplies

The global steel industry, producing over 1.8 billion metric tonnes of steel annually, is dominated by a few major producers: China (the largest), India, Japan, the United States and Russia.30 Australia plays an important role in the global steel supply chain, by mining and exporting iron ore and coking coal for steel production.

Local Australian steel output is supplemented by imported steel, some of which is critical for project success, particularly finished-steel products that are not manufactured in Australia, such as stainless steel and tool steel. Over 2013–14 to 2023–24, Australia imported approximately 2.5 million tonnes of steel a year.

Using imported steel in local construction can expose projects to risks inherent to global resourcing, such as price fluctuations, greater competition, supply-chain disruptions, product quality variances and local compliance modifications.

Additionally, embodied carbon emissions of imported steel can create uncertainty, add complexity and compromise Australia’s measures and efforts in decarbonising the infrastructure sector.

Domestic steel production

With an estimated output of 5.3 million tonnes annually, Australia’s steel industry is substantial. There are four major manufacturers of steel in Australia, supported by over 300 distribution outlets and numerous manufacturing, fabrication and engineering companies.31

The capabilities of the Australian steel industry include: steel manufacturing, roll-forming, distribution, fabrication, construction modelling, hot dip galvanizing, protective coatings and grating and handrails.

Steel fabrication

Analysis undertaken with the Australian Steel Institute reveals Australia has an estimated steel fabrication capacity of 1.4 million tonnes per year. The domestic steel-fabrication sector is comprised of majority small and medium-size enterprises, many of which are multi-generational family-owned businesses.

Whilst some businesses continue to operate as traditional ‘jobbing’ shops, many have developed specific areas of specialisation and associated capabilities. These include: bridge work, architectural steelwork, refurbishment and maintenance of mining equipment, sheet metal fabrication, chemical-industry infrastructure, civil construction, wind tower fabrication, and portal-frame structures.

Green steel

The Australian Government has identified green metals (including green steel) as a priority industry under its Future Made in Australia National Interest Framework. While Australia is in the early stages of developing facilities with the capacity to produce green steel, it has the potential to reduce carbon emissions from the steel-production process and maximise the economic and industrial benefits of our move to net zero.

The Australian Government 2024–25 Budget commits funding for Green Metals Foundational Initiatives that will explore ways government can stimulate demand, including industry participation frameworks at federal and state levels, which will help define opportunities for the inclusion of green metals in energy, defence, infrastructure and housing projects.32

Domestic steel fabrication supply capacity analysis

Australia needs 3.8 million tonnes of fabricated steel structure elements over 2023–24 to 2027–28.. By sector, buildings will require 55% of total demand for fabricated steel, transport 29% and utilities 16%.

Based on data provided by the Australian Steel Institute, we analysed the capacity and location of 296 domestic steel fabricators, representing an estimated 70% of total domestic capacity. As shown in Table 4, we estimate these producers have a capacity to produce approximately 939,500 tonnes annually, with over two-thirds (69%) capacity located across New South Wales, Queensland and Victoria.

We note that based on the Australian Steel Institute dataset, there is currently very little capacity in the Northern Territory, at less than 1% of total domestic capacity. However, the Territory will require 7% of national demand.

Table 4: Steel fabrication capacity versus demand, by state and territories

| State/territory | Estimated annual capacity (tonnes) | % of total capacity | % of demand |

|---|---|---|---|

| New South Wales | 255,000 | 27% | 34% |

| Queensland | 199,000 | 21% | 17% |

| Victoria | 195,000 | 21% | 20% |

| Western Australia | 152,000 | 16% | 9% |

| South Australia | 114,500 | 11% | 6% |

| Tasmania | 14,500 | 2% | 2% |

| Australian Capital Territory | 7,000 | 1% | 2% |

| Northern Territory | 2,000 | 0% | 7% |

| Australia | 939,500 | 100% | 100% |

Note: Percentages do not add to 100% due to rounding.

Source: Infrastructure Australia analysis of Australian Steel Institute data (2024)

Delivery of fabricated steel to project sites will be critical for our energy transition